Most consumer health giants own brands, shelves, and trust. They don't own all the molecules. That gap is the heist.

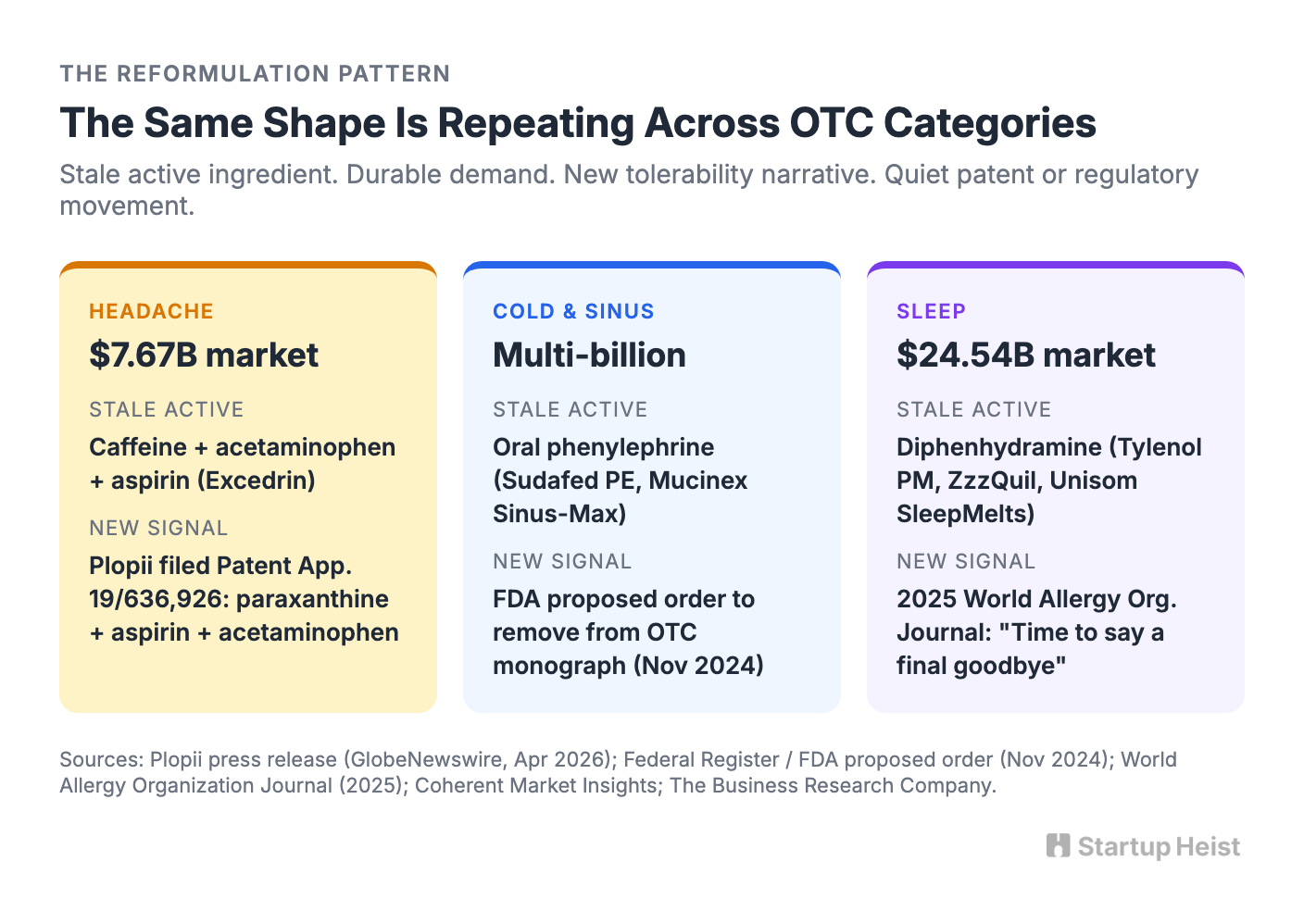

On April 24, 2026, a small biotech called Plopii filed U.S. Patent Application 19/636,926 with the United States Patent and Trademark Office. The application contains 40 claims. The covered formulation pairs paraxanthine with aspirin and acetaminophen. It's, in essence, a caffeine-free structural rethink of the Excedrin-style headache pill, and the press release positions it as the first new structural approach to OTC headache relief in decades. The pitch is straightforward. Consumers want the relief pattern of a caffeine-enhanced analgesic without the jitteriness, sleep disruption, dependency, and rebound headache that come with caffeine itself.

