Data-center fortunes used to be made on cooling systems and infrastructure hardware. The next one will be made on information about local fights.

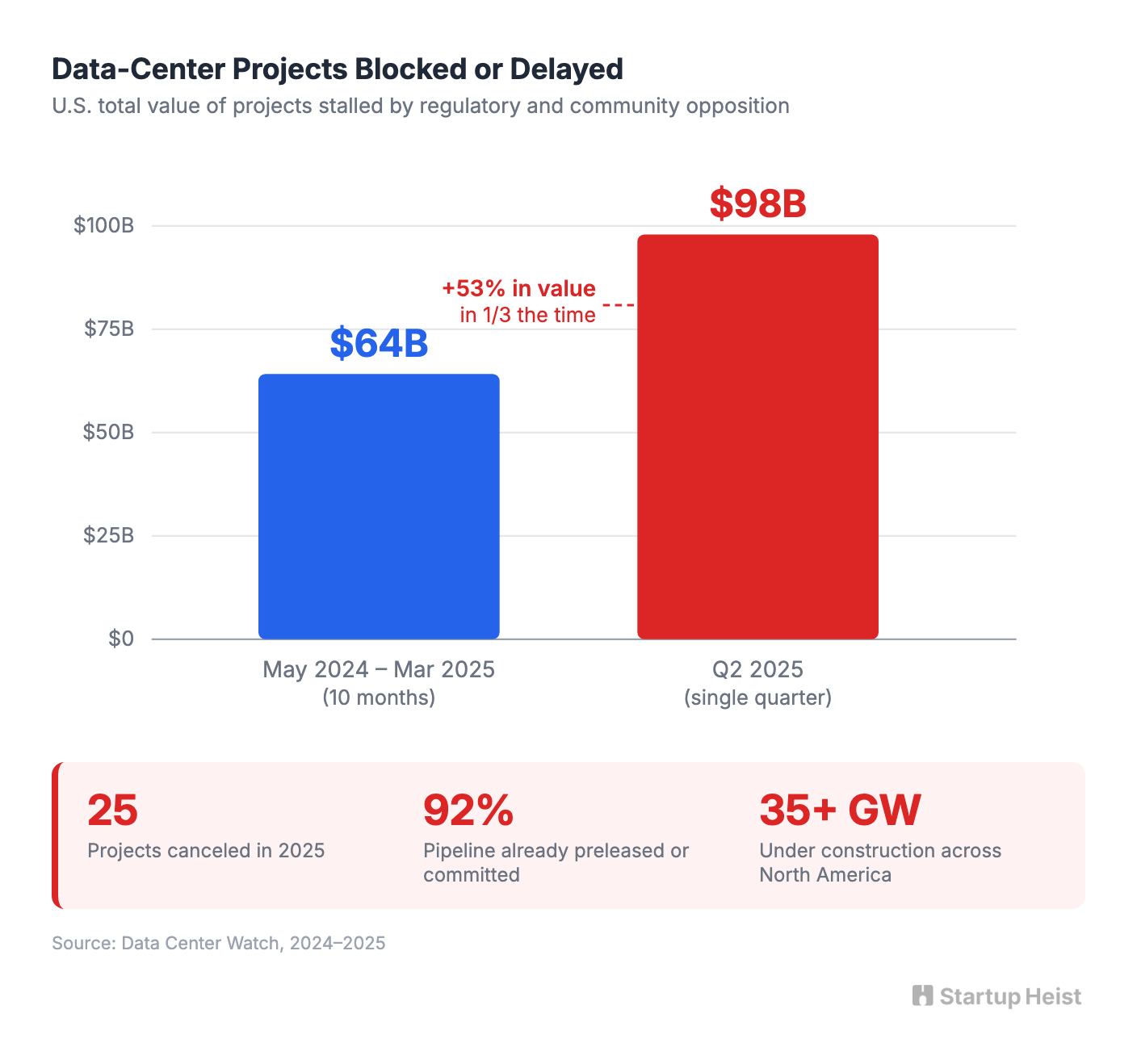

Data centers have graduated from a real-estate story into a county-board and planning-commission story. More than 35 gigawatts of capacity are under construction across North America, with 92% of that pipeline already preleased or committed. But the local processes that approve or kill these projects are slow, fragmented, and increasingly hostile. Data Center Watch tracked $64 billion in U.S. data-center projects blocked or delayed from May 2024 to March 2025. By Q2 2025, the blocked-or-delayed total climbed to $98 billion in a single quarter. Twenty-five projects were canceled in 2025 alone.

