ISO-Ready: The Payment File Layer SMB Exporters Don't Know They Need Yet

Most small exporters don't think they're in the financial messaging business.

They think they sell machine parts, specialty chemicals, food ingredients, electronics components, textiles, or industrial supplies. They keep the books in QuickBooks or Xero. They push wires through their bank portal. When something breaks, they call the bank, forward a PDF invoice, retype an address, and hope the money moves.

That world is getting less forgiving.

Cross-border payments are moving onto ISO 20022, a global financial messaging standard built around richer, structured data. Instead of loose, free-text instructions, banks want machine-readable information about parties, addresses, bank identifiers, purpose codes, remittance details, and transaction context. Cleaner inputs make payments easier to screen, route, reconcile, and monitor. Messy inputs stop being a clerical nuisance and start becoming failed payment files.

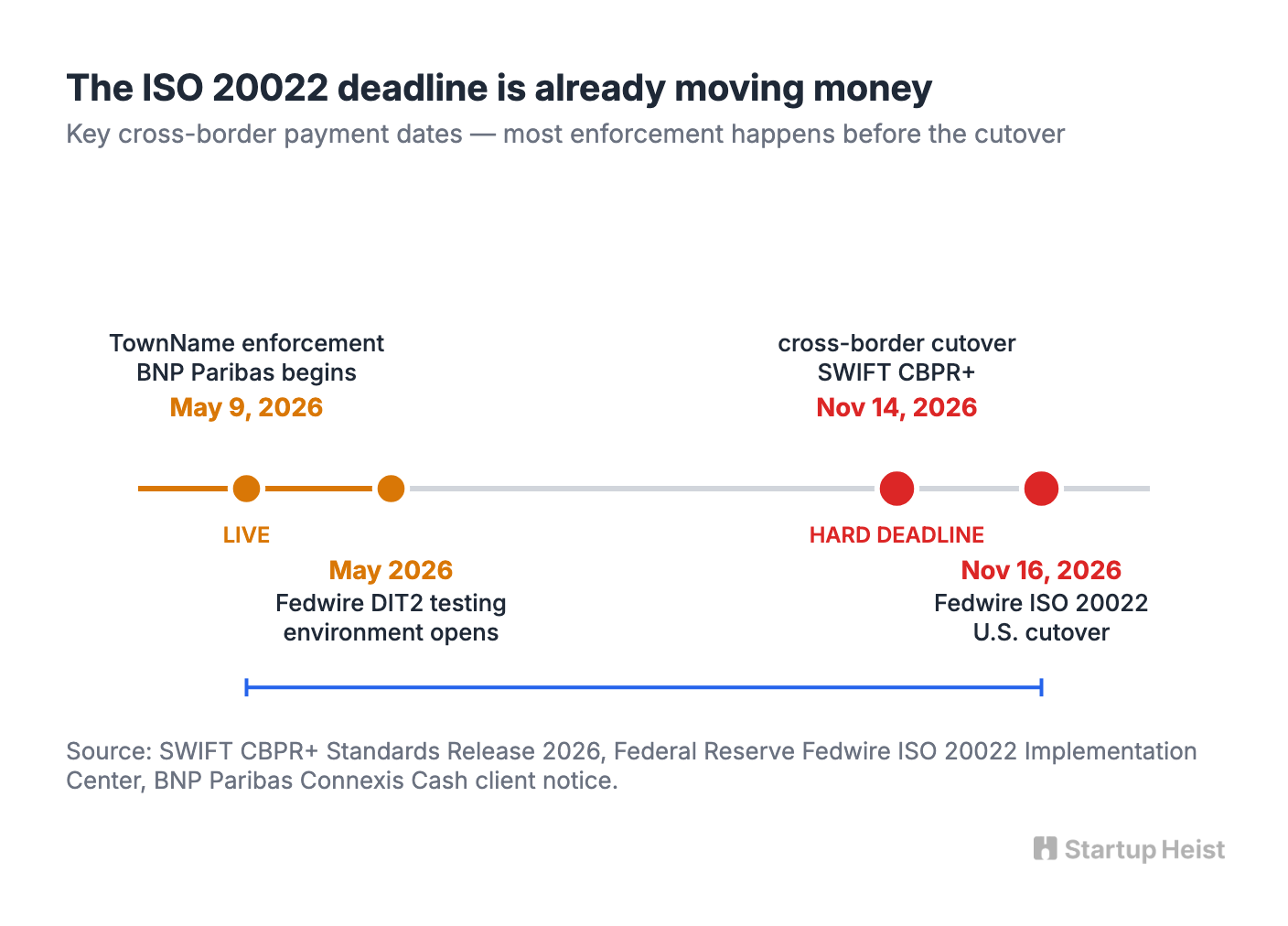

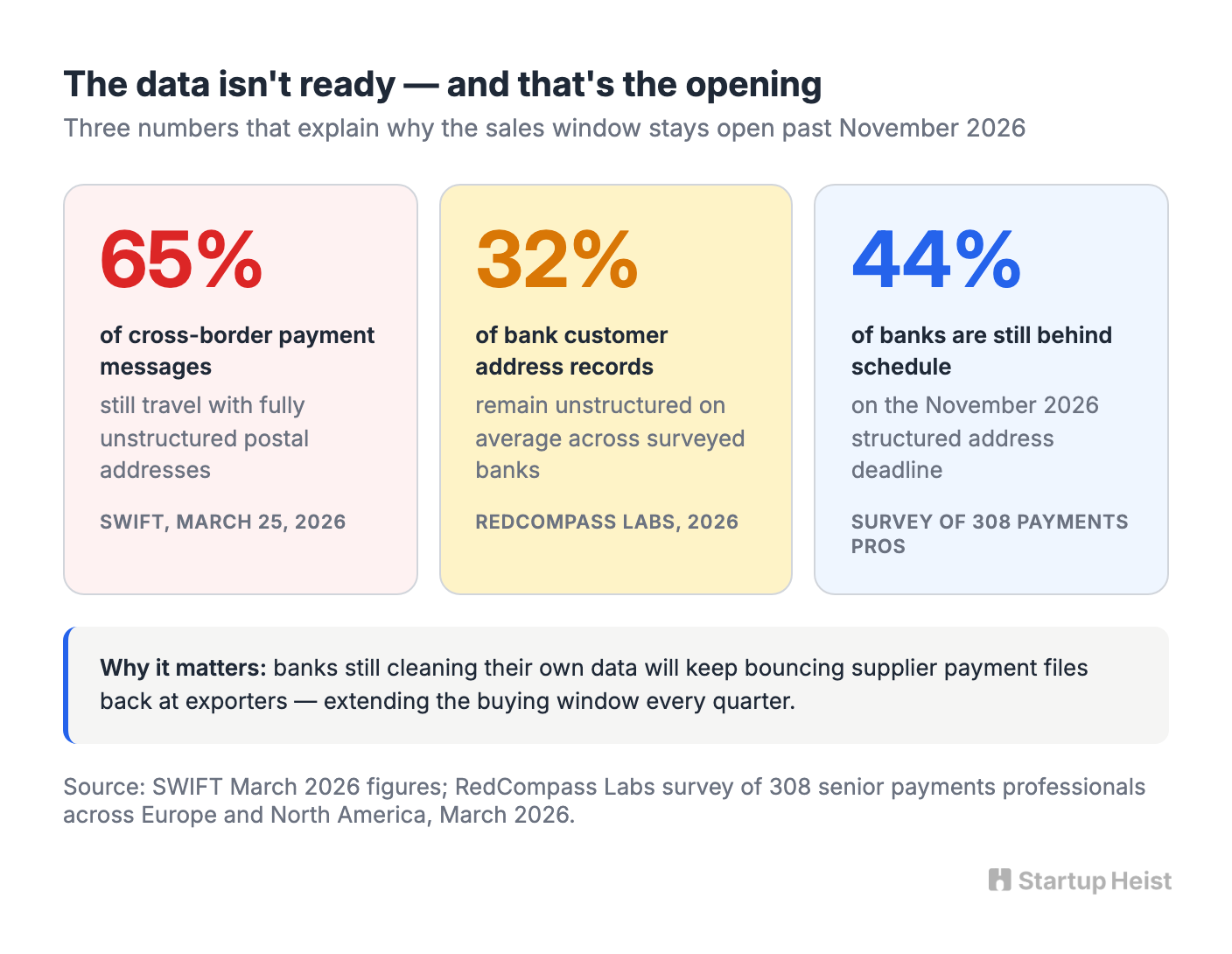

The near-term wedge is specific. On November 14, 2026, SWIFT removes fully unstructured postal addresses from cross-border payment messages under CBPR+ Standards Release 2026. Two days later, on November 16, 2026, the Federal Reserve's Fedwire Funds Service does the same on the U.S. domestic high-value rail. Three free-text address lines disappear. Town and country become mandatory in dedicated fields. Roughly 65% of cross-border payment messages still travel with unstructured addresses today, per SWIFT's own March 25, 2026 figure. JPMorgan's client guidance is blunt: fully unstructured addresses won't be accepted.

So there's a clean opening. Build a niche B2B micro-SaaS that plugs into QuickBooks and Xero, validates outbound supplier payments, converts them into bank-specific ISO 20022 pain.001 XML files, and gives small and mid-market exporters a practical way to become payment-data ready without buying a treasury system or upgrading their ERP. You're not replacing Stripe. You're not building a global payments company. You're not a bank. You're a translation layer between accounting software and an increasingly intolerant financial network.

