The Buyer's Radar: Turning TikTok Shop Into a Retail Sourcing Layer

In April 2026, a low-sugar gummy brand named Behave started rolling into almost 2,000 Target stores. A year earlier, the company was weeks from dying. The turn came from a single drop on TikTok Shop: Super Sour Skulls sold out in three days, a Target buyer saw the velocity, and the brand converted social proof into shelf space. Target is now carrying the Skulls as an exclusive SKU.

Read that sequence as a signal, not a feel-good founder story. It tells you how retail sourcing actually works in 2026, and it points to a gap in the market large enough to build a real software company inside. Here's the shape of it.

The money: 300 seats at $900/mo blended = $3M ARR. At 600 seats, meaningful territory. High-margin niche SaaS, not venture fantasy.

Inside:

• MVP: ranked weekly brief for one category

• Three-tier pricing: $499 / $999 / $1,499+

• Buyer outreach email that lands meetings

• Four moat layers, including relationship data

The Shift Nobody Built Software For

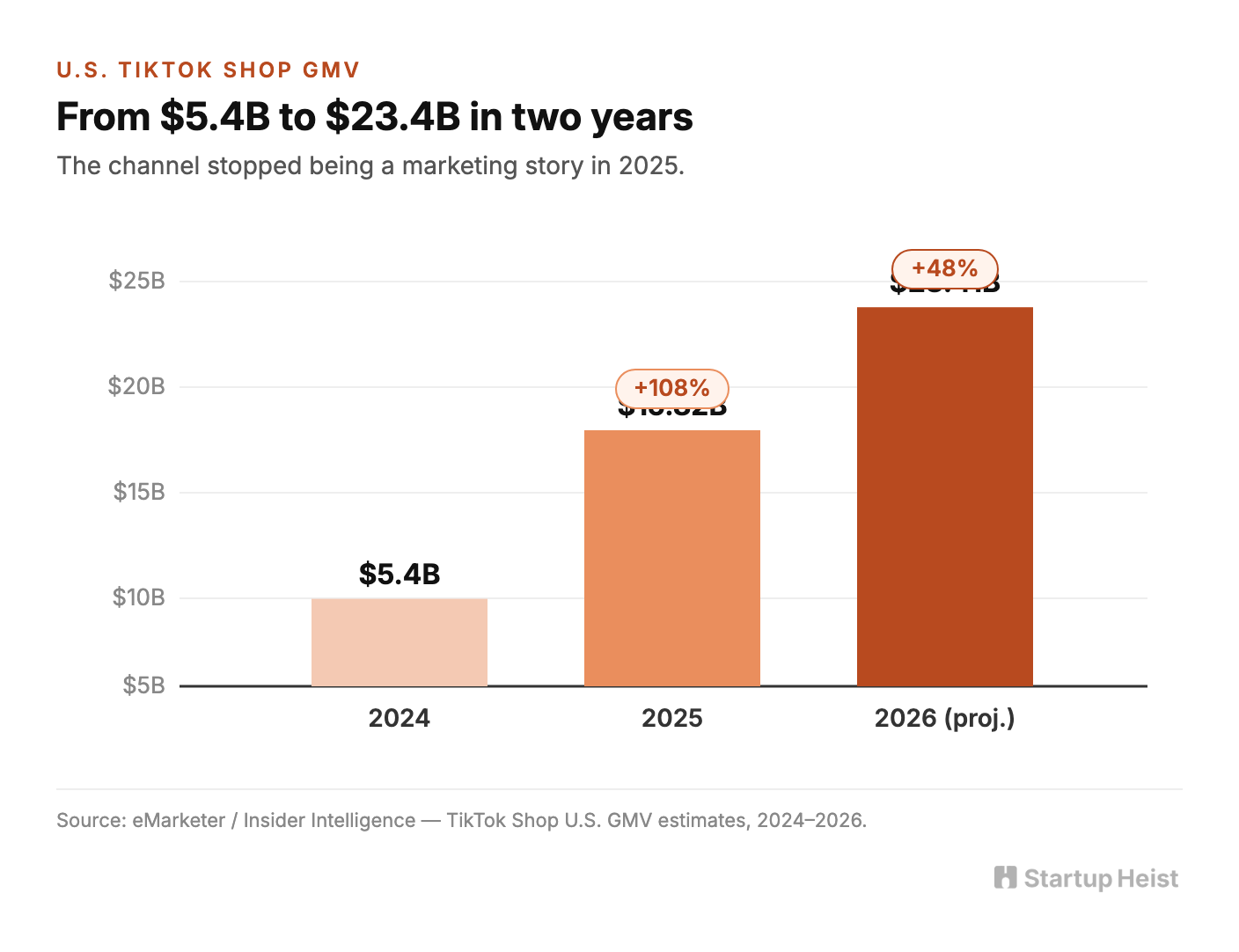

TikTok Shop is no longer a curiosity. U.S. sales will reach $23.41 billion in 2026, up 48% year over year, after growing 108% in 2025 to $15.82 billion. The platform already owns 18.2% of U.S. social commerce and is projected to hit one in four dollars by 2027. U.S. TikTok buyers are on track to climb from 53.2 million in 2025 to 57.7 million in 2026, crossing half of all U.S. social buyers. On Black Friday 2025, TikTok drove more than half of all shopper traffic across the MikMak platform, the single largest source of commerce discovery that day.

When that much transaction volume runs through one channel, the channel stops being a marketing story and becomes a demand-intelligence feed. What breaks on TikTok is no longer internet gossip. It's an early read on what consumers are about to pull off a shelf.

