Pop-Up Passport

There is a specific kind of retail gap in the U.S. right now, and it is bigger than it looks. American malls have figured out that more product isn't enough. They need formats that create urgency, novelty, and a reason to show up in person. South Korea is running a live demo of the next phase.

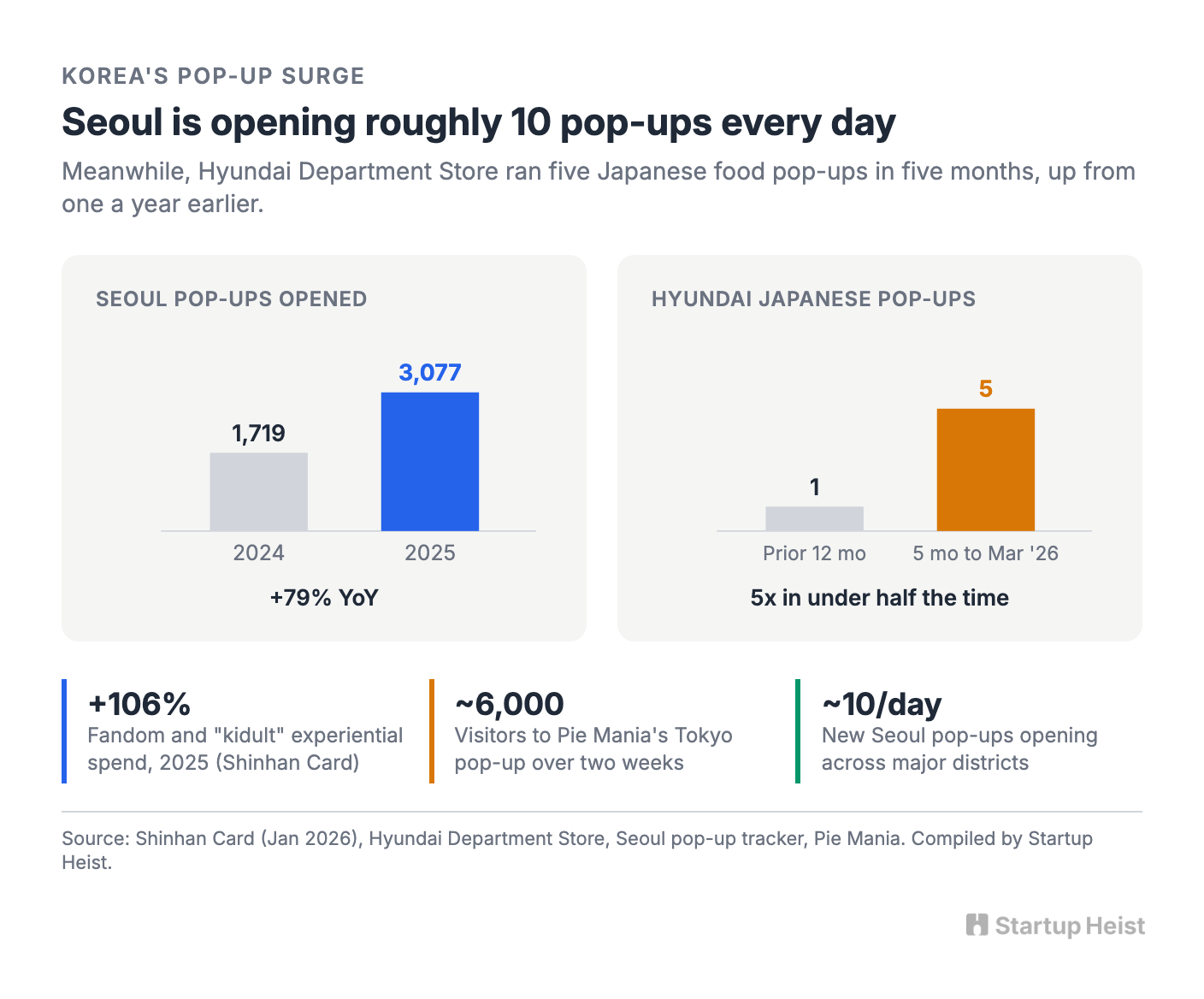

Shinhan Card reported in January 2026 that payments at fandom and experiential venues tied to anime, gaming, and "kidult" categories jumped 106% in 2025. Hyundai Department Store ran five Japanese food pop-ups in the five months through March 2026, up from one a year earlier. One Tokyo pie counter alone, Pie Mania, drew roughly 6,000 visitors over two weeks. Seoul's major districts opened 3,077 pop-ups in 2025, up 79% year-over-year — roughly ten new ones every day. Emotional retail is getting institutionalized.

