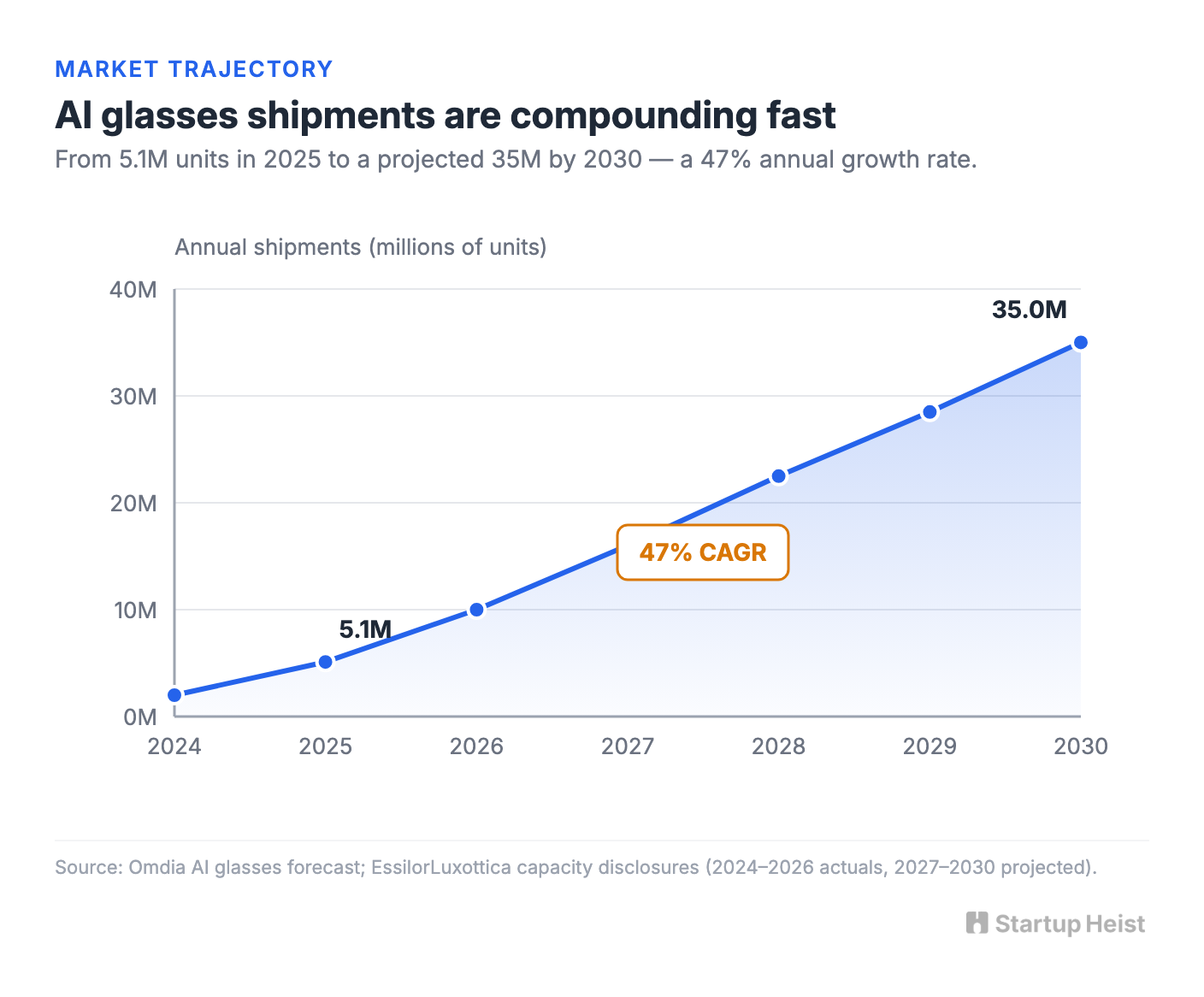

EssilorLuxottica sold over 7 million Meta AI glasses in 2025, more than triple the prior year. Production capacity talks have moved from 10 million units to 20 million, with internal discussions now pushing toward 30 million if demand holds. Omdia projects 35 million AI glasses shipping annually by 2030, a 47% compound growth rate from 2025.