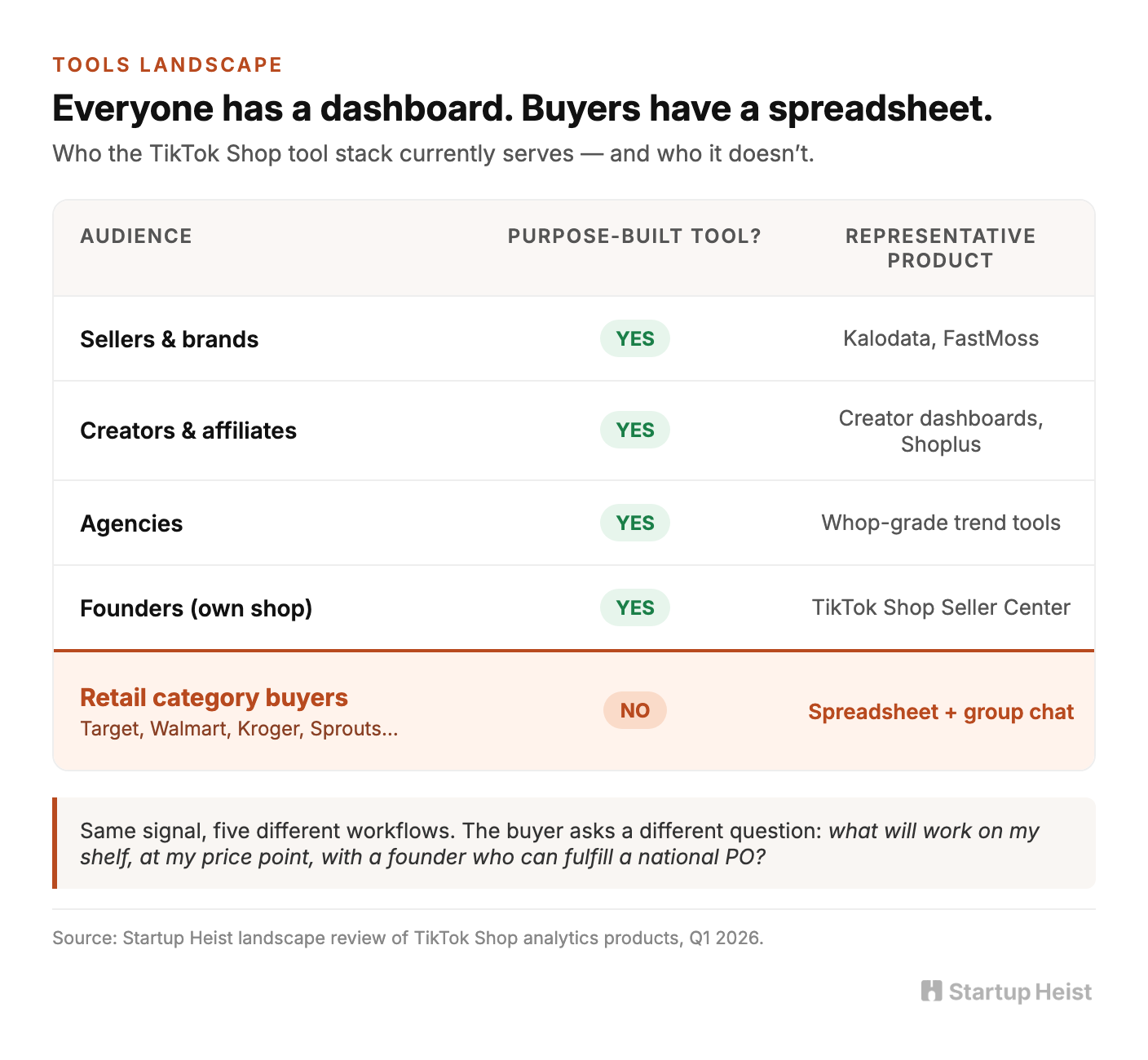

The people who need that read most are category buyers at Target, Walmart, Kroger, Albertsons, Sprouts, Whole Foods, and the strong regional chains, measured on how often they spot breakout brands before the chain across the street does. Retail buyer scouting used to live at trade shows, with brokers, and inside distributor rolodexes. Today, a category manager workflow includes reading short-form commerce signals — sell-through velocity, repeat creator mentions, comment sentiment, review counts, out-of-stock frequency — and buyers are doing it with a spreadsheet, a bookmark folder, and a group chat. The market moved. The software didn't.

