The Edge Capacity Arbitrage: Build the Brokerage for the AI Infrastructure Nobody Wants to Underwrite

The next phase of the AI boom will not happen entirely inside billion-dollar data centers in Northern Virginia.

Some of it will happen in a secure room beside a warehouse in Fort Worth. Some will sit inside an industrial building near a logistics corridor. Some will live in a small colocation facility with 15 kilowatts of available power that nobody has bothered to market properly.

The opportunity isn't to turn every vacant office closet into a miniature data center. That sounds clever until you meet the unglamorous realities of power distribution, redundant cooling, fiber diversity, fire suppression, physical security, and uptime guarantees. The viable heist is narrower and more valuable. Build a specialized edge colocation brokerage and intelligence platform for small, verified footprints: 1 to 20 kilowatts of low-latency compute in buildings that already have the right infrastructure or can be upgraded economically.

Here's the opportunity:

The money: A lean two-person team can reach $250K to $750K a year. At scale, 100 active deployments yield $20K in monthly recurring commissions before assessments and data subscriptions.

Inside:

• Five-stream pricing for a concierge brokerage

• The six-category Edge-Readiness Score

• DFW beachhead map and supply playbook

• Five compounding moats nobody can scrape

Think of it as a cross between LoopNet, a data-center procurement consultant, and a technical underwriting desk. It helps companies find the small pockets of infrastructure they need near warehouses, factories, retail clusters, and metro cores without negotiating blindly with landlords, carriers, and colocation providers. It won't be an instant-booking marketplace on day one. It's a high-touch brokerage with a software layer, and that software layer gets more defensible with every site survey, every latency test, every retrofit estimate, and every completed deployment. That is where the real business lives.

The bottleneck is moving closer to the customer

AI training created demand for enormous centralized clusters. AI inference creates a more complicated map.

Inference is the moment a trained model actually does something: interprets a video feed, detects an anomaly, answers a query, routes a robot, analyzes a sensor stream. More and more, these workloads need to run near the places where the data is generated. Intel frames edge computing as processing data closer to its source so time-sensitive applications can respond in real time. NVIDIA is shipping edge-AI platforms for autonomous machines and industrial automation. AWS sells Local Zones and Outposts around the same need: put compute near users, local machinery, on-premises systems, and regulated data.

The cloud isn't disappearing. The architecture is fragmenting. A warehouse robotics system may still train models centrally and ship long-term analytics to the cloud, while local infrastructure handles the video inference, fleet coordination, model serving, and caching that turn slow, expensive, or fragile when every request travels to a distant region. You aren't selling a remote server room as the brain of a forklift. You're selling a resilient intermediate layer between the device and the hyperscale cloud, and that layer matters more as AI moves into physical space.

The hyperscalers have already named the category. AWS Local Zones place select cloud services near end users for very low latency, and its second-generation Outposts racks extend AWS into on-premises and colocation spaces, with the company citing industrial control systems and edge inference among the use cases. They're validating the demand, but they aren't solving every deployment. A robotics vendor rolling out across 40 warehouses doesn't want to build and babysit a hardened server room at every site. A retail-analytics company may need local video processing in several metros without the volume to negotiate directly with the big colocation operators. These buyers don't need more raw real-estate listings. They need a trusted answer to one technical question: where can I place 8 kilowatts of resilient compute near this corridor, with the right fiber, cooling, security, and timeline?

The market is large. The wedge is deliberately small.

