Retail real estate isn't collapsing. It's turning over.

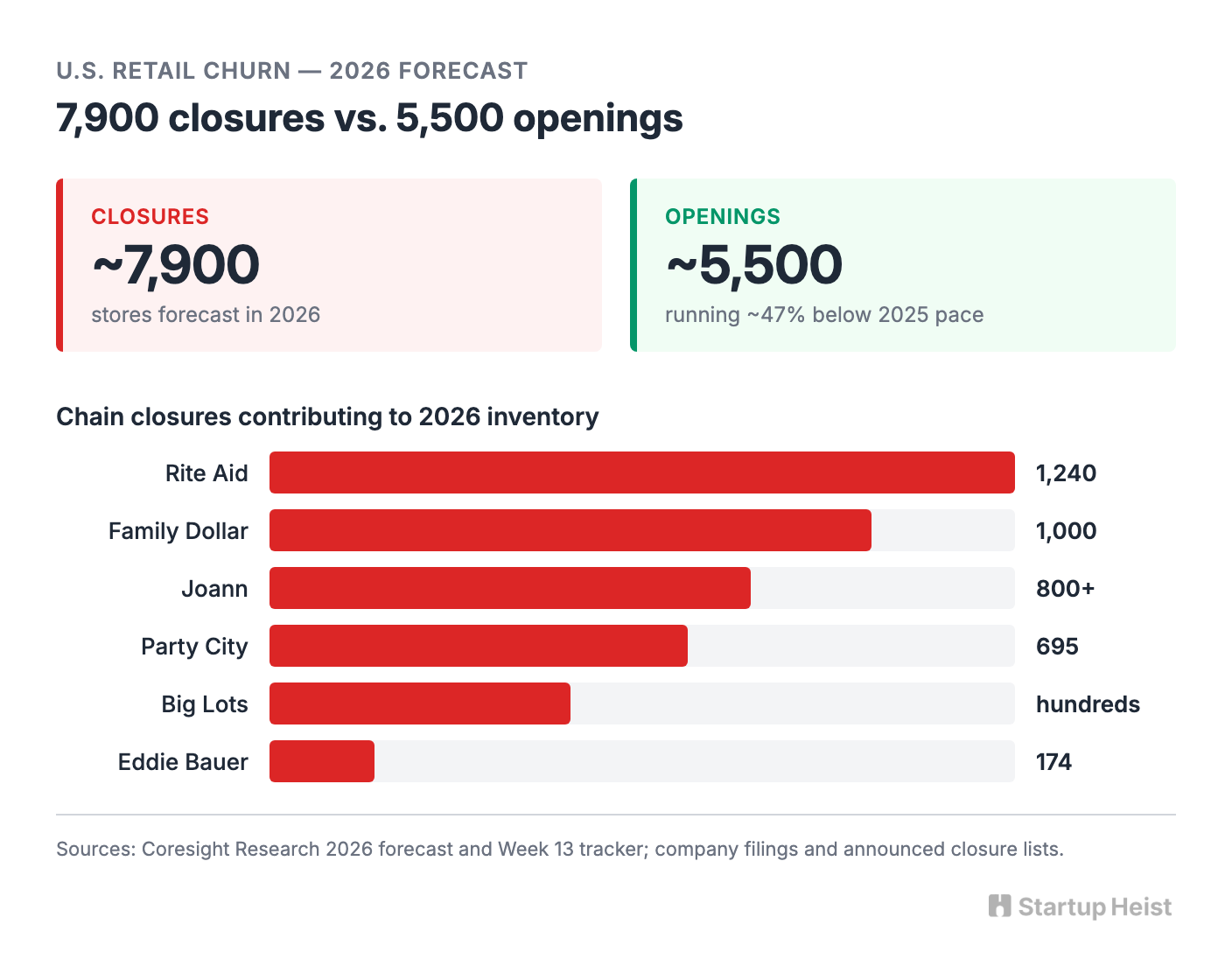

Coresight expects roughly 7,900 U.S. store closures in 2026 against about 5,500 openings. Failing formats are vacating space that expanding formats want, and the handoff between them is the most opaque transaction in commercial real estate. The headlines hear "closures" and write the obituary. The reality is messier and more interesting.

