The Scam Firewall for Aging Parents

The best elder-fraud startup is not an antivirus app. It is a family-configured interruption layer that steps in during the ten minutes when a scammer is trying to move money.

A man calls your mother and says he works for her bank. There has been suspicious activity on her account. Her savings are in danger. She has to act now.

He knows her name. He knows where she banks. The number on her screen looks legitimate. He is calm, patient, professional. When she hesitates, he transfers her to a second "fraud specialist" who walks her through exactly how to protect her money. The safe move, he explains, is to withdraw it and move it somewhere secure.

This is how high-value fraud actually works. Manufacture an emergency, isolate the victim, fake authority, and keep her on the line until the money is gone. Artificial intelligence has made every part of that cheaper. A single operator can now generate flawless scripts, run long automated conversations, clone a familiar voice from a few seconds of audio, and launch hundreds of attempts without staffing a call center full of skilled manipulators.

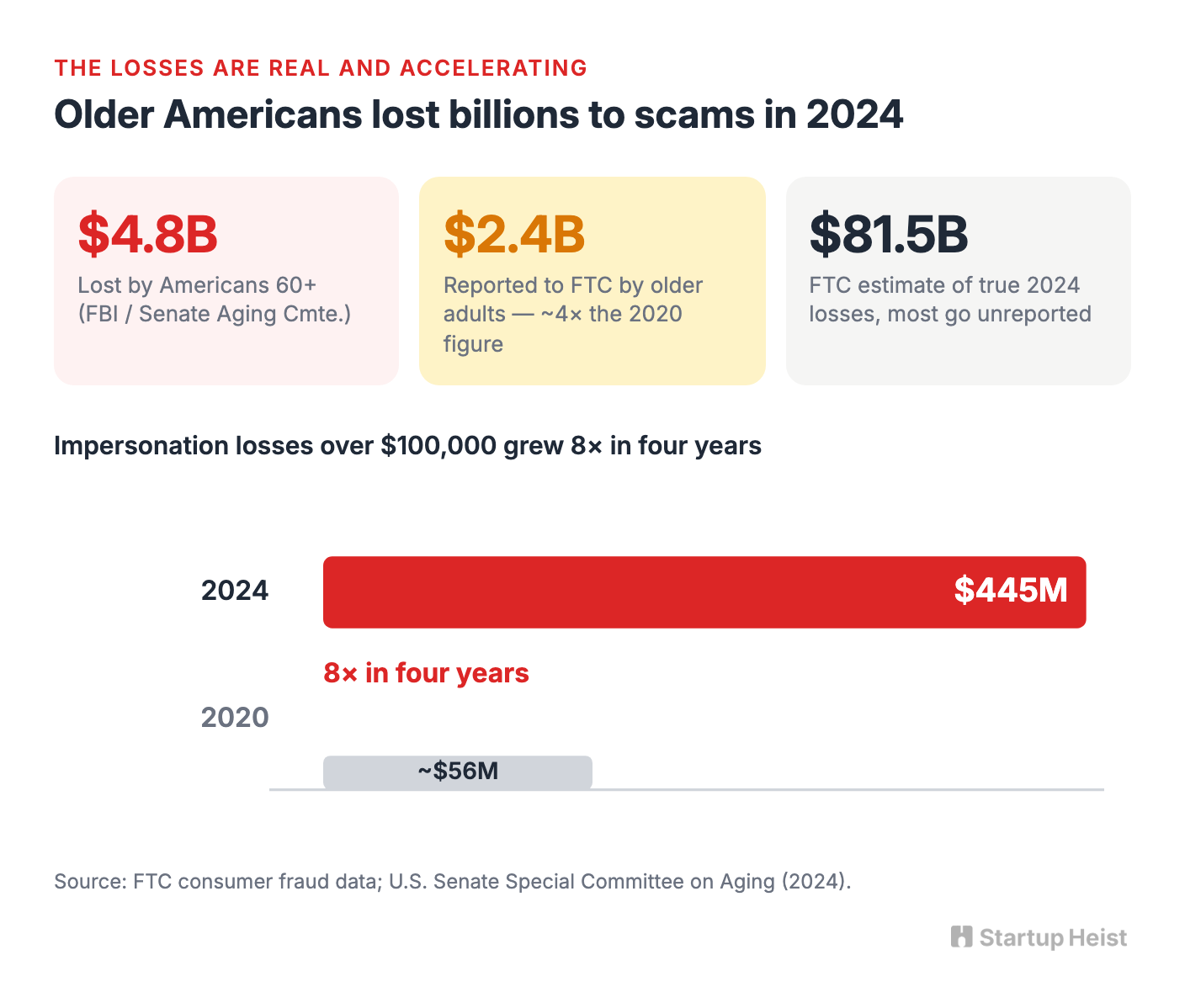

Older adults are the prime target because the payout is large and the savings are real. The U.S. Senate Special Committee on Aging reported that Americans over 60 lost $4.8 billion to scams in 2024, based on FBI data, while adults aged 50 to 59 lost another $2.5 billion. The committee flagged AI, cryptocurrency, and social media as the accelerants making these schemes harder to spot.

The Federal Trade Commission tells a sharper version of the same story. Older adults reported roughly $2.4 billion in fraud losses to the FTC in 2024, about four times the 2020 figure. The catastrophic end of the curve grew fastest. Reported losses over $100,000 from impersonation scams hit $445 million in 2024, eight times what they were in 2020. And because most fraud never gets reported, the FTC estimates the real number for older adults in 2024 could run as high as $81.5 billion.

There is a company hiding inside those numbers, and it is not the one most builders reach for. The weak version is an app that promises to detect deepfake voices. The strong version is a caregiver-bought scam firewall for aging parents: a lightweight elder fraud protection layer that screens suspicious calls, turns government safety advice into product workflows, checks sketchy websites and payment requests, and pulls in a trusted family member the moment a situation turns dangerous.

Here's the opportunity:

The money: 10,000 households at $15/mo is $1.8M ARR; 50,000 reaches $9M. Sold as peace of mind to the worried adult child, not the parent.

Inside:

• MVP scope around the bank-impersonation call

• Three-tier pricing up to a managed-phone plan

• Trust-channel GTM with outreach scripts

• The family-graph moat competitors can't copy

The product does not need to catch every scam. It needs to interrupt enough high-risk moments before irreversible money moves. The gap between detection and interruption is the whole opportunity.

The real product is an intervention system

"Scam firewall" sounds like antivirus: install it, let it run quietly, trust the machine to block the bad stuff. That framing is comfortable, and it is wrong.

Scams are not malware. The dangerous ones are persuasion attacks. They play out across phone calls, websites, payment apps, crypto ATMs, bank lobbies, gift-card racks, and relationships built over weeks. A scammer might spend months earning trust before asking for a dime. No single app can inspect every channel, verify every caller, and stop every transaction.

Voice-clone detection is the most fragile place to plant a flag. A scammer impersonating a bank, a government office, a romantic partner, or a grandchild often uses a perfectly real human voice. Even when the audio is synthetic, the useful question is rarely whether AI generated it. The useful question is behavioral: is someone demanding secrecy, account access, gift cards, crypto, or a transfer "to protect your money"?

The government already publishes the right answers. The FTC tells consumers not to trust caller ID, never to use contact details from an unexpected message, and to hang up and call an organization back on a number they know is real. It warns that no legitimate agency demands payment in gift cards, cryptocurrency, payment apps, or wire transfers. The National Council on Aging issues parallel warnings about voice cloning, deepfake impersonation, and personalized phishing.

The opportunity is to turn that advice into a product that shows up at the exact moment it matters. Picture a parent on a suspicious call. A plain yellow card appears on her screen:

This caller is not in your contacts. Banks never ask you to move money to keep it safe. Hang up and call the number on your bank card. Send this call to Linda?

She taps one button. Her daughter gets an alert with the caller's number, the risk signals, and a one-line read: Possible bank-impersonation scam. Unknown caller. Urgency language. Caller discussed moving funds. Call Mom now.