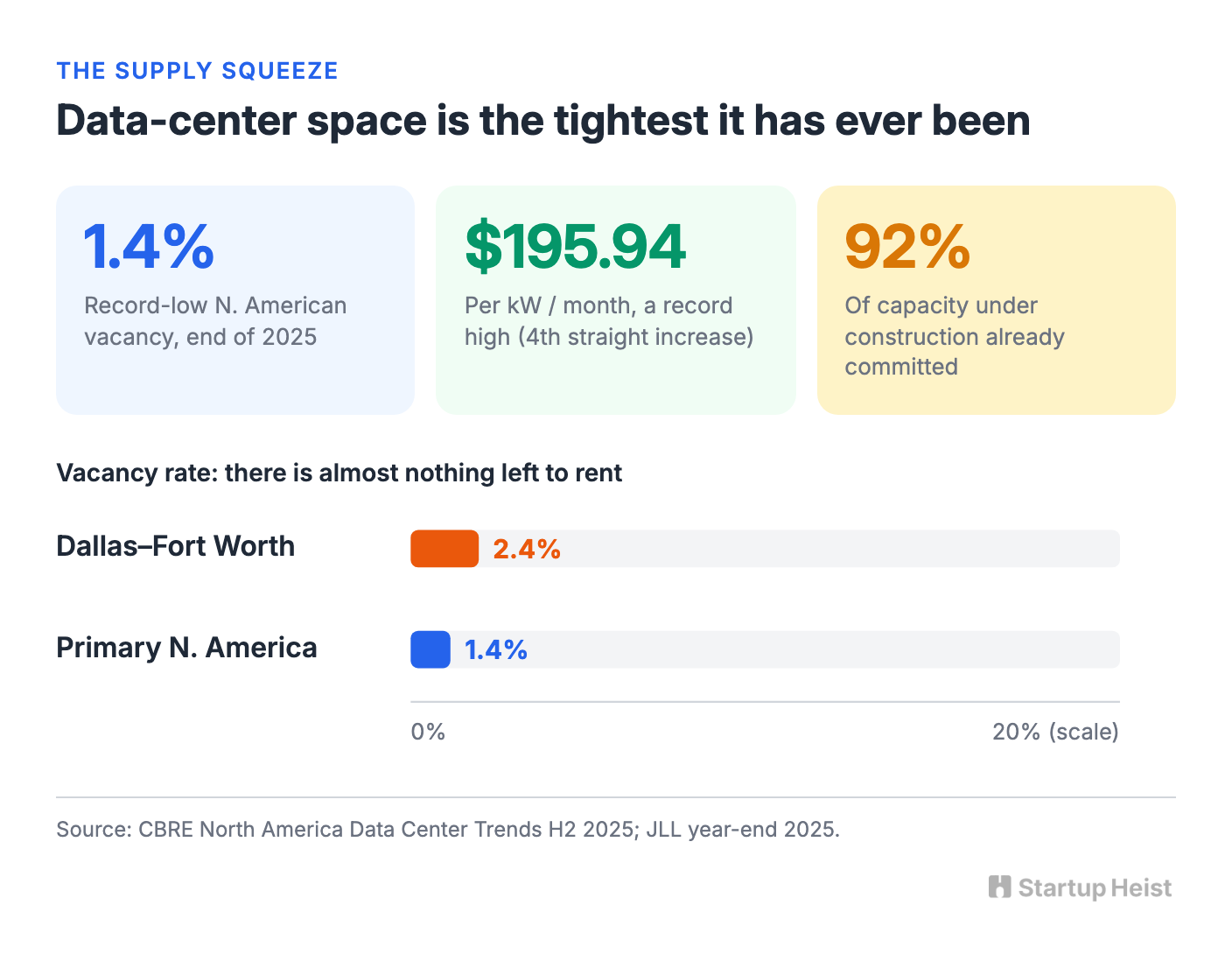

The broader data-center market is already tight. CBRE reported that vacancy across primary North American markets fell to a record-low 1.4% at the end of 2025, with inference AI explicitly named as a driver of demand for more regional and distributed infrastructure. Average asking rates for 250-to-500-kilowatt wholesale requirements hit a record $195.94 per kilowatt per month in the second half of 2025, the fourth straight annual increase. JLL reported that 92% of North American capacity under construction was already committed at year-end.

Tight supply doesn't guarantee a gold rush at the small end. Edge has been overhyped before. Back in 2020, the Uptime Institute warned that suppliers were seeing a trickle of micro-data-center orders rather than the predicted flood, and that the underlying business cases can be genuinely complex. That history should shape the company. Don't raise money to blanket America with server closets. Don't buy buildings. Don't build speculative nodes and pray that autonomous-vehicle startups show up.

Start with a more conservative premise: there's a procurement failure hiding inside a growing category. The customer needs a small amount of specialized capacity. The supply exists in fragmented pockets. The specs are inconsistent, the economics opaque, and the best sites nearly impossible to find through a generic commercial real-estate search. The winning company organizes the market before it tries to automate it.

Why Dallas-Fort Worth is the right beachhead

Austin makes a better headline. Dallas-Fort Worth makes a better first market.

DFW is already a serious data-center hub. CBRE reports the region crossed roughly 1 gigawatt of colocation inventory by the end of 2025 with a vacancy rate of just 2.4%, the third North American market to pass 1 GW after Northern Virginia and Atlanta. Around 700 megawatts of additional capacity is under construction, and 94.5% of it is already preleased. It's also a logistics machine. DFW International Airport says air cargo contributes more than $20 billion a year to the North Texas economy, and the region sits at the crossroads of air, road, rail, e-commerce, and industrial development. AllianceTexas alone combines an intermodal yard, two Class I rail lines, highways, and an industrial airport.