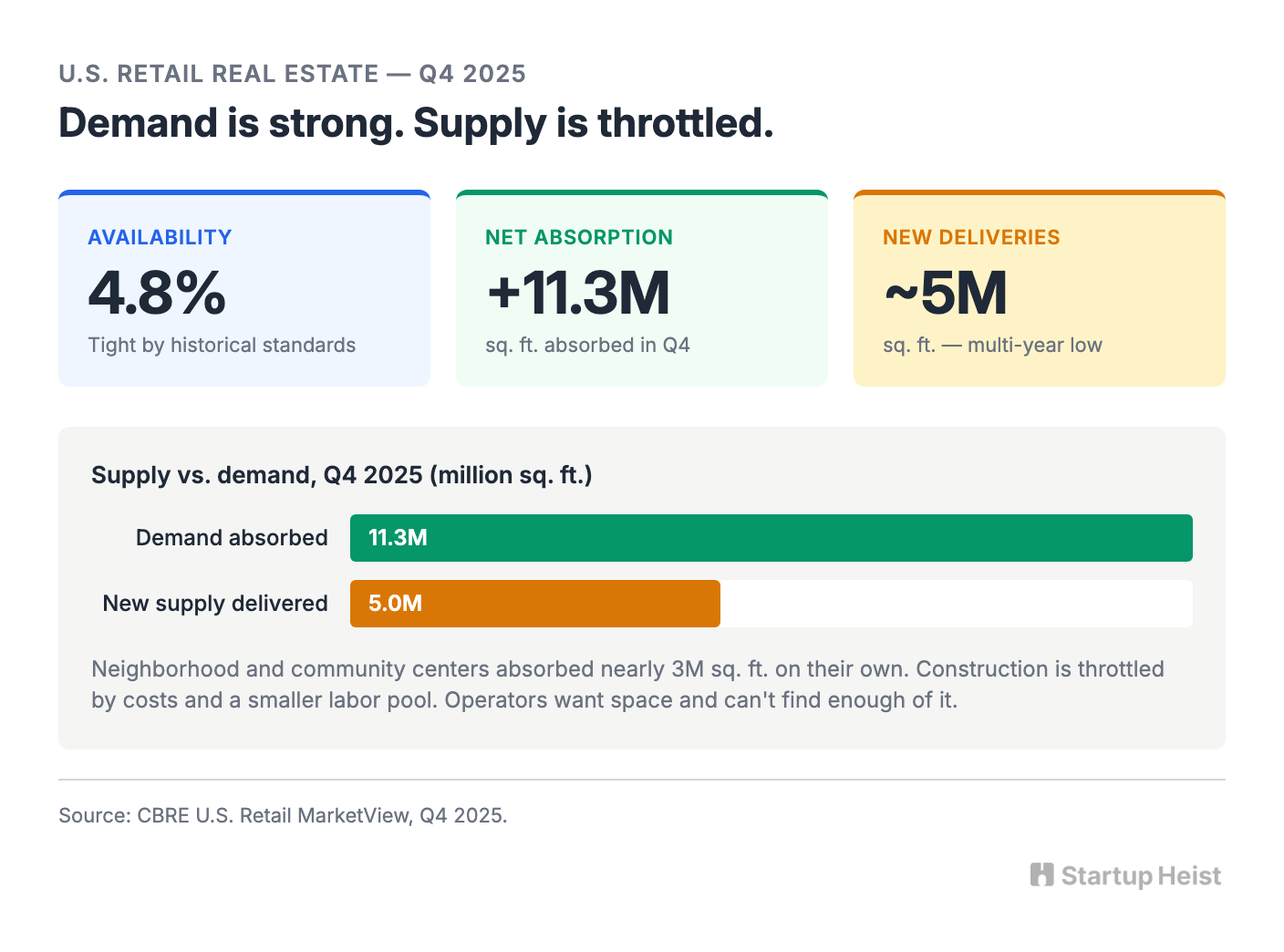

Look at what CBRE measured at the end of 2025. U.S. retail availability sat at 4.8% in Q4, with 11.3 million square feet of net absorption. Neighborhood and community centers absorbed nearly 3 million square feet on their own. New deliveries fell to roughly 5 million square feet, throttled by construction costs and a smaller construction labor force. A tight retail real estate market with strong demand and constrained supply.

Now layer the closure cycle on top.