The opportunity is a gap between where the capital is flowing and where the information lives: a data-center permit and community-intelligence tracker for the Pennsylvania–Delaware–New Jersey corridor.

The money: 15 subscribers at $8K average ARR gets a solo founder to $120K. Institutional tiers run $2,500+/month.

Inside:

• Full MVP scope for one technical founder

• Core data model and object schema

• Four-cluster go-to-market with outreach

• Tiered pricing from $299 to $2,500+/mo

The Capital Collision

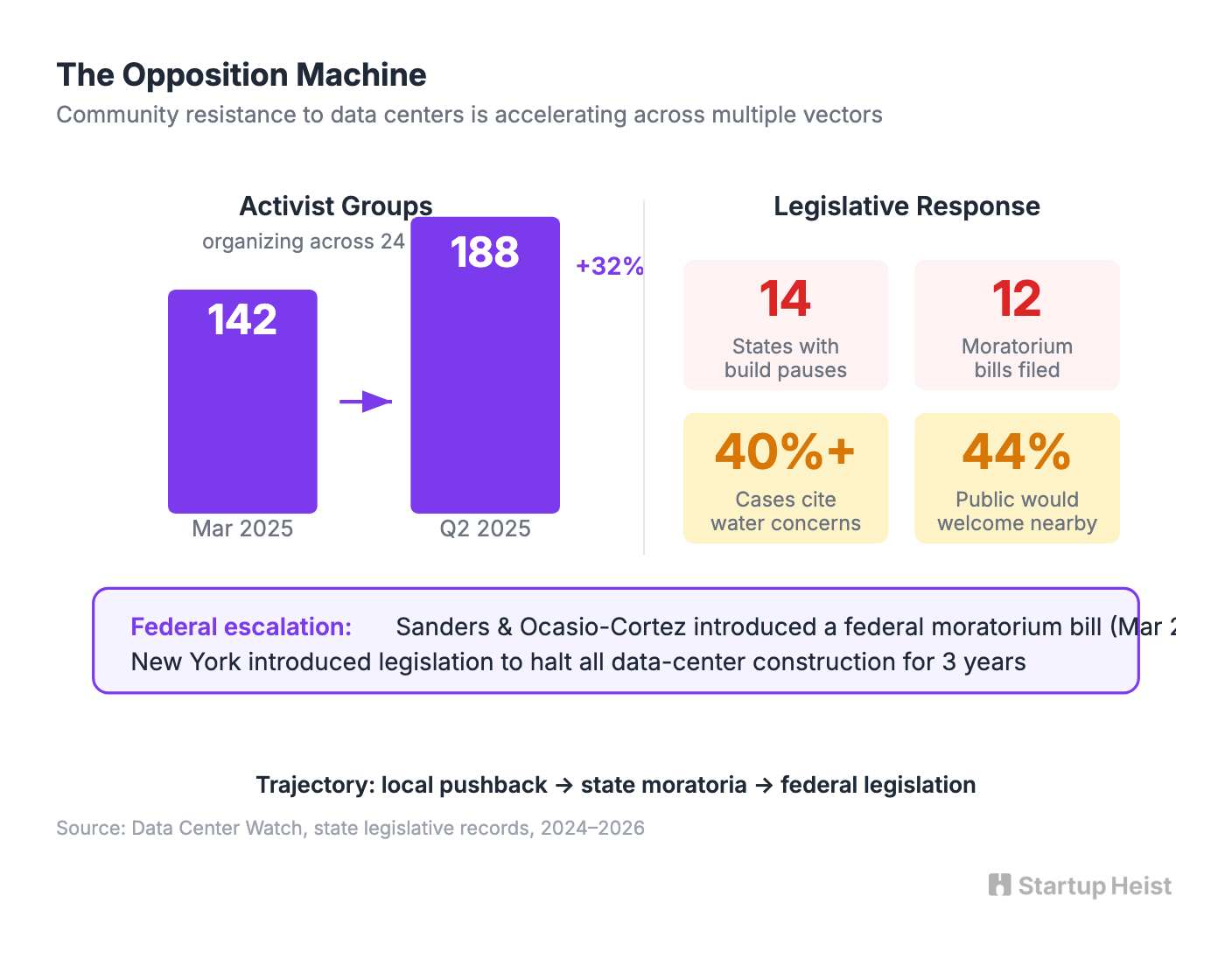

Communities are pushing back hard. Data Center Watch identified 142 activist groups organizing across 24 states by March 2025, with that number climbing to 188 groups by Q2 2025. Water use was cited in more than 40% of contested cases. Communities in at least 14 states have enacted temporary construction pauses. Twelve states filed formal moratorium bills in the current legislative cycle. New York introduced legislation to halt all data-center construction for three years. On March 25, 2026, Senators Sanders and Ocasio-Cortez introduced a federal moratorium bill. Only 44% of Americans would welcome a nearby data center.

The data behind all of this is technically public but economically inaccessible. County websites are inconsistent. Hearing notices are buried in agenda PDFs. Zoning changes are described in local planning language. Utility proceedings live in separate docket systems. Lawyers, investors, advocacy groups, and utilities all want the same four things: What's being proposed? Where is it in the process? What could stop it? What should I watch next?