America has the products. Pop Mart, now operating more than 40 U.S. locations as of early 2026 and opening 20 more at Simon malls this year including a flagship at King of Prussia, is pulling collectible revenue that would have been unthinkable three years ago. Sukoshi Mart is pushing toward 40 U.S. stores. Kiokii and… just planted its American flag at American Dream. Daiso crossed 167 U.S. locations. Olive Young, the Korean beauty giant, opens its first two American stores in May 2026 in Pasadena and at Westfield Century City, with a California logistics hub already built for broader rollout.

What the U.S. still doesn't have is the format: the limited-time Seoul dessert counter, the Tokyo stationery micro-world, the Osaka snack bar, the Kyoto craft demonstration, the fandom-heavy kidult scene that feels transportive for two weeks and then disappears. Shipping product is easy. Staging scenes is the harder craft, and that's where the moat lives.

Here's the opportunity:

The money: A founder running 6 to 12 activations a year across 3 to 5 properties can clear $20K to $50K+ per event between revenue share, marketing support, and ancillary programming, without opening a permanent store.

Inside:

• Operating MVP for one pop-up

• Three-bucket pricing and deal structure

• 90-day supply, property, and launch plan

• Outreach templates for malls and brands

• Unit economics and kiosk rent anchors

• Five red flags that sink first-timers

Why this works now

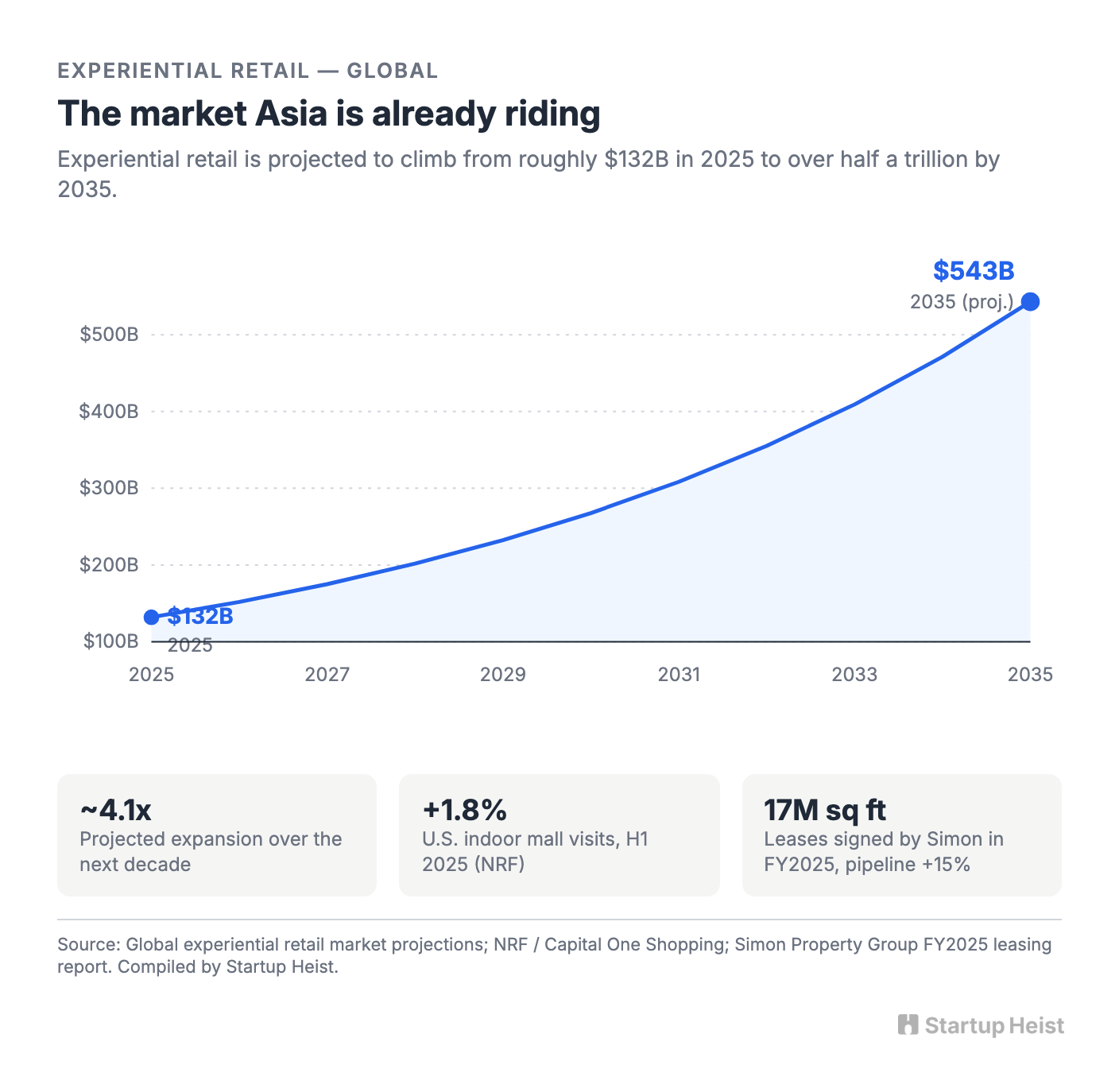

Landlords are productizing short-term retail. Simon markets specialty leasing across pop-ups, carts, kiosks, and inline spaces and calls its operator roster "the finest retail pop-up store operators in the U.S." Brookfield offers the same with terms as flexible as "a few days to one or two years." ICSC has profiled specialty leasing teams quadrupling their brand-sponsorship revenue and lifting ancillary income 150% in two years, with Federal Realty growing ancillary revenue 500% over a decade. Non-traditional leasing is no longer a side budget.