Or she gets a text about an overdue toll, a frozen account, a new online friend, a marketplace seller wanting a deposit. A single large button reads Check this before paying. She pastes a link, forwards the text, scans a QR code, or uploads a screenshot, and gets a plain-English verdict: High risk. This website was registered days ago. The payment request is unusual. Do not send money. Want to call your daughter?

This is not an AI bodyguard. It is a decision-friction machine. It buys time, breaks isolation, inserts a trusted human into the transaction, and makes the safe action easier than the risky one.

Why the market is better than it looks

On the surface, elder-fraud protection reads like a modest subscription niche. The likely price is $10 to $20 a month, and the buyer pool is narrower than the one for antivirus or family-safety apps.

What changes the math is emotional intensity. Fall-detection subscriptions protect against a rare event with catastrophic downside, and families buy them without blinking because the alternative is too frightening to gamble on. Scam protection lives in the same part of the brain. The buyer is not the parent. It is the adult child who lies awake wondering whether one convincing phone call could erase decades of savings.

That buyer already exists, and already shops this way. The elder-care market has fully normalized the "set this up for Mom" purchase. Medical-alert companies sell fall detection, GPS, and caregiver apps where the parent uses a simple device and the adult child pays the bill and runs the account.

The adjacent fraud products prove willingness to pay. True Link sells a prepaid Visa with caregiver-set spending rules, blocked merchant categories, and transaction alerts for $12 a month. EverSafe monitors accounts, credit, and suspicious activity and now markets phishing-email monitoring. Carefull watches accounts for elder-specific risk and, in March 2026, landed a partnership with banking-technology provider CSI to push elder-fraud protection through financial institutions. teleCalm goes deeper for dementia families, letting caregivers manage phone settings remotely, starting around $55.99 a month. Newer entrants like ZoraSafe and SeniorShield.ai are moving upstream into AI call screening, QR scanning, and family alerts.

The category is not empty, and that is the good news. Families already understand the problem. The open question is whether anyone can package call screening, simple transaction checks, and family escalation into one product that feels easier than stitching together five separate tools.