Why This Corridor

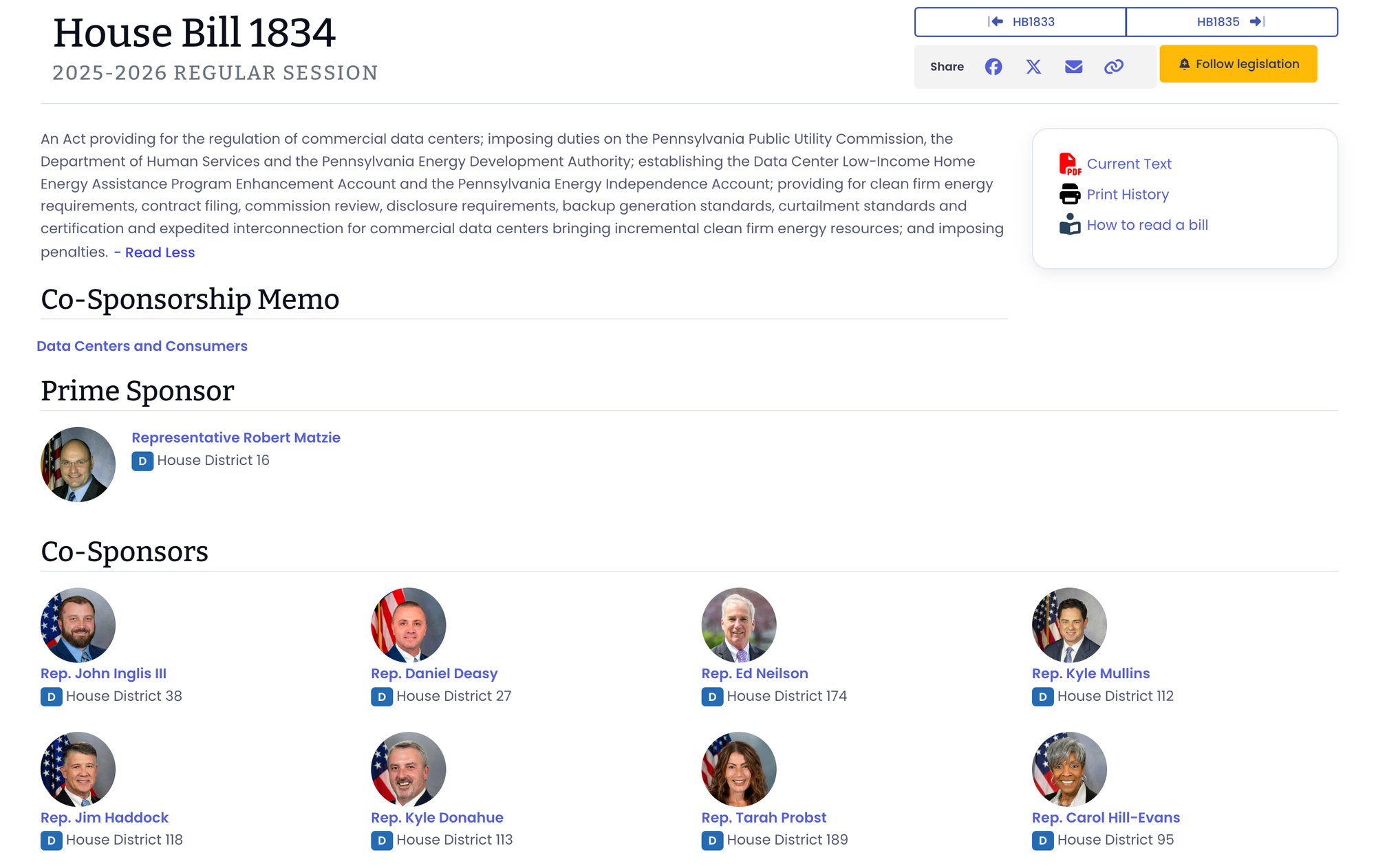

Pennsylvania is generating both project activity and formal regulatory structure at the same time. The state House voted 104–95 on March 24, 2026 to approve HB 1834, tasking the Public Utility Commission with regulating commercial data centers. The bill bars utilities from passing data-center infrastructure costs onto residents, requires operators to cover transmission upgrades, and mandates clean-energy sourcing starting at 10% in 2027, rising to 32% by 2035. Governor Shapiro's GRID standards, outlined on February 3, 2026, offer operators a voluntary framework: supply your own energy or pay for new generation, and in exchange unlock fast-track permitting and tax credits.

In Delaware, New Castle County unanimously approved data-center zoning regulations on March 11, 2026: 1,000-foot residential setbacks, a ban on open-loop cooling unless reclaimed water is used, energy-efficient generator mandates, and decommissioning requirements. The rules took effect on March 19, 2026 but exempt projects already in the pipeline. That distinction between grandfathered projects and new filings is exactly the kind of intelligence gap a tracking product would surface.

The corridor's density of land-use law firms, environmental groups, PJM-exposed utilities, infrastructure investors, and industrial real-estate operators means one intelligence product can serve multiple paying audiences from a single dataset.