That combination hands you both sides of the marketplace. On the supply side: existing data-center operators, carrier-dense facilities, industrial landlords, and infrastructure vendors. On the demand side: warehouses, distribution centers, manufacturers, robotics integrators, computer-vision vendors, and retail-logistics operators. Your first map shouldn't cover the country. It should cover a handful of corridors: DFW Airport and Las Colinas, AllianceTexas and north Fort Worth, the Plano-Richardson Telecom Corridor, Irving and Carrollton, South Dallas industrial clusters, and the sites near existing carrier hotels. You aren't after thousands of mediocre listings. You want the first 50 to 100 sites where a credible technical conversation can begin.

The product is an underwriting system, not a marketplace

Marketplaces for traditional colocation already exist. OCOLO lists more than 3,300 facilities across 89-plus countries, letting providers showcase power density, cooling, certifications, and connectivity. Operators like TierPoint already offer secure colocation, redundant power, carrier-neutral connectivity, cloud on-ramps, and remote hands. You won't beat them by building a prettier directory of standard data centers.

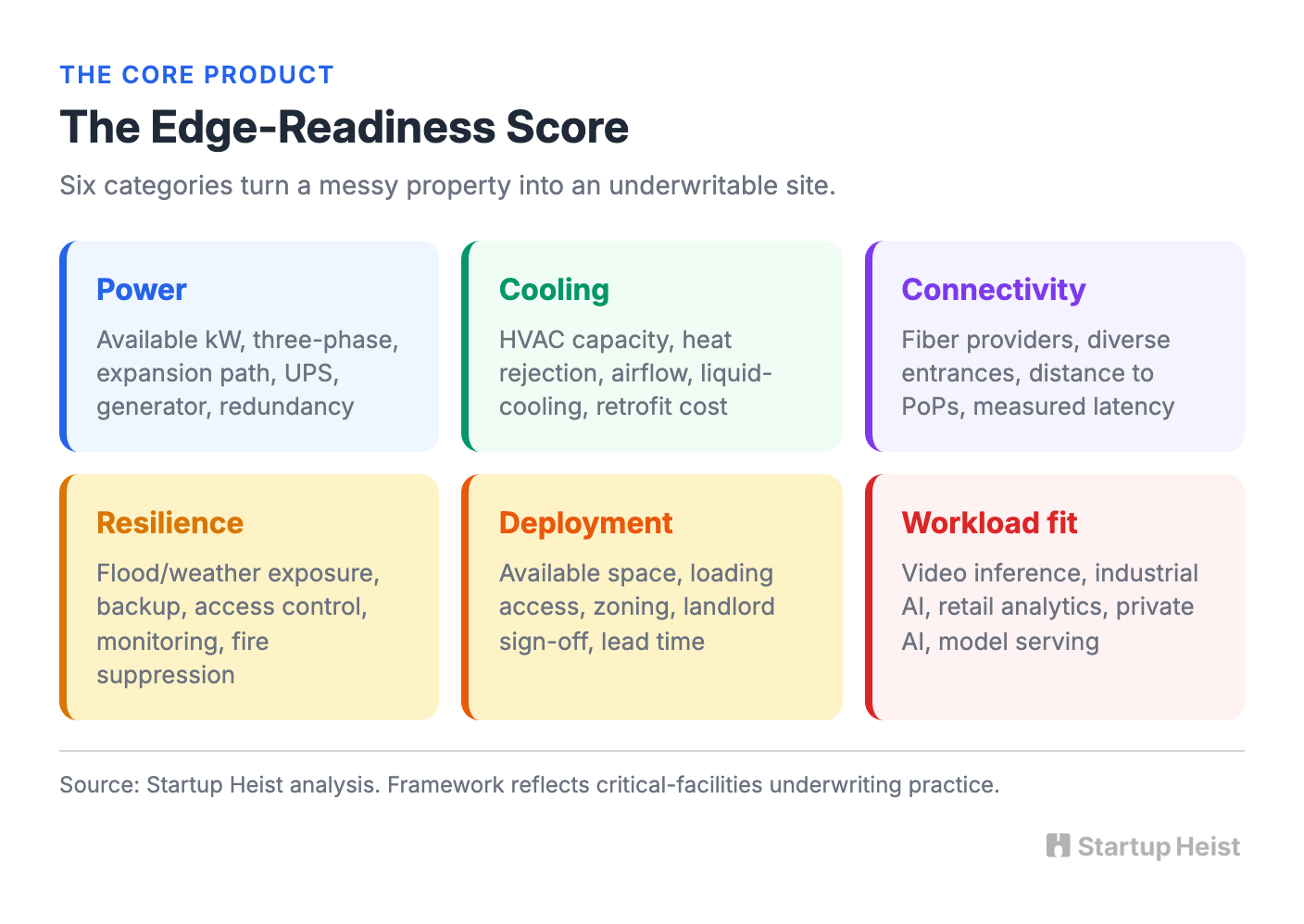

The opportunity begins exactly where their sales workflows break down: the buyer needs only 4 to 12 kilowatts, the location is unusually specific, the best option is a small regional colo or a qualified industrial property, the landlord can't describe the asset, and the buyer can't judge retrofit risk from a listing. The platform standardizes that messy middle. The core product is an Edge-Readiness Score, a structured assessment of each site across six categories.