This category isn't waiting to happen. It's arriving.

And almost no one is building the brand that should be building itself around it: the Dbrand of face-tech. Skins, wraps, clip-on lenses, comfort grips, privacy covers, and limited drops for the new computer on your face.

When a device lives in your pocket, people care about protection. When it lives on your face, they care about identity. Phones became a skin-and-case business. Apple Watches became a band business. Crocs became a charm business. Sneakers became collectible culture. AI glasses are next, and the people who own that layer can't be the giants making the hardware. The opening belongs to someone smaller, faster, and willing to make the weird stuff.

The first wave of AI glasses tested whether anyone would wear them. The second wave tests whether people like how they look while wearing them, and that's the wedge.

Here's the opportunity in one frame:

The money: $10K to $30K MRR target territory in year one with disciplined monthly drops and bundle AOV above $50. Low six figures profitable, seven figures with execution.

Inside:

• MVP scope: 12-18 SKUs, Wayfarer first

• Bundle pricing and unit economics math

• Four-phase GTM with creator seeding

• Four-layer moat: templates, trust, content, culture

Why this exists now

For years, smart glasses had the same problem. They made the wearer look like a beta tester. Google Glass read as a social warning label. Early AR headsets looked like lab equipment. Most camera glasses landed somewhere between geeky and creepy. The technology was interesting. The form factor was socially expensive.

Ray-Ban Meta changed that. The product isn't perfect, but it succeeded at one thing every prior attempt failed at: it made smart glasses look like glasses. The lineup now spans the Wayfarer from $329, the sportier Oakley Meta variants, and the $799 Ray-Ban Meta Display with a heads-up screen and a wrist-worn neural input band. The Display launched in late 2025 and the waitlist already extends into the back half of 2026. Meta had planned expansion to Canada, the UK, France, and Italy. It paused that rollout indefinitely in January 2026, unable to keep up with U.S. demand. The bottleneck is supply, not interest.

The rest of the field is filling in fast. On April 29, 2026, the Chinese brand Moonix unveiled its Monet AI glasses in Silicon Valley: 14.9 grams in the standard model, 4 millimeter temples, designed to look like luxury eyewear that quietly contains AI rather than wearable tech that pretends to be jewelry. Apple is testing four design variants. Google's Android XR glasses are further along than press coverage suggests, with confirmed hardware partnerships across Samsung, Warby Parker, and Gentle Monster, signaling that the fashion-and-tech intersection is now the explicit playing field. Xiaomi is in. Rokid is in. Snap re-entered the category in April 2026.

The hardware companies have stopped trying to make sci-fi goggles. They're making normal eyewear that quietly contains AI. Once that works, the buyer changes. The first buyer asks what the device can do. The second buyer asks how it looks on them, and the second buyer is the one who buys accessories.

