The Beef Squeeze Is Quietly Opening a New Procurement Category

The beef story is being misread.

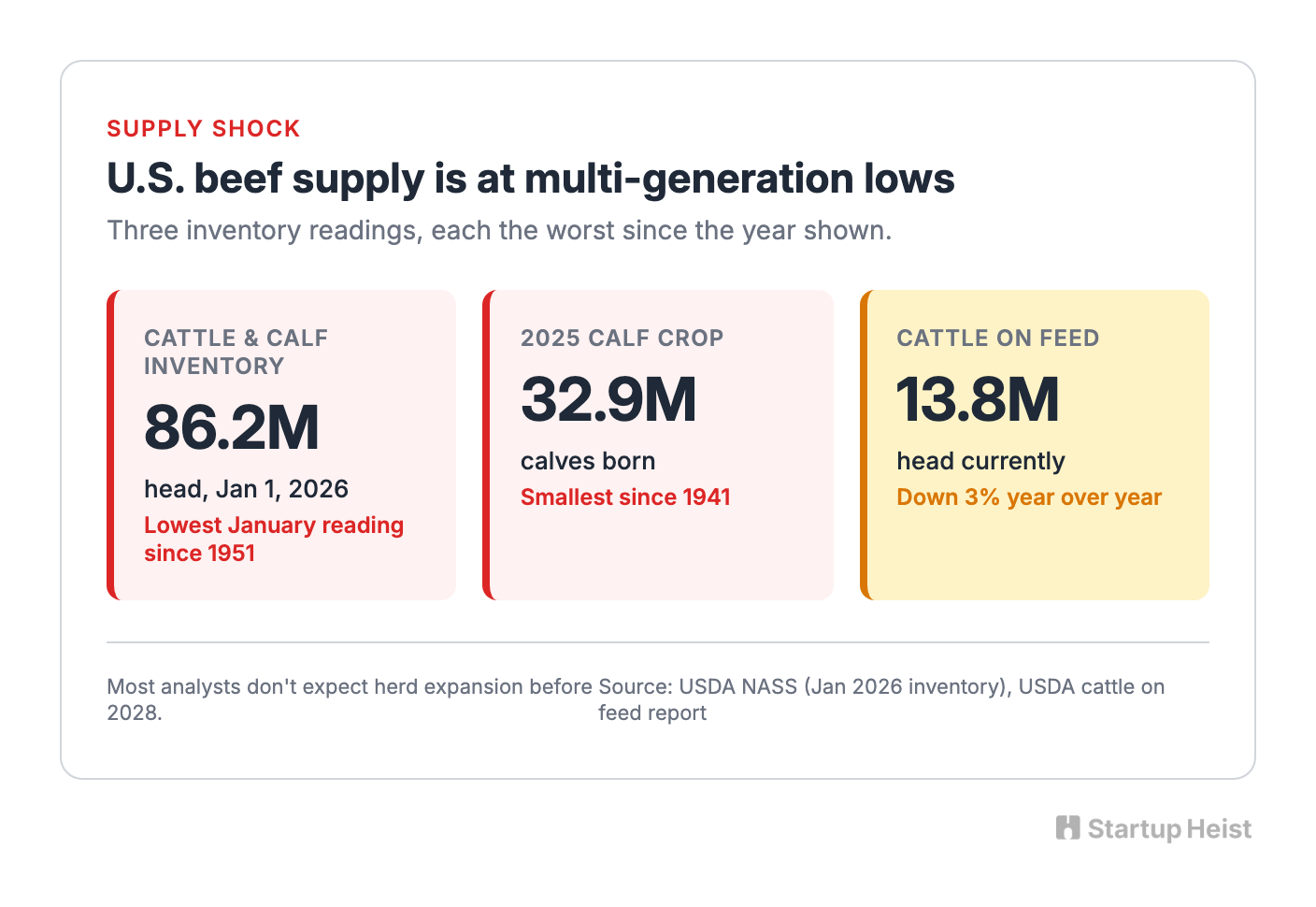

Most coverage flattens it into one headline: beef is expensive. The real story is structural. U.S. cattle and calf inventory fell to 86.2 million head as of January 1, 2026, the lowest January reading since 1951. USDA pegged the 2025 calf crop at 32.9 million, the smallest since 1941. Cattle on feed sit at 13.8 million, down 3% year over year. None of those numbers snap back next quarter. The cycle is still contracting, and most analysts don't expect herd expansion before 2028.