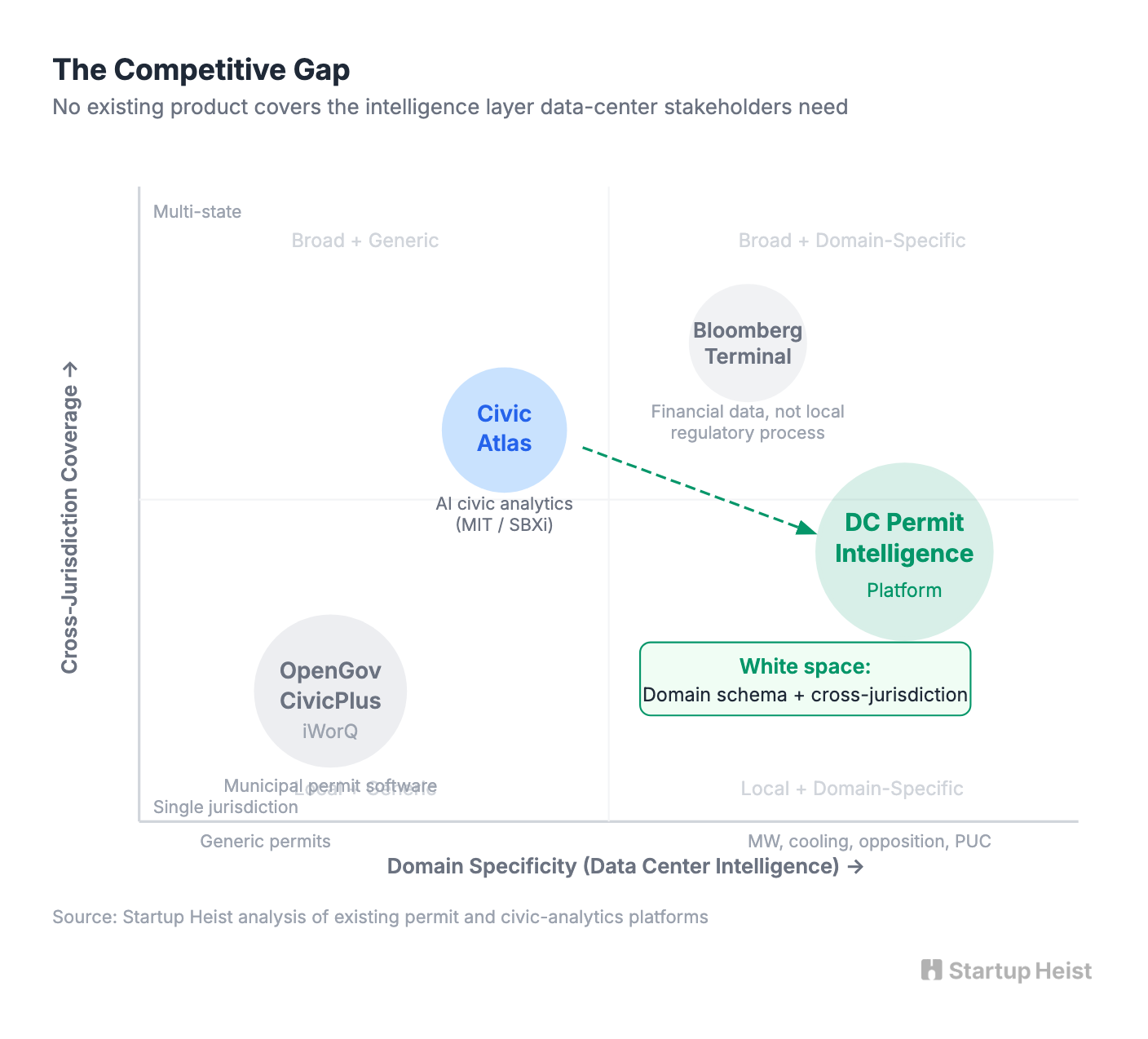

The Competitive Gap

Generic permit software (OpenGov, CivicPlus, iWorQ) serves municipalities managing internal applications. Civic Atlas, backed by MIT and SBXi, runs AI-powered civic-development analytics across building permits, zoning cases, and development activity. Neither product is tuned to the specific economics and politics of contested data-center siting across jurisdictions.

The value proposition is closer to Bloomberg than to GovTech. A paying customer doesn't care that you scraped a PDF. They care that you flagged something actionable: this project sits in a county where new setback rules just passed. This hearing matters because open-loop cooling is politically toxic here. This site may clear data center zoning but will face ratepayer scrutiny at the PUC. That requires a domain-specific schema tracking megawatts, cooling method, water source, interconnection status, tax incentives, data center opposition sentiment, and procedural milestones. The schema itself is the intellectual property.