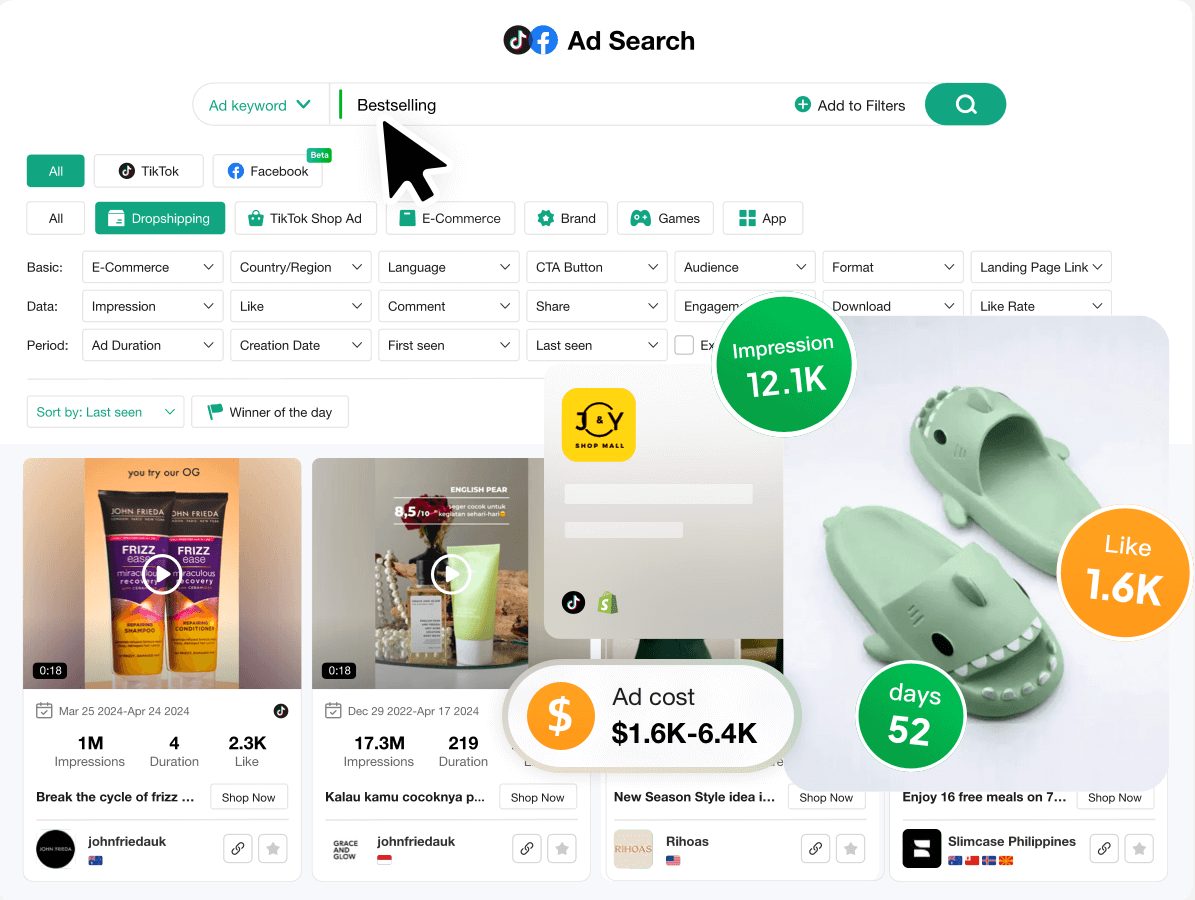

The natural assumption is that someone already built this. Kalodata and FastMoss are the obvious candidates, and they're real products with real data. FastMoss tracks over 500 million products across the U.S., U.K., and Southeast Asia. Kalodata refreshes every 15 minutes and benchmarks AOV inside sub-categories. Both are built for the seller side of the table. Their core question is which affiliate is selling, which product is converting, which video pulled its weight. That answers a marketing workflow. A category manager wants a filtered answer to a different question: what should I look at this week that will work in my category, at my price point, on my shelf, with a founder who can actually fulfill a national purchase order? Founders have TikTok Shop analytics. Agencies have creator tools. Influencers have dashboards. The buyer has screenshots. That asymmetry is the wedge.

The Product: A Trade Desk for Buyers

Position this as buyer prospecting infrastructure, not social commerce intelligence. The second framing sounds enterprise. The first sounds like a tool you expense on Monday.

Picture a trade desk. Not ad-tech bidding, but one screen a buyer opens in the morning and leaves 20 minutes later with five brands worth emailing. Ranked list. Short explanation per brand. Velocity sparklines. Price point. Review growth. Operational readiness flags. Founder contact. Export, track, or request an intro in one click. Less SaaS platform, more perfect scouting intern who read the internet so the buyer didn't have to.

Where the Moat Comes From

Raw TikTok Shop data won't defend this business. The official Shop API and Research API already expose shop rating, review count, item sold count, product pricing, and product sold count. Public trend surfaces are scrapable. If the product stops at data access, a seller tool can launch a buyer module the quarter it notices you.