Here's the opportunity:

The money: $100-300K ARR at 500-1,500 customers paying $99-499/mo, plus $750-5,000 setup fees. Realistic path to a profitable solo vertical SaaS.

Inside:

• Bank-specific payment packs as the real moat

• Free vendor data audit as the wedge offer

• $99-499 SaaS pricing plus setup fees

• Deadline-driven outbound to controllers

The Problem: Accounting Software Was Built for Humans. ISO 20022 Is Built for Machines.

A small exporter's accounting system holds enough information for a human to make sense of a payment. A vendor name. A mailing address pasted from an old PDF. An invoice number. A bank account. Maybe a SWIFT/BIC code, maybe an IBAN. The country might be buried in a free-text address line. The remittance description might say "payment for parts." The same supplier might be formatted one way for Germany, another for Mexico, a third for Japan. For years, the banking system has absorbed this mess through human repair and legacy MT message formats.

ISO 20022 reverses the direction of travel. It pushes the standard toward structured fields and shoves the cleanup work upstream onto the originator. The Bank for International Settlements has tied its harmonisation program to a 2027 alignment target for all major payment infrastructures. Friction no longer gets absorbed quietly inside the bank. It surfaces as a payment in manual review, a beneficiary record that needs repair, a wire that arrives late because a field was missing, a supplier asking where the money is.

Large companies throw consultants, treasury management systems, and bank implementation teams at this. A $200 million manufacturer running SAP and Kyriba has options. The upper-SMB exporter running QuickBooks does not. That's the gap a small, sharp product can step into before the deadline closes it.

Why Now: November 2026 Is Already Live

Deadlines create budget. This one is already moving money.

SWIFT confirms November 14, 2026 as the cutover for CBPR+ messages. The Federal Reserve's ISO 20022 implementation center confirms November 16, 2026 for Fedwire. The DIT2 testing environment opened in May 2026, giving banks and corporates six months of runway. Treasury teams that haven't started are already behind. And the deadline isn't the only forcing function. MT101, the legacy Request-for-Transfer format, reaches end-of-life in November 2026 and is being replaced by pain.001 version 9. Companies still on MT101-based bank flows face a double migration: format and address.

The pain isn't theoretical. On May 9, 2026, BNP Paribas began validating and enforcing the TownName field for Connexis Cash users. Early enforcement, before the November deadline, on a major bank. Other banks are watching. RedCompass Labs surveyed 308 senior payments professionals across Europe and North America in March 2026 and found 44% of banks still behind schedule on the structured address deadline, with an average of 32% of customer address records still unstructured. Nearly one in ten banks has more than half of their address data non-compliant. That means customer-facing banks will keep bouncing supplier payment files back at exporters until their own systems catch up. The sales window doesn't close on November 16, 2026. It extends through every quarter that banks spend cleaning up their side of the pipe.

The buyer doesn't want a 70-page ISO 20022 guide. The buyer wants a green checkmark that says: "This payment batch is ready for your bank." Whoever ships that checkmark first owns the moment of confusion.

The U.S. Census Bureau identified 270,001 U.S. exporters in 2024, generating $1.817 trillion in goods exports. SME exporters made up over 97% of that count and roughly 35% of known export value. A meaningful slice of that long tail uses QuickBooks or Xero and still pushes payments through bank portals. A $199-per-month product reaches roughly $1.2 million ARR at 500 customers. At 1,500 customers, it's a $3.6 million ARR business. Add setup fees and bank-template packages, and a profitable small vertical SaaS company comes into view.

The Existing Competition Proves Demand and Leaves the U.S. Exporter Gap Wide Open

A real market exists, but the existing tools serve a different geography.