Eddie Bauer is the cleanest signal of the moment. Its store operator filed for Chapter 11 on February 9, 2026, operated roughly 180 stores across the U.S. and Canada at the time of filing, and lined up an auction for March 6. The qualified-bid deadline came and went on March 3 with nothing submitted. The auction was canceled. All 174 remaining locations are liquidating, with physical closures slated by April 30. Authentic Brands Group still owns the trademark and is shifting e-commerce to a new licensing partner, so the brand survives. The boxes don't.

That's 174 second-generation retail spaces hitting the market in a span of weeks, in a market where good boxes are scarce. Eddie Bauer is just the loudest event of a wider cycle. Joann liquidated 800-plus stores after a second bankruptcy. Big Lots closed hundreds before a rescue deal collapsed for the rest. Party City, Express, Rite Aid, and Family Dollar are all contributing inventory across 2026.

Here's the opportunity sitting in plain sight.

The money: 30 Pro subscribers at $799/mo = $24K MRR. One $2,500/mo broker territory account replaces three Pro seats. Real budgets, no procurement cycle.

Inside:

• Five-module MVP for retail recapture

• Three-tier pricing from $299 to $5,000

• Sun Belt wedge with 5K-25K sq ft boxes

• Five-layer event graph as the moat

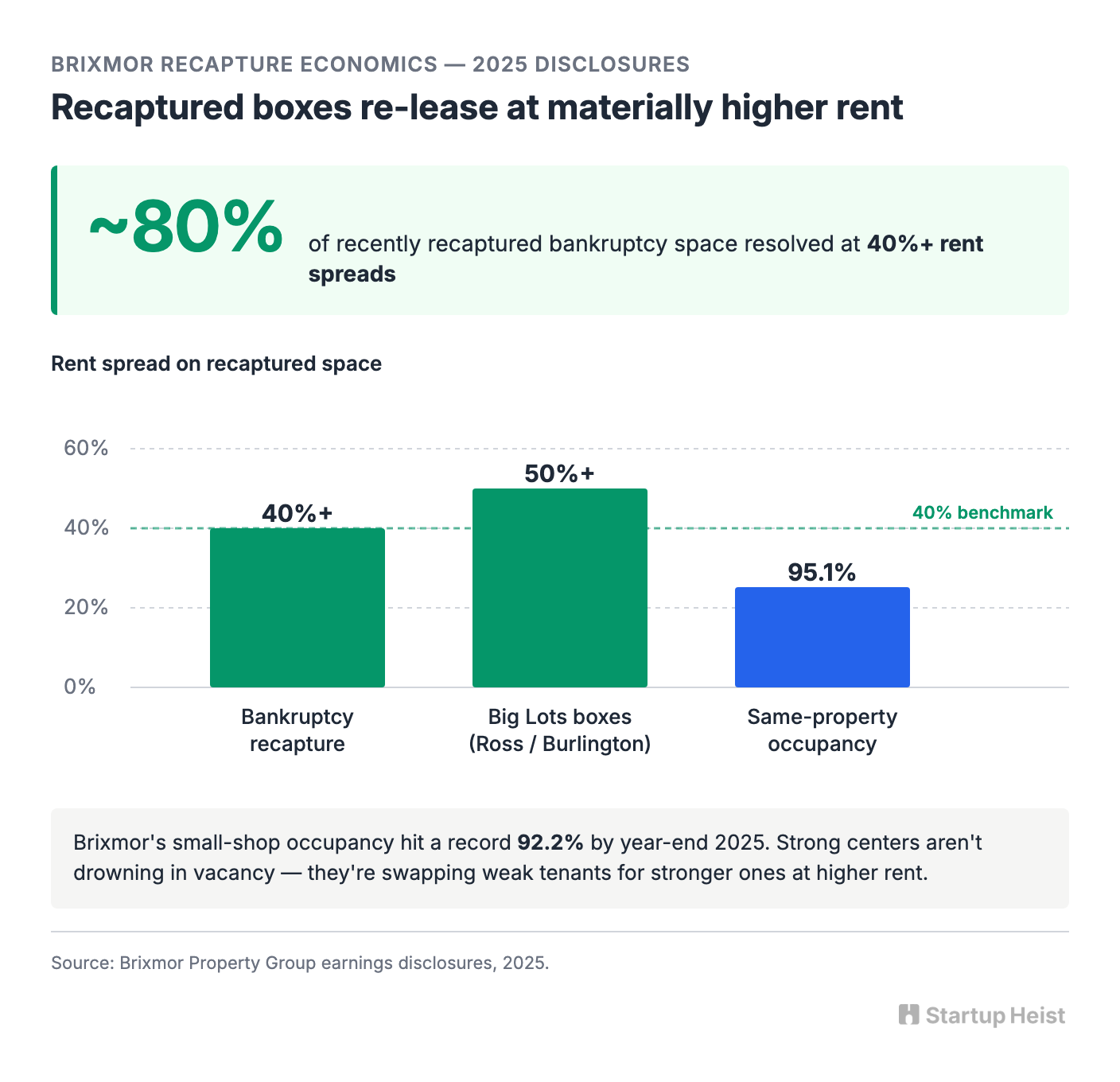

These aren't abandoned husks. Many sit in well-anchored centers landlords have spent five years upgrading. Brixmor disclosed across 2025 that roughly 80% of recently recaptured bankruptcy space was resolved at rent spreads exceeding 40%. Big Lots boxes in particular were being backfilled by Ross Dress for Less and Burlington at spreads above 50%. Brixmor's same-property occupancy hit 95.1% by year-end 2025, with small-shop occupancy at a record 92.2%.

Read that twice. Landlords aren't drowning. In strong centers, they're taking back weak tenants and replacing them with stronger ones at materially higher rent. The best recaptured boxes aren't distressed inventory. They're hidden inventory.

The question worth answering isn't "where is vacancy." It's: which good retail boxes are about to come back, and who will get to them first?