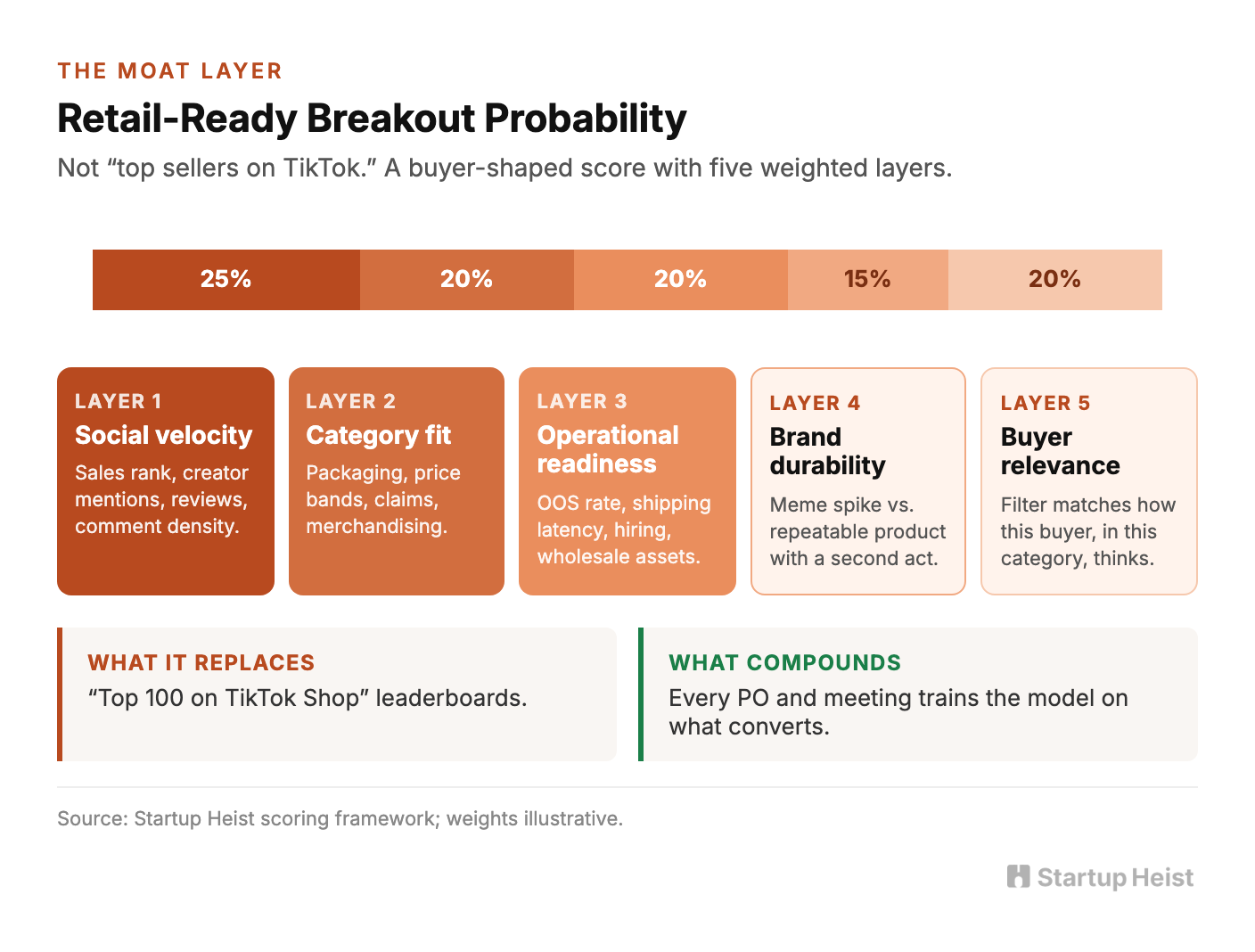

The moat lives one layer up, in how weak signals get synthesized into buyer-ready recommendations. The right model isn't top sellers on TikTok Shop. It's retail-ready breakout probability. That score layers:

- Social velocity. Day-over-day and week-over-week growth in sales rank, creator mentions, review count, comment density.

- Category fit. Packaging cues, price bands, claim language, flavor profile, size, merchandising compatibility with a given shelf.

- Operational readiness. Out-of-stock frequency, shipping latency, inbound response rate, hiring activity, founder LinkedIn footprint, distributor mentions, wholesale inquiry pages, retailer-facing asset quality.

- Brand durability. Meme spike with no second act, or a repeatable product broad enough to survive retail rotation?

- Buyer relevance. "Refrigerated beverages in the Northeast." "Better-for-you candy under 10 grams of sugar with Gen Z appeal." The filter thinks the way a buyer thinks.

That scoring layer is the defensible piece. It maps to the buyer's brain, not the seller's. There's a second moat inside the same system: relationship data. Once buyers use the tool, every meeting, sample request, and purchase order becomes training signal. Over time the product learns what trends into a PO, not just what trends. The feedback loop is hard to replicate because it requires buyers on the platform first.