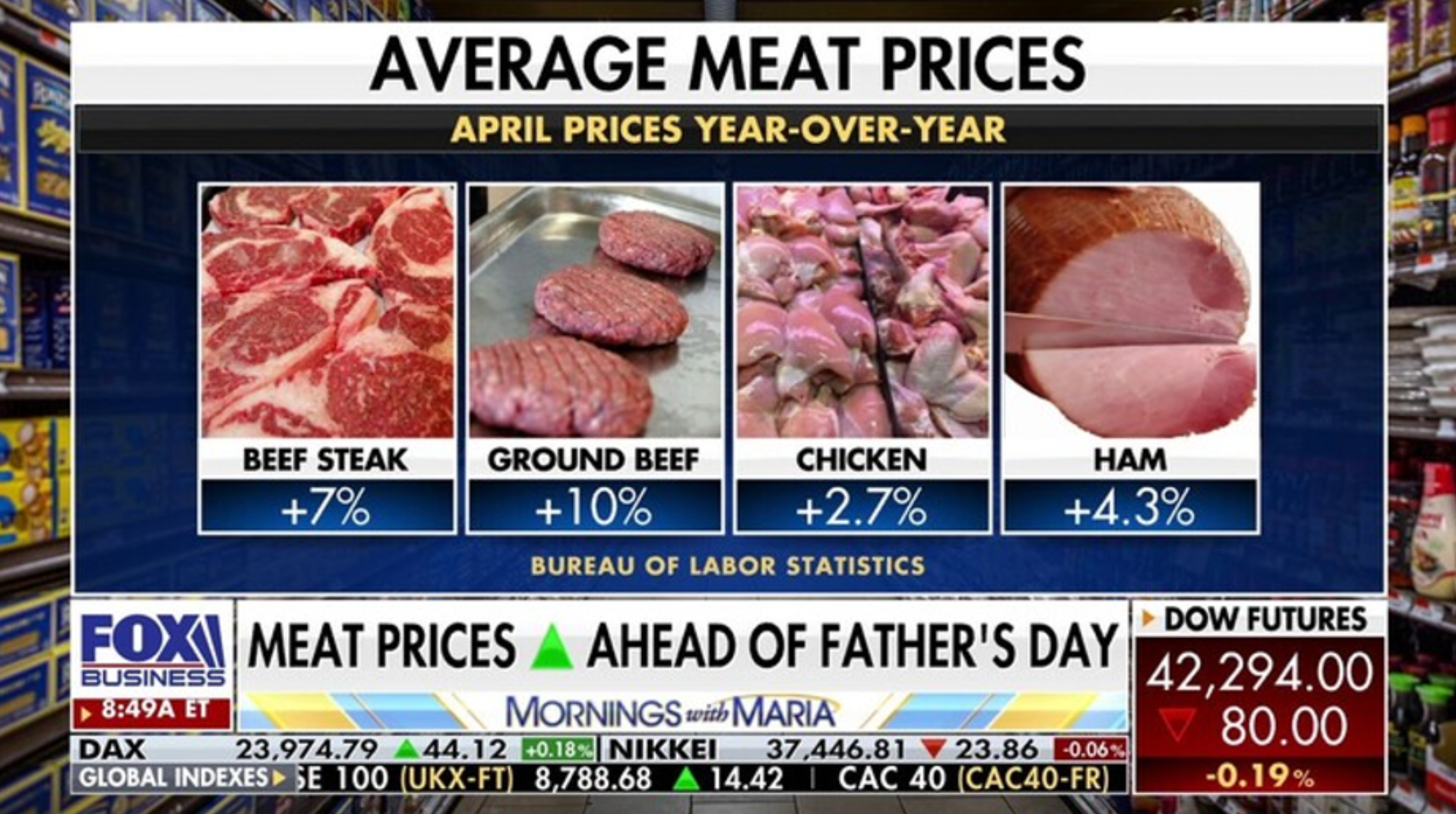

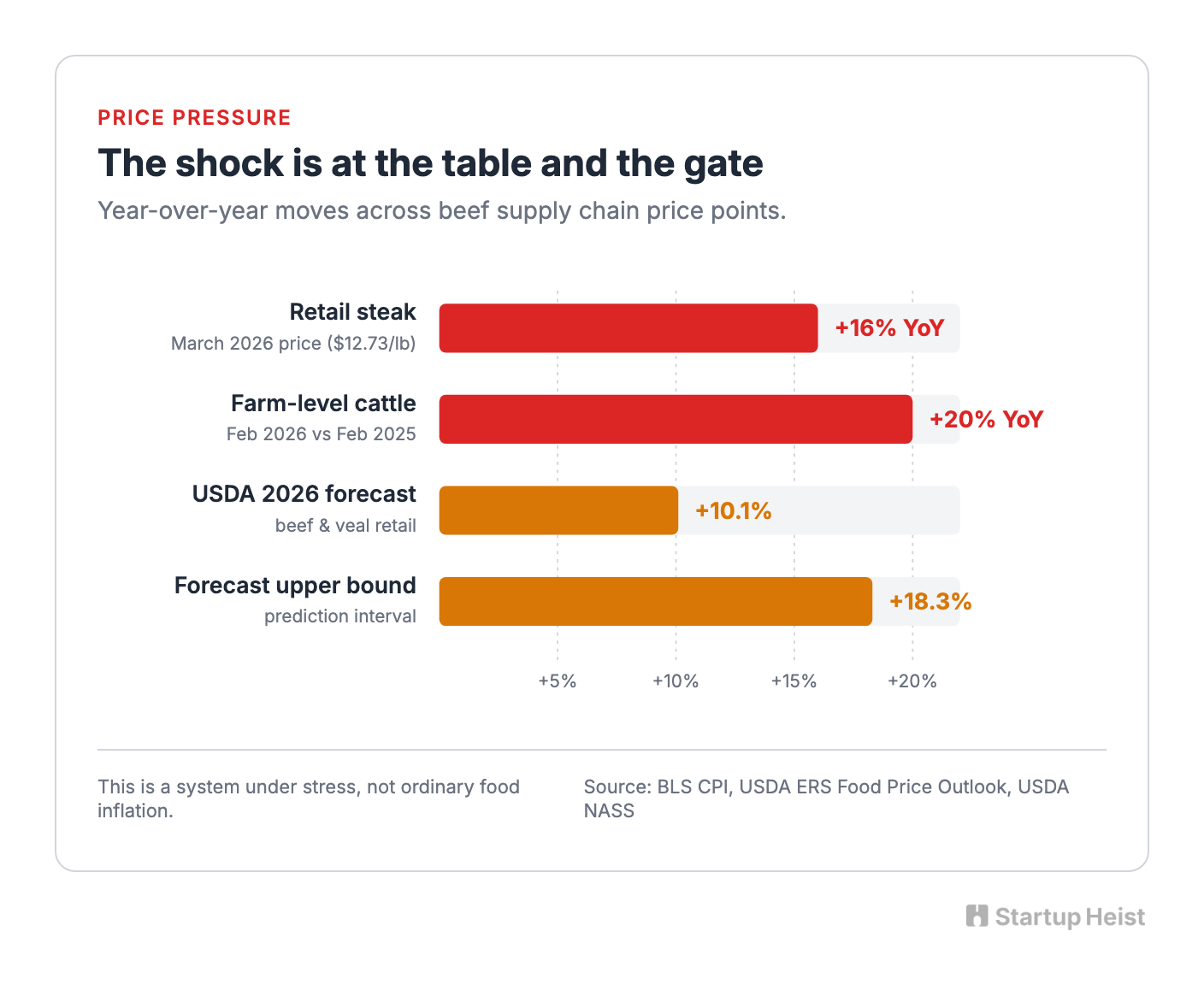

The shock has already reached the table. Uncooked beef steak prices hit $12.73 per pound in March 2026, up 16% year over year. USDA's Economic Research Service forecasts another 10.1% jump in beef and veal retail prices in 2026, with a prediction interval running as high as 18.3%. Farm-level cattle prices in February 2026 ran 20% above the prior February. This is a system under stress, not ordinary food inflation.

Here's the opportunity:

The money: 120 steak-forward independents at $349–$799/month = $42K–$96K MRR on core SaaS alone, before the 1–2% success fee on matched volume.