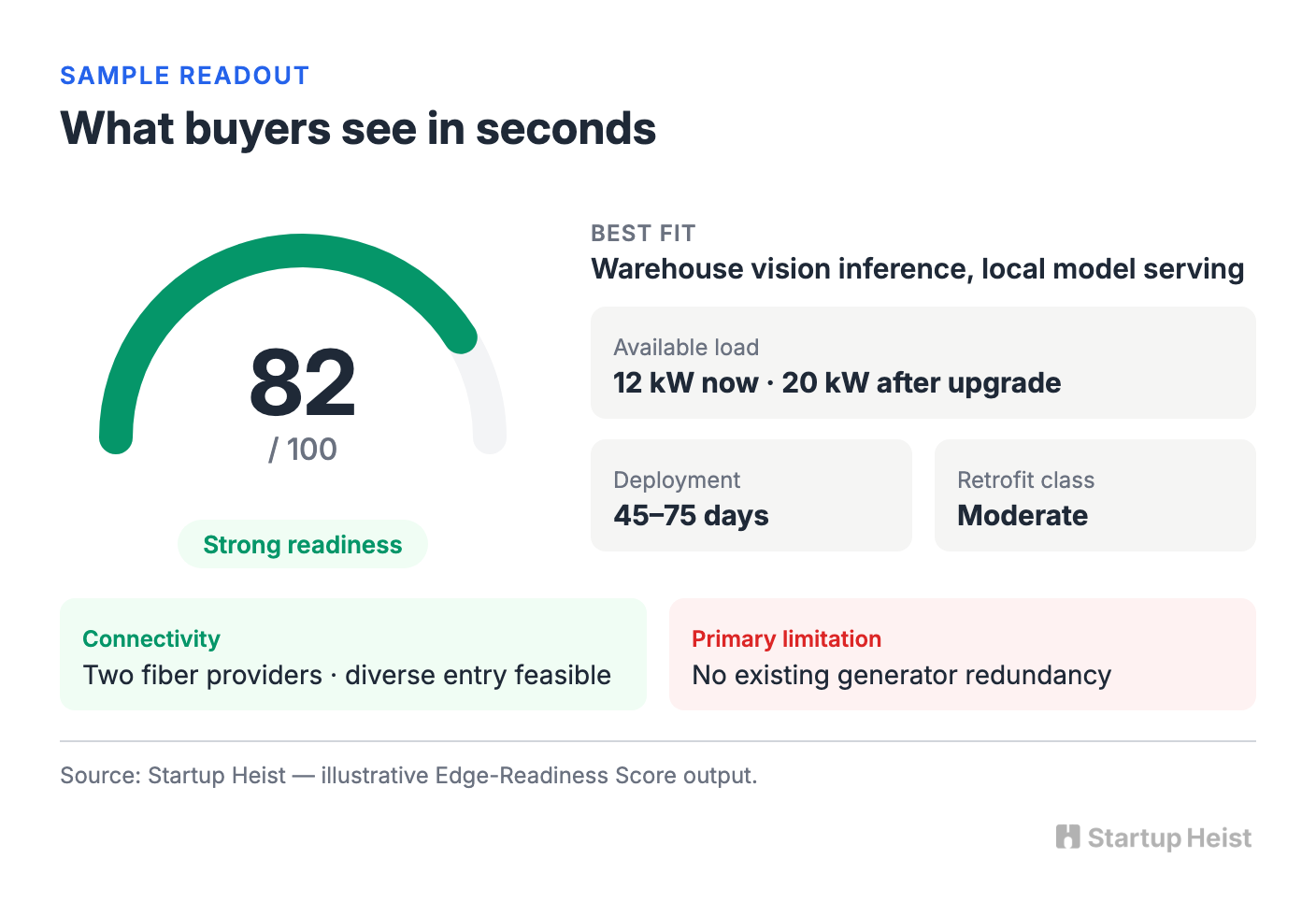

The output should be simple enough to read in seconds:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”