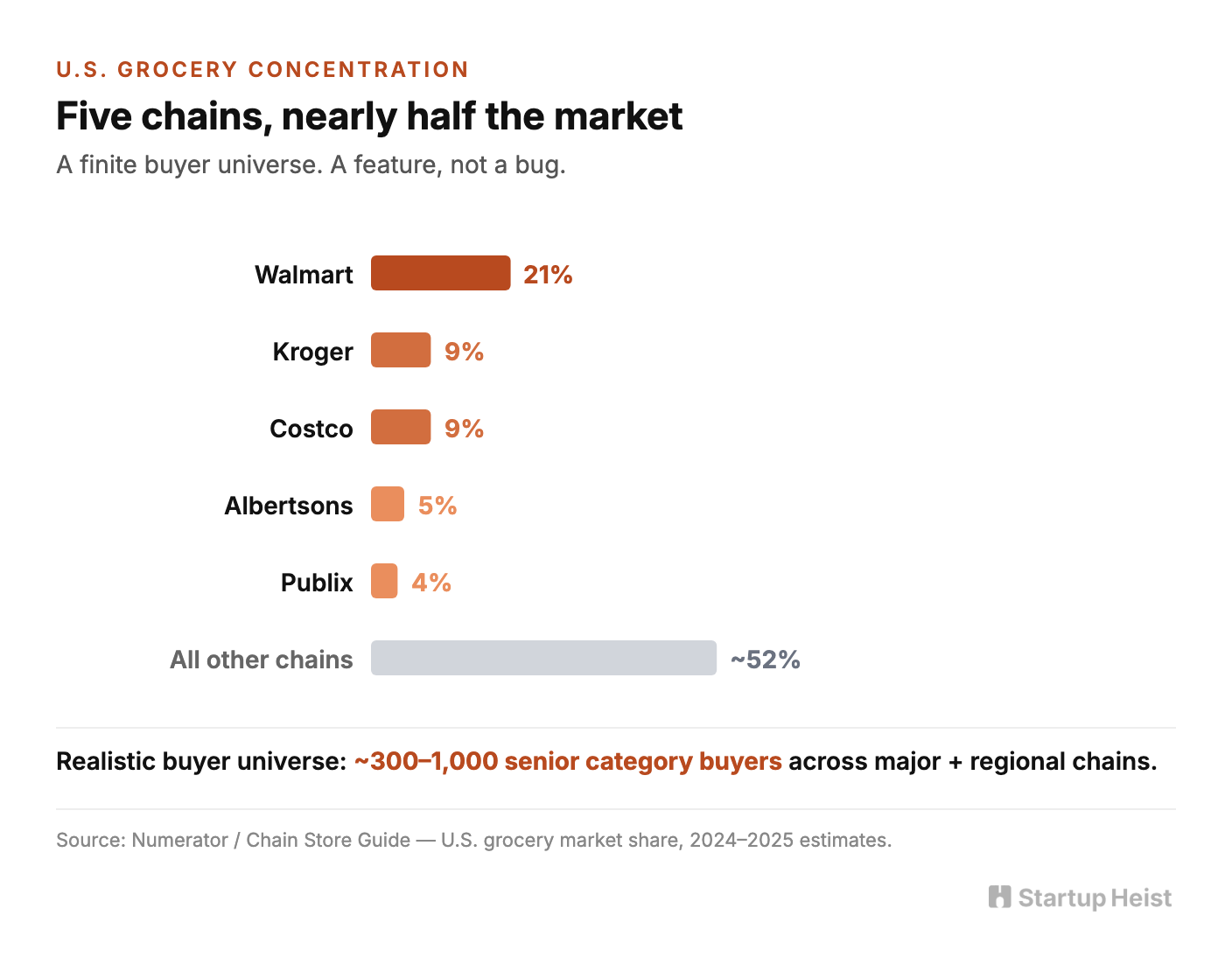

The TAM Is Small, and That Is the Point

U.S. grocery and mass retail is concentrated. Walmart commands roughly 21% of grocery market share, closer to 26% by some measures, with Kroger and Costco each near 9%, Albertsons around 5%, and Publix just above 4%. The realistic universe of senior category buyers across major chains, banners, and strong regional players is a few hundred to roughly a thousand seats. Brokers and distributor sourcing groups add another layer.

Finite, but more than enough. At 300 seats and a $900 blended monthly price, the business clears $3 million ARR. At 600 seats, it's in meaningful territory. This isn't a venture-scale monster in year one. It's a high-margin niche SaaS with a ceiling that rewards depth over breadth.

Finite TAM is a feature. It forces the go-to-market surgical. You don't need awareness. You need a handful of category managers who feel real pain around scouting quotas and competitive sourcing. The pitch isn't "adopt my analytics platform." It's "cut two hours a week and help you find one winner before Kroger does." That framing closes deals. The other one starts procurement reviews.

The MVP

Version one doesn't need to monitor the consumer internet. It needs to answer one workflow for one buyer persona inside one category.

Pick candy, snacks, or functional beverages. High-velocity categories where social proof travels fast and buyers are already conditioned to chase novelty. Ship a weekly report plus a dashboard that delivers the following:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”