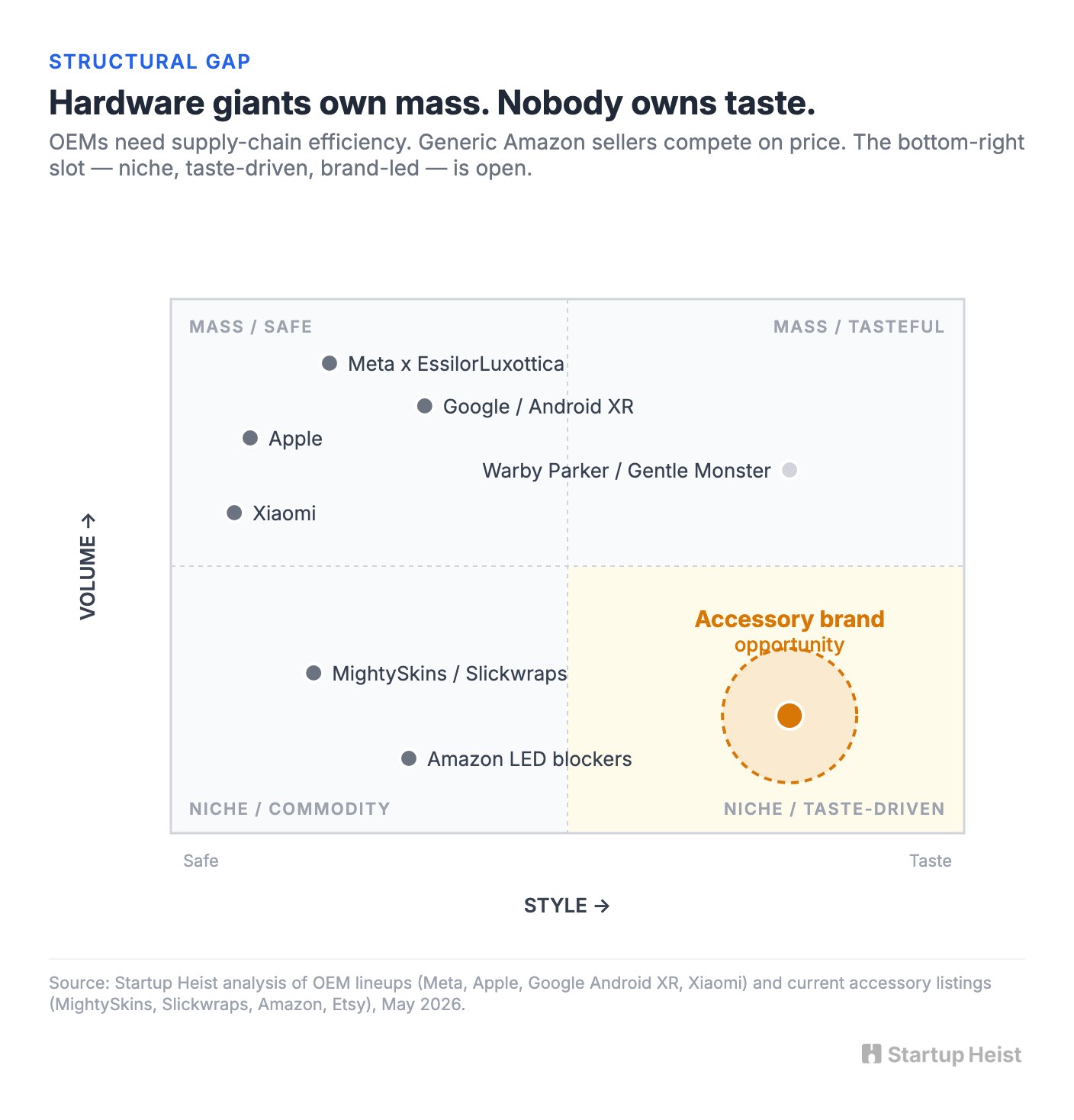

The structural gap: mass SKUs versus taste

Meta and EssilorLuxottica have to serve millions of people. Safe colors. Safe shapes. Predictable inventory. A few seasonal variants and the occasional premium edition. Hardware companies can't treat every frame like streetwear. They need supply-chain efficiency.

An accessory brand doesn't. A small brand can ship the stuff a giant cannot ship: translucent smoke wraps, racing-stripe temples, matte bone, tortoise overlays, cyberpunk lens clips, office-friendly privacy caps, creator collabs, festival kits, founder kits, runner kits, "do not record me" kits. The large company has to avoid looking silly. The small brand can make silly profitable.

Demand is already proven. MightySkins sells 3M-vinyl precision wraps for both Ray-Ban Meta Wayfarer generations. Slickwraps does too. Etsy sellers are moving custom temple covers. Amazon listings under brands like JYXEREM and Jujuclips are selling LED light privacy covers and clip-on camera blockers, often at impulse-buy prices. Target carries a Ray-Ban Meta accessory section now. The category exists. What's missing is brand. Most of these listings feel like catalog commerce: interchangeable, generic, priced like a sticker rather than positioned like a fit.

Dbrand didn't win because vinyl was hard to cut. It won because it turned device customization into a brand language: sharp copy, limited drops, memes, creator integrations, obsessive fit guarantees. The AI glasses skins version of that doesn't exist yet. There's competition. There's no category owner.

The product surface

The accessory category breaks into four product families, and a serious brand should treat them as one connected wardrobe rather than four separate Shopify collections:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”