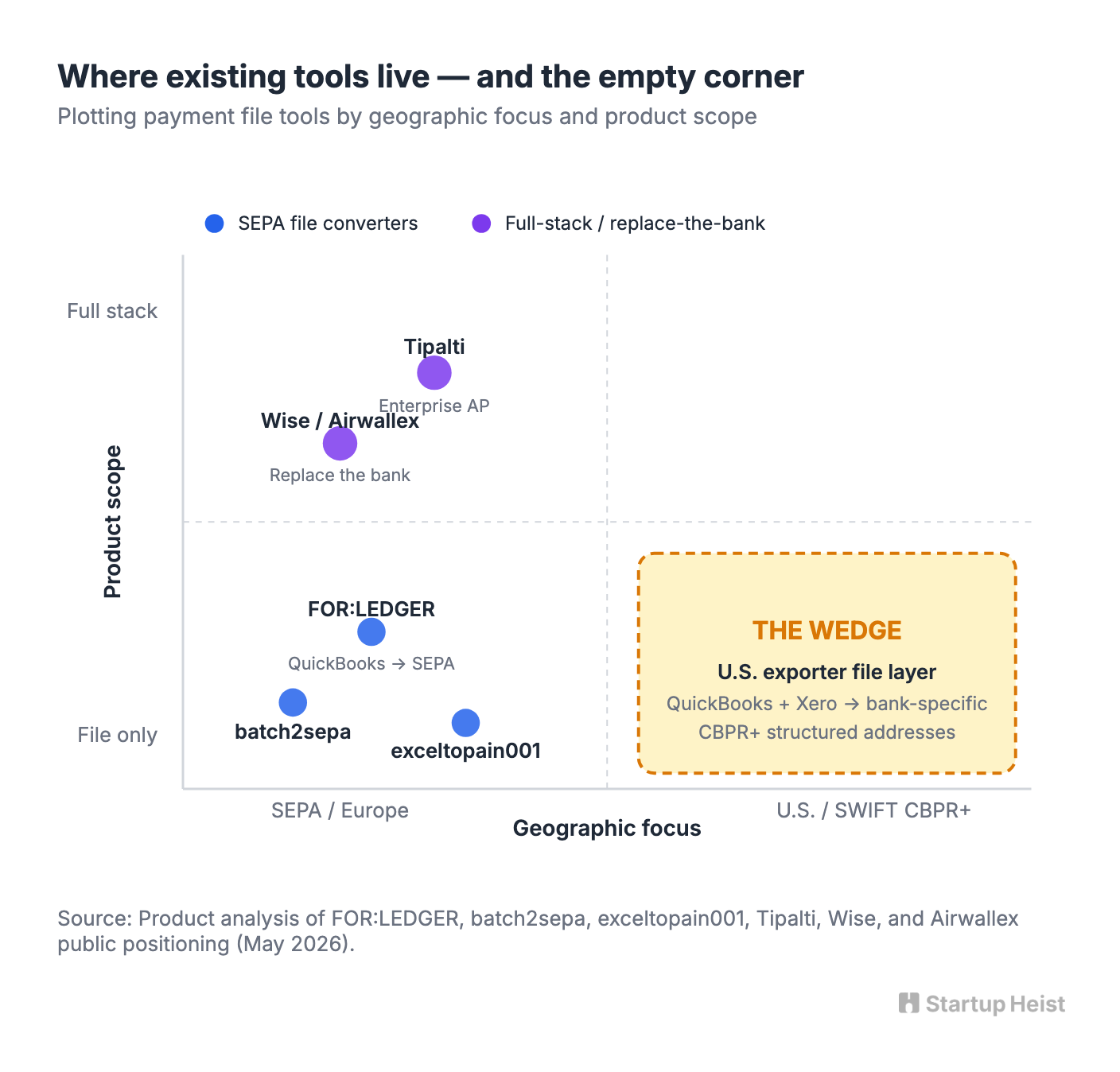

The closest existing product is FOR:LEDGER, a live QuickBooks to ISO 20022 payment file generator with pain.001 and pain.008 support. It runs across 36 SEPA countries and is built for European businesses using QuickBooks. Its existence is the strongest possible signal that the accounting-software-to-bank-file market is real. Its scope is also the proof that the U.S. CBPR+ side is wide open. batch2sepa turns Xero batches into SEPA pain.001 and pain.008 XML. exceltopain001 converts spreadsheets to SEPA and ISO 20022, with newly added SWIFT/MT103 support, but still European-bank-compatible. The open-source pain001 Python library covers multiple pain.001 versions. Tipalti integrates with QuickBooks and Xero but pushes upmarket on price and complexity. Wise and Airwallex ask buyers to abandon their bank entirely.

The pattern is consistent. The current tools are corridor-specific, SEPA-focused, or built for European batch payments. None of them are built for U.S. exporters wrestling with SWIFT CBPR+ structured addresses, Fedwire migration, bank-specific implementation quirks, and beneficiary data remediation across a fragmented set of U.S. banks. SWIFT has even released an open-source AI model to help institutions convert unstructured addresses to structured format, which means raw conversion is becoming a commodity. The defensible product isn't the conversion. It's the accounting integration, the bank-specific templates, the supplier data hygiene, and the U.S. exporter workflow.

The wedge is the middle. Too complex for manual bank portal cleanup. Too small for enterprise treasury software. Too U.S.-centric for the SEPA-native tools. The existing converters also treat the file as a one-shot artifact. The real product treats supplier and payment data as an ongoing record that needs to stay ISO 20022 ready every time a batch goes out. The deadline is coming. The buyer is real. The window is open right now.

The Product: A Bank-Specific ISO 20022 Readiness Layer

The MVP should be boring. That's a compliment.

Core Workflow

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”