Inside:

• 8–12 week MVP scope on a boring stack

• Three-tier pricing with success-fee add-on

• Cold email templates for chefs and ranchers

• 120-day launch playbook by region

Where the Pain Collects

When a supply chain gets squeezed this hard, the weakest link in the middle fails first. In American beef, that link is the independent restaurant running a serious steak program without the scale to dictate terms to a distributor.

801 Restaurant Group filed Chapter 11 on April 10, 2026, citing beef cost pressure and softer sit-down demand. The filing listed roughly $18.7 million in liabilities and followed the closure of 801 Fish in Denver and 801 On Nicollet in Minneapolis. Eleven days earlier, on March 30, 2026, Sysco announced a $29.1 billion deal to acquire Jetro Restaurant Depot, a cash-and-carry operator with 166 warehouse stores across 35 states serving more than 725,000 independent restaurants. The Independent Restaurant Coalition asked the FTC to block the deal on April 1 and collected more than 700 operator signatures within twenty-four hours.

One steakhouse group breaking and one distributor getting much larger aren't isolated events. They map where bargaining power is moving: away from small, price-sensitive restaurants, and toward the players who control supply.

The Software That Stops Too Early

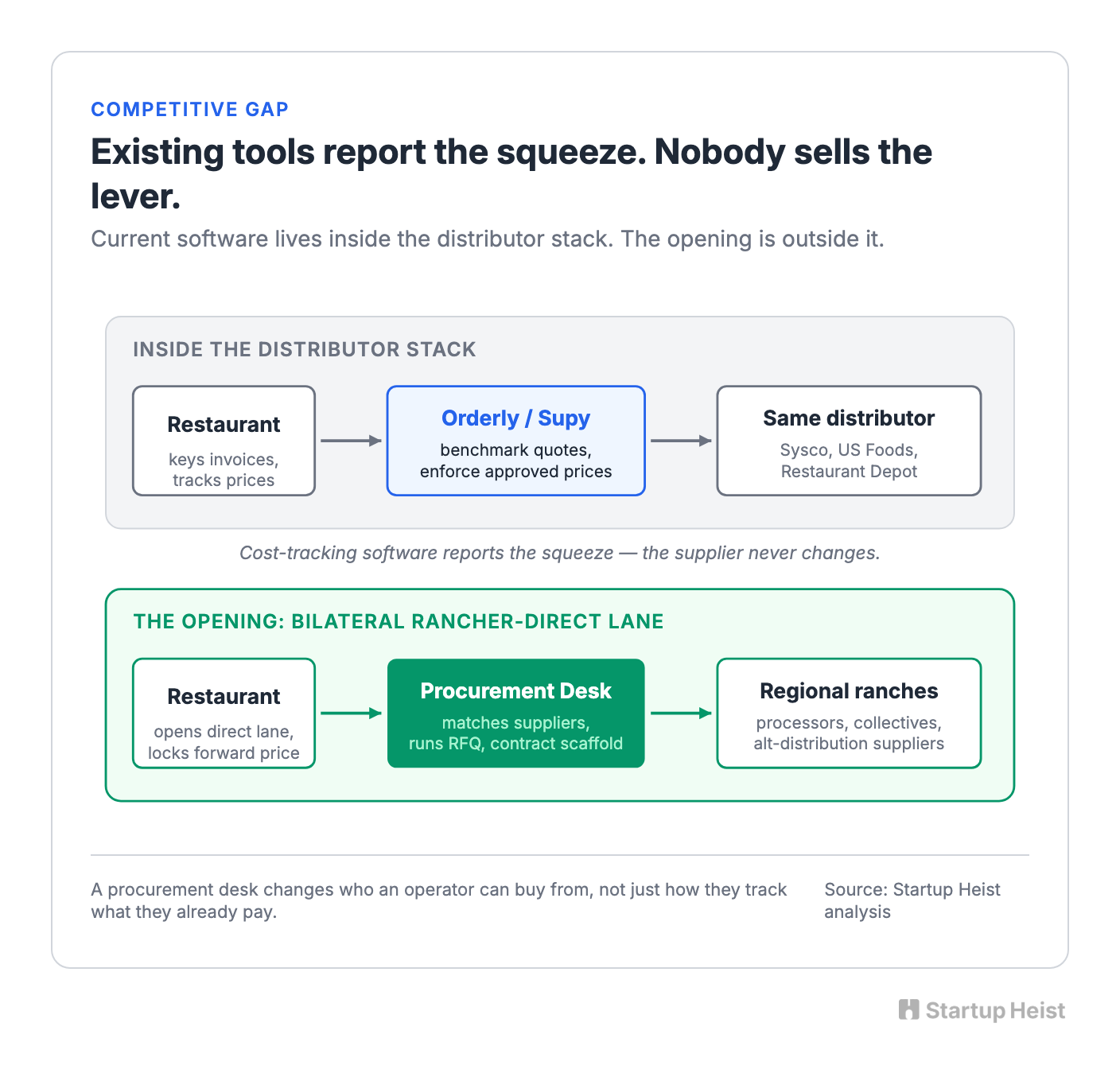

Independent restaurants aren't flying blind. Tools exist. Orderly digitizes invoices, builds a price index from hundreds of common ingredients, and lets operators benchmark quotes against local and national averages. Supy enforces approved prices across orders, flags invoice discrepancies in real time, and runs enterprise-grade approval workflows for multi-branch operators. Both are useful. Both solve the wrong half of the problem for this moment.

Every platform in the category sits inside the existing procurement stack. They tell an operator, with increasingly good data, that the price being paid is high. What they don't do is change who the operator can buy from, or help lock supply at a fixed price before the next basis move. Cost-tracking software reports the squeeze. Nobody is selling the lever.

That gap is the opening.

The Shape of the Play

The opportunity isn't a consumer beef subscription, and it isn't another general-purpose procurement dashboard. It's a procurement desk for independent restaurants that buy meaningful volumes of beef, feel every basis-point move in protein cost, and are too small to get strategic attention from Sysco or US Foods.

The product has three jobs. Compare distributor quotes against live market signals and local historicals. Surface a curated set of regional ranches, processors, and alternative suppliers who can actually fulfill restaurant demand. Provide the workflow to open a direct lane, structure a bilateral forward-buy, and manage it without turning the startup into a regulated commodities broker.