Strong indoor malls are busier than the obituary suggests, even as the broader sector contracts. Capital One Shopping data cited by NRF shows indoor mall visits up 1.8% in the first half of 2025, with visit durations up 3.3%. Simon booked 17 million square feet of leases in fiscal 2025 with a pipeline 15% above the prior year. Louis Vuitton's Pietro Beccari called retailtainment "the future of retail," and Mall of America's Jill Renslow framed the upside bluntly: the retailers who lean into bold experimentation will build lasting loyalty. The delta between A-malls leaning into experience and everything else is widening, and that's precisely where this business lives.

The supply side in Asia is maturing at the same time. Korea's "feelconomy," the emotion-first consumption shift Seoulz identified as the country's defining consumer macro for 2026, is pushing small, aesthetically tight brands to look overseas for their next audience. Hyundai's Japanese pop-up program and Seoul's ten-a-day pop-up cadence are the live proof-of-concept. Kpop Nara ran a pop-up at Mall of America, generated enough demand to announce a permanent 2026 lease, and handed the entire industry a working template. The U.S. doesn't need to invent experiential retail. It needs someone who can translate it.

What you are actually selling

Call it "importing cute products from Asia" and you've already lost the plot. You're selling four things at once:

- To the mall: traffic, novelty, press, and social content.

- To the brand: U.S. market entry without opening a store.

- To the customer: a temporary ritual, not just merchandise.

- To yourself: a distribution position between foreign brands and American real estate.

That last line is the whole business. Anyone can import SKUs. Fewer people can source culturally resonant brands, negotiate temporary rights, coordinate freight, localize merchandising, and package the result into something a U.S. specialty leasing manager can greenlight in a week. The asset you're building isn't inventory. It's deal flow plus repeatable format translation.

The best initial wedge

Start narrow. Very narrow. "All Asian experiential retail" is too broad operationally and too fuzzy commercially. Pick one of three wedges:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”