One filing rarely changes a category. This one matters because it points at something larger: OTC categories are enormous, trusted, and weirdly stale. Pain relief, sleep aids, antacids, allergy, cough and cold. The shelves are full of multibillion-dollar brands built around active-ingredient combinations that often feel older than the consumer behavior around them. Excedrin still means acetaminophen + aspirin + caffeine. OTC sleep still leans on sedating antihistamines like diphenhydramine and doxylamine. Acid reflux is still dominated by H2 blockers and PPIs that haven't meaningfully evolved in a generation. Brands have evolved. Packaging has evolved. Marketing has evolved. The active-ingredient logic hasn't.

Here's the opportunity:

The money: A founder-led intelligence shop with 40 paid seats across the $499 and $1,250 tiers clears roughly $35K MRR before any studio-tier deals.

Inside:

• Sleep-first MVP scope and dossier blueprint

• Three-tier pricing from $499 to $7,500

• Founder-led GTM with full outreach scripts

• The ontology moat that compounds weekly

That asymmetry creates a very specific opportunity: build a reformulation arbitrage intelligence tool for indie OTC founders, supplement entrepreneurs, private-label CPG operators, consumer health investors, and brand studios. Not a drug company, not a supplement brand, not a regulatory consultancy. A radar.

The product watches FDA OTC monographs, USPTO patent filings, PubMed research, Amazon category data, and legacy formulations to answer one commercially valuable question: which large OTC category is still built on an old formulation, has known consumer complaints, and now has credible research or patent activity around a better-tolerated alternative?

That's a very expensive, very specific question. The people who need the answer will pay $499 to $2,499 a month if the signal is good.

The Pattern Is Already Repeating

The Plopii filing is one data point. The same shape shows up in three other categories right now, and that's what makes the radar timely.

In November 2024, the FDA issued a proposed order to remove oral phenylephrine from the OTC monograph after concluding the ingredient isn't effective at standard doses. That order has not been finalized. The comment period closed May 7, 2025, and a final order is required before manufacturers must reformulate or pull product. The decongestant sits inside Sudafed PE, Mucinex Sinus-Max, daytime cold formulations from Tylenol and Advil, and dozens of private-label products. Every major manufacturer, including Kenvue, Procter & Gamble, Reckitt, and Bayer, now faces a forced reformulation cycle on a category worth billions in annual retail sales. The writing is on the wall. Whoever moves first with a credible substitute owns shelf space the incumbents are about to vacate.

In acid relief, the precedent already played out. After the FDA requested removal of all ranitidine products in April 2020 over NDMA contamination, demand for famotidine surged so sharply that Canada and the United States both reported sustained shortages between September 2019 and December 2021. Brands and private-label operators that had famotidine inventory and a story captured the migration. The PPI category barely moved. The opening was inside the H2 blocker shelf and lasted for years.

In sleep, the substrate is older but the pressure is higher. A 2015 study in JAMA Internal Medicine found a 54% increase in dementia risk for the heaviest users of strongly anticholinergic drugs, including diphenhydramine. A 2021 Cochrane systematic review reinforced the link. The American Geriatrics Society lists first-generation antihistamines on its Beers Criteria as potentially inappropriate for older adults. A 2025 review in the World Allergy Organization Journal, titled "Diphenhydramine: It is time to say a final goodbye," argued explicitly that the active has reached the end of its life cycle and now represents a comparatively greater public health hazard within its class. The ingredient is still in Tylenol PM, Advil PM, ZzzQuil, Sominex, Unisom SleepMelts, and roughly every store-brand OTC sleep aid in America.

The pattern is consistent across all of these. Stale active ingredient. Durable consumer demand. New safety or tolerability narrative. Quiet patent and research movement around a better-tolerated alternative. A handful of brands worth billions still parked on top of it. Multiply that by a dozen categories and the opportunity is obvious.