The white space is between the call and the payment

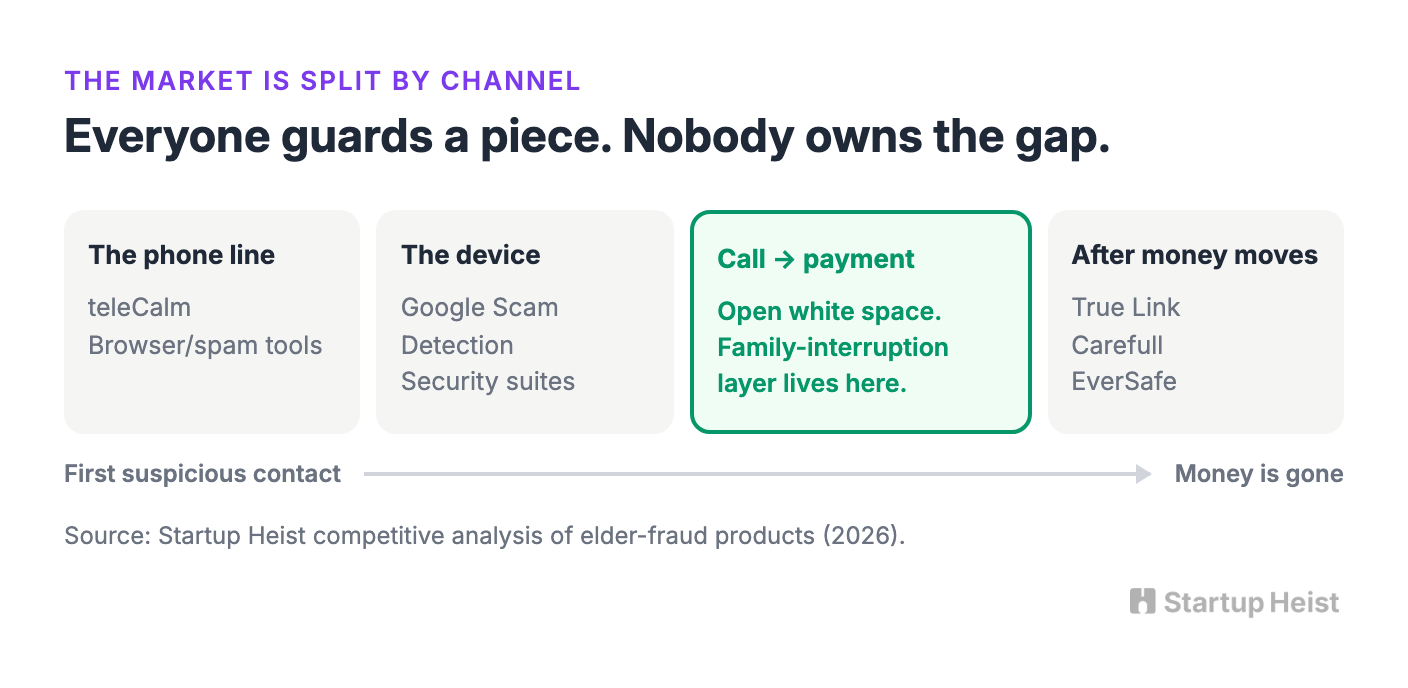

The existing market is split by channel. True Link, Carefull, and EverSafe act after money becomes visible. teleCalm owns the home phone. Browser tools flag bad websites. Security suites chase malware and identity theft. Nonprofits hand out brochures and hotline numbers.

Each piece is useful. None owns the critical gap between the first suspicious contact and the moment the victim sends money. That gap is where the company should live.

