Build the Poor Man's QSIC

Dollar General is expanding AI-enabled, measurable in-store audio across 12,000 stores through QSIC by Q2 2026, tying that network to point-of-sale data, real-time ad targeting, and closed-loop reporting that meets IAB verification standards. QSIC closed a $25 million Series B in January 2025 and is deploying more than 70,000 speakers across North America. At 7-Eleven, QSIC powered the Gulp Radio rollout across 5,000-plus stores, with reported 5 to 9% overall sales lifts. This is the industrialization of physical-store attention.

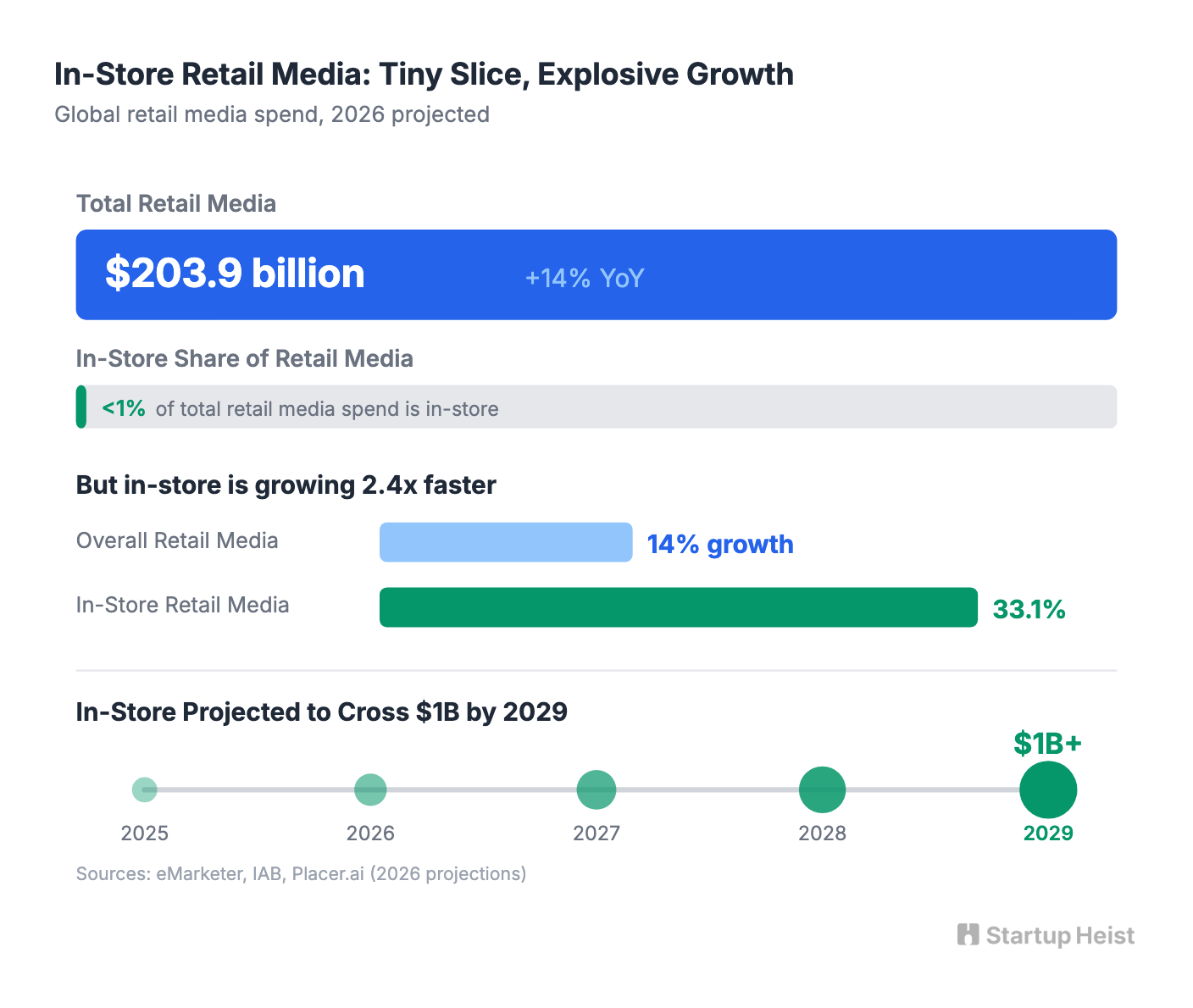

The retail media market is expected to hit $203.9 billion globally in 2026, growing 14% year over year. In-store retail media is climbing even faster at 33.1% growth, yet it still represents less than 1% of total U.S. retail media spend. Analysts project in-store will cross the billion-dollar mark by 2029. Everyone sees this working. Almost nobody has productized it for the businesses that need it most.

The opportunity is underneath the enterprise tier.

The money: 50 convenience stores at $199/month = $10,000 MRR from SaaS alone, before media revenue.

Inside:

• Full MVP scope and pricing strategy

• Best first customers by vertical

• Three-layer revenue model breakdown

• Cold outreach template included

Forget building another QSIC. Build the poor man's version for small chains and strong independents: convenience stores with 5 to 50 locations, regional pharmacies, garden centers, car washes, quick-service operators with captive dwell time. A dead-simple system that turns existing speaker infrastructure into programmable retail media: house ads, vendor-funded promos, localized spots, dayparted campaigns, and basic measurement tied to sales windows. The goal is helping overlooked retailers monetize the attention they already own.

Why This Market Exists

The enterprise tier is consolidating fast. QSIC powers Dollar General, 7-Eleven, and McDonald's. Vibenomics, acquired by Mood Media in March 2023, partnered its network with Stingray Advertising to form the largest U.S. in-store audio advertising network: over 25,000 locations reaching 800 million monthly shoppers, including Kroger, Albertsons, and Safeway. These players sell scale, attribution, and programmatic insertion to national CPG brands.