The mispriced pain

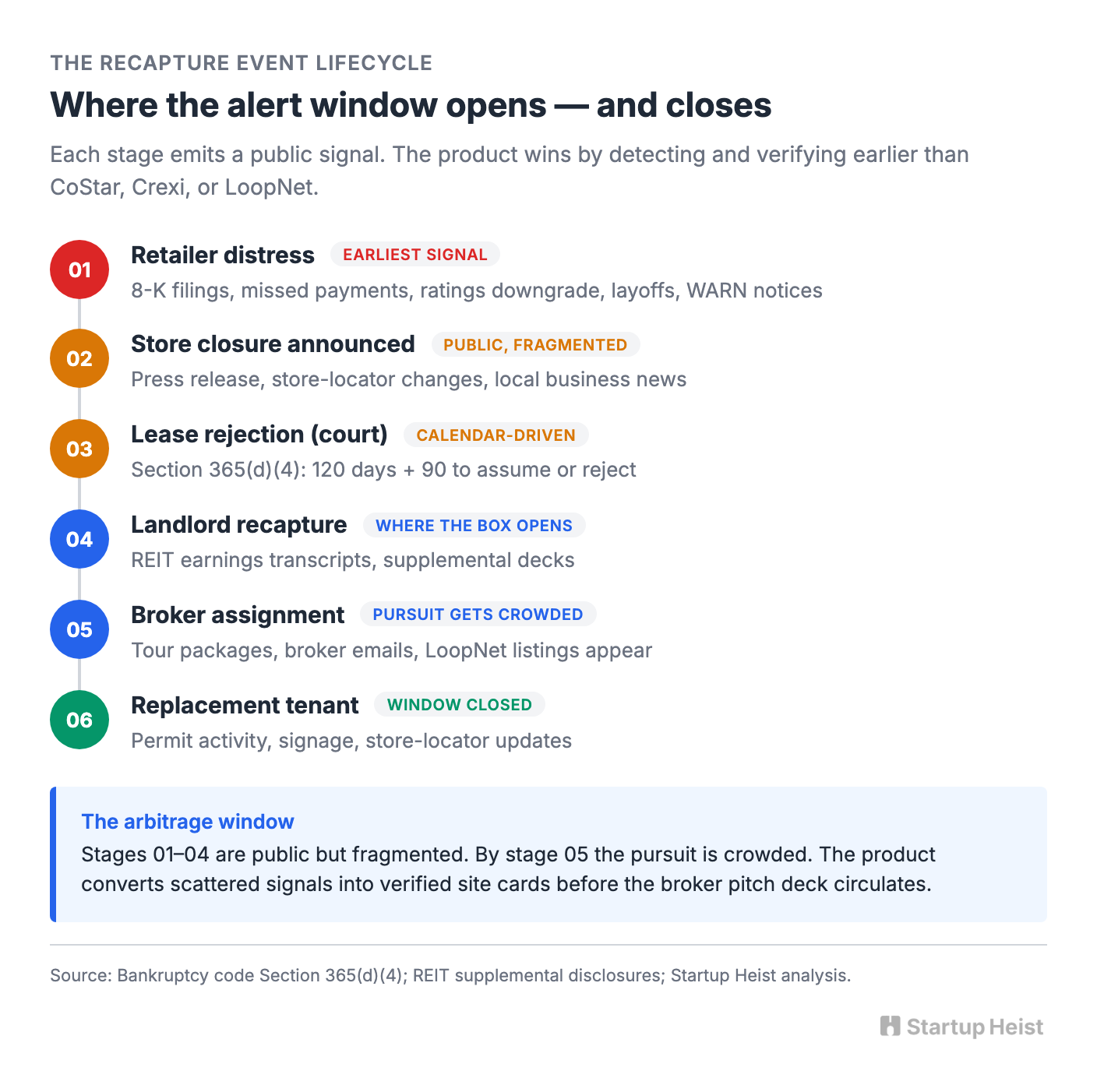

Expansion teams already have access to listings. CoStar covers the deepest national database. Crexi runs the marketplace for marketed inventory. Placer.ai measures foot traffic. LoopNet aggregates the broker-driven feed. None of them are optimized around the narrow moment a retail site moves from distressed tenant event to recaptured box to available deal.

That moment is where the money sits. By the time a listing is live, the pursuit is already crowded.

The information that predicts the listing exists. It just lives in ugly places. Bankruptcy dockets and lease rejection schedules. SEC filings and 8-Ks. Shopping center REIT earnings transcripts where executives mention recapture. Local business journals reporting a closure two weeks before the broker pitch deck circulates. State WARN notices. Liquidation sale start dates. County permit activity at the site. Old-fashioned phone calls between landlords and the brokers they trust.

The single most underappreciated public data point is the lease rejection deadline. Section 365(d)(4) of the bankruptcy code gives a debtor 120 days from petition to assume or reject a commercial lease, with one 90-day extension. After 210 days, undecided leases are rejected by operation of law. Each of those decisions is a recapture event. The court calendar tells you when they're coming.

That data is public. It isn't yet a product.

The buyer isn't Aldi first

The instinct is to build a Bloomberg terminal for distressed retail and pitch it to every expanding chain: Aldi, Sprouts, Five Below, Burlington, Crumbl, Raising Cane's, Orangetheory, F45.

Wrong wedge.