In one sentence: show a chef whether the strip loin quote is fair, show a regional alternative, tell them whether to lock now or wait two weeks, and run the RFQ. Restaurant operators don't want futures theory. They want fewer ugly surprises on Thursday night service.

Why a Wedge, Not a Terminal

The best version of this business isn't Bloomberg Terminal for beef. That sounds impressive and sells poorly. The best version is narrow enough to explain to a chef in ninety seconds.

Geography is the wedge. Launch in cattle-heavy states where transport economics favor regional supply and where buying direct from a ranch or processor is already culturally legible: Texas, Kansas, Nebraska, Oklahoma, and likely Colorado and Missouri. In those markets you're not inventing behavior. You're making a messy workflow more visible, more comparable, and more repeatable.

Protein is the second wedge. Start with beef. Volatility is obvious, margins are painful, and operator attention is already locked on it. Once the workflow is stable for beef in one region, the same rails extend to lamb, pork, seafood, and seasonal produce contracts. Beef is the beachhead, not the ceiling.

The Moat Is Not the Dashboard

The dashboard won't be the moat. The moat is the combination of transaction memory, a local supply graph, and operator trust.

After twelve months of running the loop, a single question becomes unanswerable for anyone outside the system. Which restaurants are price-sensitive versus quality-sensitive? Who buys ribeye versus ground versus mixed programs? Which suppliers deliver consistently? Which regions experience basis blowouts and when? Which direct deals actually renew? Orderly and Supy see what happens inside the restaurant. A procurement desk sees what happens between fragmented buyers and fragmented suppliers when markets get ugly. That dataset eventually underwrites financing, insurance, and embedded services.

There's also a counter-positioning advantage against distribution consolidation. The Sysco and Restaurant Depot combination, which isn't expected to clear regulators until fiscal Q3 2027, strengthens the case for an independent tool that preserves optionality for small operators. A startup doesn't beat Sysco by being bigger. It wins by becoming the independent restaurant's negotiating layer.

The Honest Ceiling

This isn't a huge TAM-on-day-one SaaS. It's a sharp vertical tool with real expansion paths. A disciplined solo founder or small team can build this into a high-six-figure or low-seven-figure ARR business before deciding whether to broaden into a more ambitious marketplace or financing layer. That restraint is part of the appeal. The business doesn't require a fantasy to work.

The MVP

Version one needs five things:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”