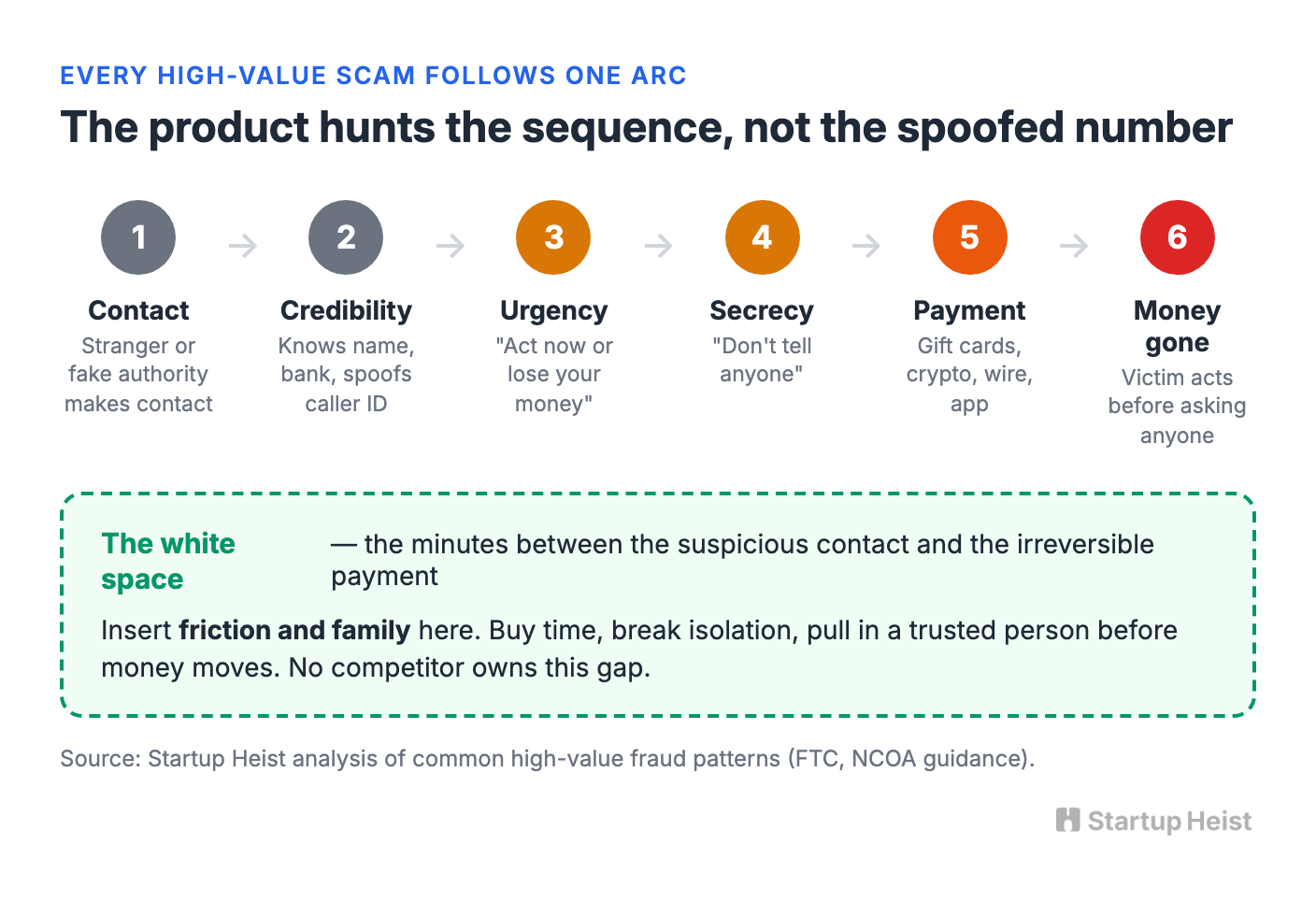

Almost every high-value scam follows the same arc. A stranger or fake authority makes contact. They build credibility. The conversation turns urgent. The victim is told to keep it secret. An unusual payment method appears. And the victim acts before consulting a single trusted person. The product should hunt for that sequence, not for a spoofed number or a robotic voice.

That points to a defensible thesis. Build a caregiver-controlled fraud-interruption layer that spots risky conversations, reinforces safe habits, and escalates to family before money moves. The call is the wedge because it is the most emotionally legible entry point. Transaction checks come later, because scams refuse to stay on the phone. The hard part is resisting the urge to market a universal shield on day one.

Google validates the need and rewrites the strategy

The strongest signal that call-level scam detection is real comes from Google. Its Phone app now runs Scam Detection on Pixel devices, using on-device AI to flag fraud-associated conversation patterns mid-call, with the audio staying on the device. It covers Pixel 6 and later in the US, runs on Gemini Nano on Pixel 9 and up, and is now available on the Samsung Galaxy S26 line. Google Messages applies the same on-device approach to suspicious texts from non-contacts.

This is validation and warning in one move. It confirms that real-time alerts during a suspicious conversation are useful. It also means no startup should build its entire identity around having invented AI scam detection. Google can ship that at the operating-system level, process audio privately, and put it on millions of phones for free.

So the opportunity sits one layer above the detector. Google protects the device. A caregiver product protects the family workflow. A caregiver needs answers the on-device classifier will never surface. Did Mom get three suspicious calls this week? Did one match a bank-impersonation pattern? Did she click a link afterward? Is there a safe word? Does she know which number to call back? Should her son get an alert? Is she heading to a crypto ATM or a gift-card aisle? Is this a one-off, or a pattern that points to repeat targeting or cognitive decline?

The moat is not a single classifier. It is the trusted network, the escalation logic, the intervention history, the distribution, and the accumulating understanding of how scams move through households.

Do not build the app that promises to hear every call

The naive plan writes itself: build an iPhone and Android app, listen to every cellular call, analyze the audio live, detect cloned voices, alert the caregiver. That plan is far harder than it sounds.

Apple's CallKit is built mainly to wire VoIP services into the system call interface, not to hand third-party apps raw cellular audio. Android's `CallScreeningService` is more generous, letting apps identify, screen, block, or divert calls, especially from numbers outside the contact list. But no native platform gives every app unrestricted access to live call audio.

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”