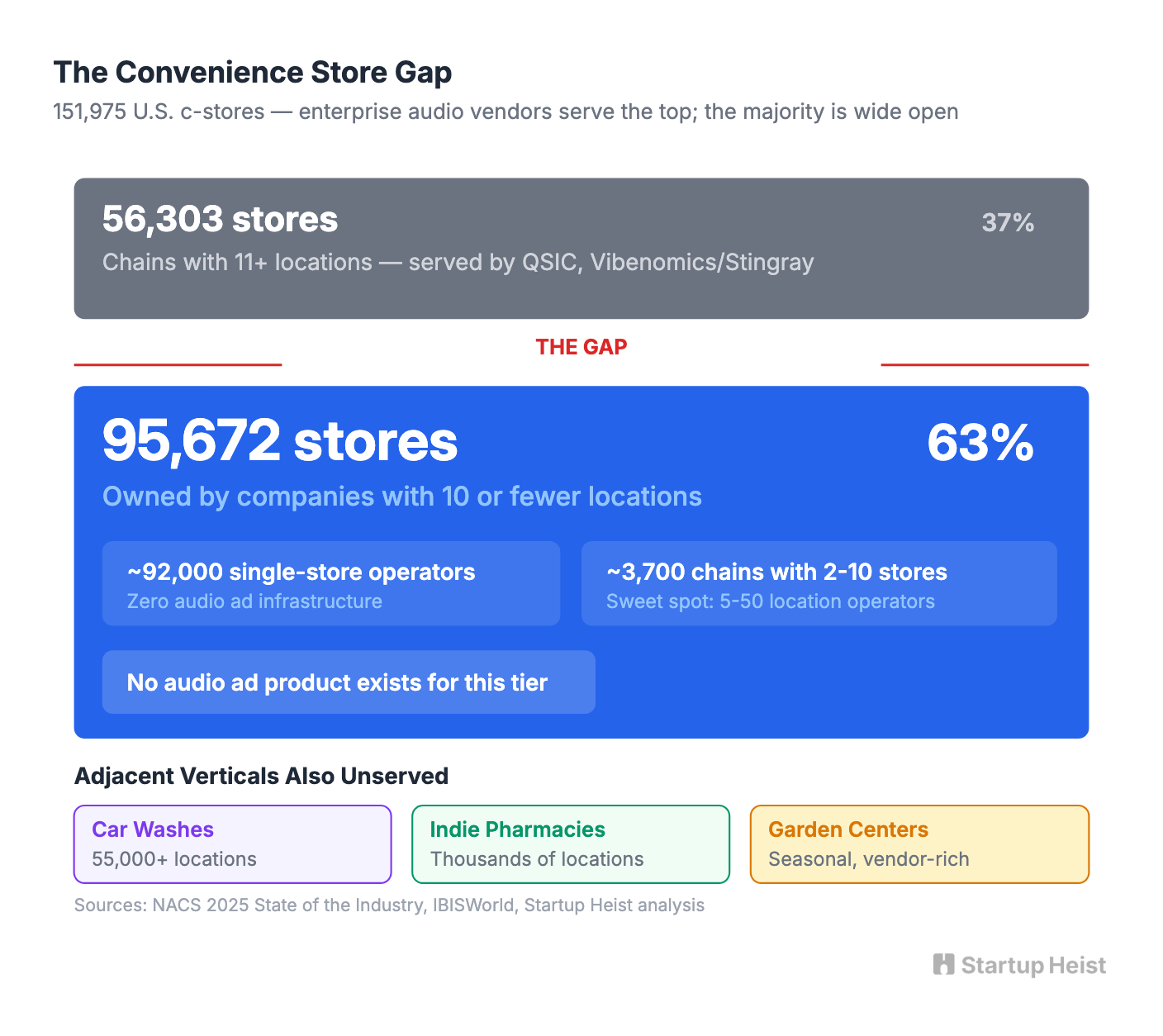

The majority of physical retail operates below that threshold. The U.S. convenience store industry alone counts 151,975 locations. Of those, 95,672 are owned by companies running 10 stores or fewer. Nearly 92,000 are single-store operators. Add 55,000-plus car washes, thousands of independent pharmacies, and countless garden centers: the long tail of physical retail is enormous, fragmented, and structurally invisible to enterprise audio vendors. These operators already spend on promotions through flyers, Facebook, local radio, vendor co-op, and direct mail. A five-store convenience chain already runs seasonal specials. A pharmacy already does flu-shot reminders. A car wash already upsells memberships. What none of them have is a simple way to convert the in-store attention they already own into something they can measure, repeat, and sell.

Why Now

Dollar General's rollout validates three things at once. Retailers now view in-store audio as retail media infrastructure, not background ambiance. Point-of-sale linkage turns audio from a branding toy into a measurable channel. And 7-Eleven's Gulp Radio results prove the use case works in high-traffic, operationally messy retail environments where staff turnover is constant and tech sophistication is low.

Meanwhile, 76% of purchases still happen in physical stores and 40% of media buyers now deploy retail media across the entire shopping journey. The format has crossed from experimental to inevitable. The enterprise players are consumed with enterprise-scale coordination, and a simpler, SMB-shaped product can slip underneath.

The fast play is a lightweight audio scheduling and ad-creation tool for small retailers who already have speaker systems. The strategic play is accumulating merchant data, campaign history, vendor relationships, and daypart performance, then stitching together a mini retail media network across neglected physical categories.

The Real Product

Don't overbuild this.

Position the first version as in-store audio OS for independents. Avoid the adtech or AI media infrastructure labels. They scare buyers and invite the wrong expectations.

Version one needs five things:

Audio scheduling. A store owner or district manager schedules house messages and paid promos by location, daypart, and campaign window. This replaces the current approach at most small retailers, which ranges from someone pressing play on a Bluetooth speaker to a forgotten CD from 2019.

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”