Why The Window Is Open Now

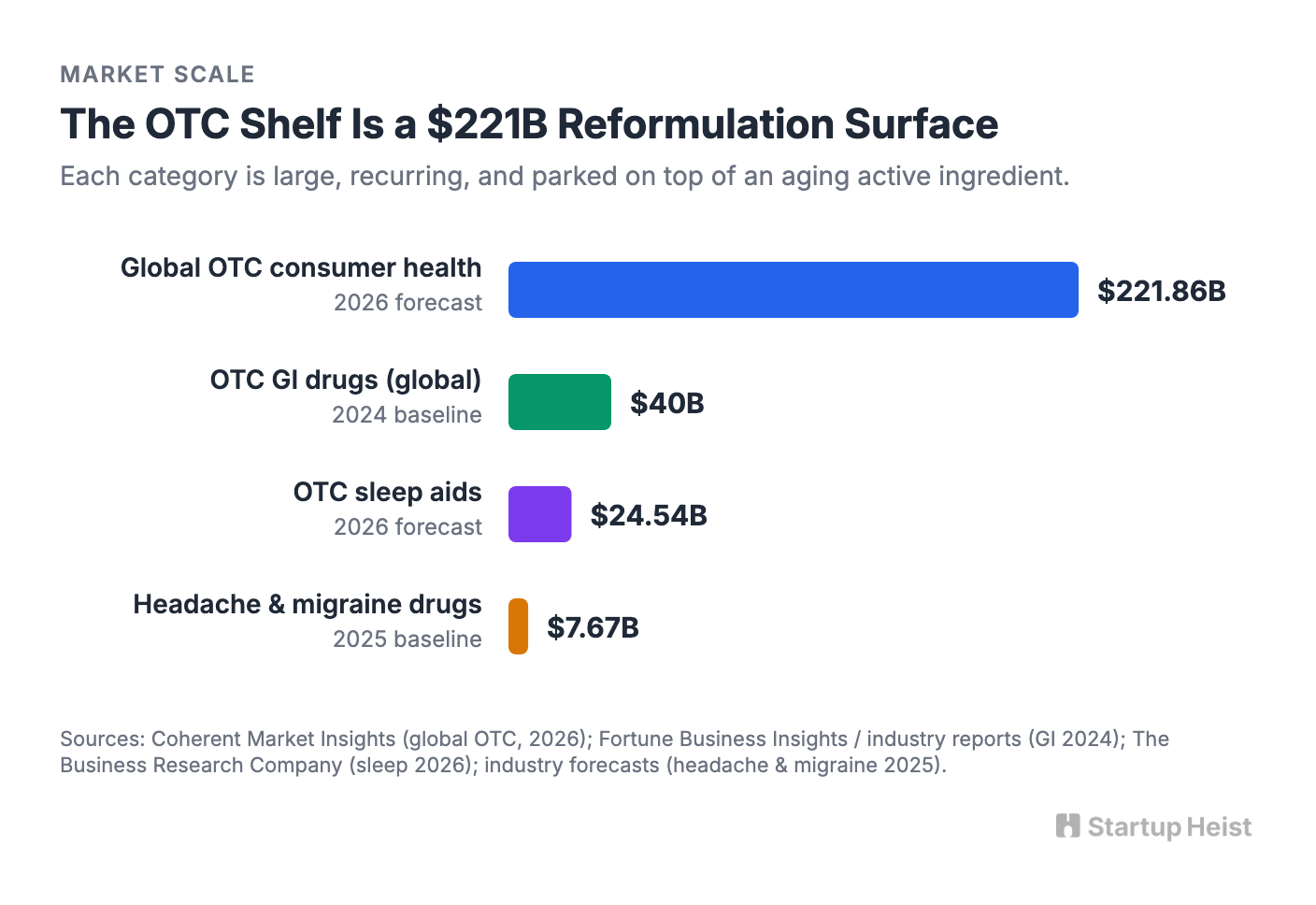

The OTC market isn't a niche. The Consumer Healthcare Products Association reports that OTC medicines save the U.S. healthcare system more than $167 billion a year by keeping minor ailments out of clinics and emergency departments. Globally, OTC consumer health is forecast to reach $221.86 billion in 2026 and grow to roughly $304 billion by 2033.

The OTC sleep category alone is projected to grow from $22.69 billion in 2025 to $24.54 billion in 2026 at an 8.1% CAGR, with melatonin now holding around 30% of revenue share by ingredient. Headache and migraine drugs were a $7.67 billion category in 2025 and are projected to grow to over $20 billion by 2035. The gastrointestinal OTC drugs segment cleared $40 billion globally in 2024.

These aren't soft markets. Consumers buy headache medicine, sleep aids, heartburn relief, cold medicine, allergy pills, and digestive remedies repeatedly. They don't need to be educated that the problem exists. They already self-medicate. They already trust the OTC shelf. They already search Amazon at midnight when something hurts, burns, itches, or keeps them awake. That makes reformulation unusually powerful. The customer isn't being asked to adopt a strange new behavior. The pitch is "you already buy this, here is a version that fixes the thing you dislike about the old one." That message converts.

Two structural shifts make the timing real.

The first is the regulatory environment. The CARES Act of March 2020 added section 505G to the Federal Food, Drug, and Cosmetic Act and replaced the old monograph rulemaking process with a faster administrative-order system. Industry can now submit OTC Monograph Order Requests, or OMORs, directly to FDA. The Over-the-Counter Monograph Drug User Fee Amendments were reauthorized for fiscal years 2026 through 2030 and signed into law in November 2025. FDA received its first industry OMOR in fiscal 2024, a sunscreen ingredient request from DSM Nutritional Products, with a goal date in April 2026. The system isn't purely theoretical anymore.

The second is data accessibility. FDA Monographs@FDA exposes monograph status and active ingredient detail. USPTO patent data is structured and queryable. PubMed and NCBI APIs are robust. Amazon retail data is brittle but workable through third-party tools. The entire category is now monitorable in a way it has never been before, and monitorable markets create data products.

What This Product Actually Is

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”