Who Pays

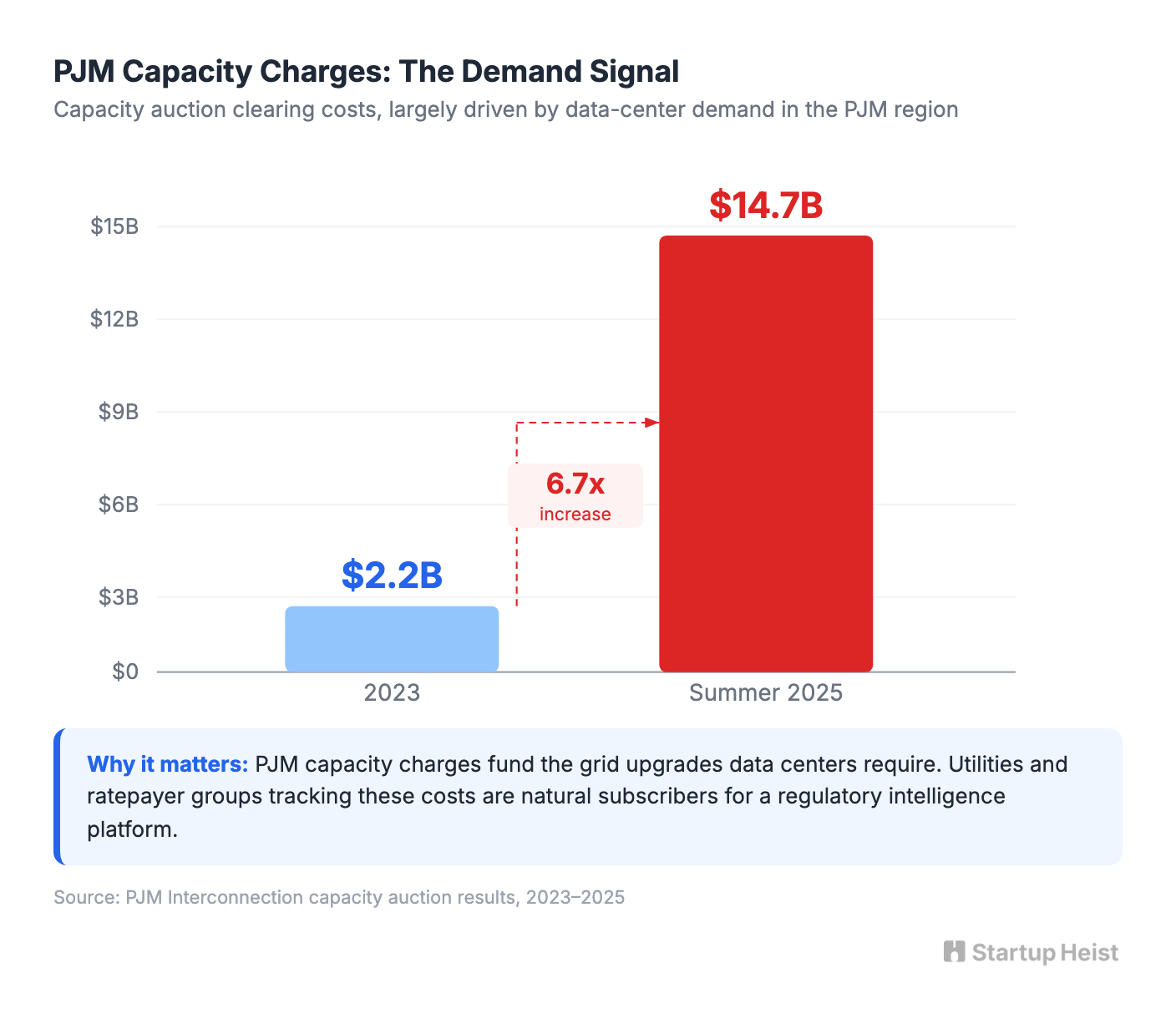

Regional law firms tracking zoning shifts and docket developments. Advocacy coalitions and ratepayer groups replacing manual spreadsheet monitoring. Utilities and regulatory-affairs teams watching PJM interconnection disputes (capacity charges hit $14.7 billion in summer 2025, up from $2.2 billion in 2023, largely driven by data-center demand). Infrastructure investors who can justify a subscription with one avoided site mistake. Large landholders near substations and industrial corridors whose underwriting depends on regulatory tracking intelligence. Local newsrooms that pay less but anchor distribution.

This is a narrow market with expensive pain. Ten to 25 organizations in the first corridor at $3,000 to $50,000+ per year gets to meaningful revenue without pretending this is a mass-market dashboard. Sign 15 customers at an average of $8,000 ARR and you're at $120,000. The larger platform case (extending from data centers to transmission, battery storage, peaker plants, crypto mines, logistics megaprojects) comes after the data model is proven. The shared pattern isn't "data centers." It's locally controversial capex moving through fragmented public processes.

The Playbook

MVP Scope (6–10 Weeks, One Technical Founder)

Build:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”