Aldi is opening more than 180 U.S. stores in 2026 across 31 states, on its way to about 2,800 locations and a target of 3,200 by 2028. Sprouts has 140-plus approved sites in its pipeline and plans 40 new stores this year. The hunger is real. So is the procurement cycle. Big chains run internal real estate teams, retain national broker partners, and pay enterprise vendors. They're slow, politically protected, and the wrong first customer.

The right first customer sits one tier below: tenant-rep brokers covering multi-market clients, franchise development directors trying to place operators in defined territories, multi-unit operators expanding from 5 to 50 locations, private-equity rollups in fitness, urgent care, med spa, dental, pet care, and discount retail. These buyers live close enough to the deal to value the information. One good site pays back a year of subscription. They can decide on a $799 invoice without a procurement cycle.

The cleanest profile: a tenant rep or expansion lead responsible for finding 10–100 retail sites a year across defined markets, in categories that thrive in 5,000–25,000 square foot second-generation retail boxes.

Build a pre-market recapture alert system for the people who source sites for a living.

Why now

Three forces line up.

Failing retailers are producing closure events at scale. Eddie Bauer alone puts 174 stores into the pipeline. Joann put 800-plus. Big Lots, Express, Party City, Rite Aid, and Family Dollar are all contributing across 2026. And Coresight's Week 13 tracker shows 2026 store openings running roughly 47% below the prior-year pace through mid-April, a real-time signal that operators are pickier and the deal pipeline is tightening further.

Expanding operators want physical space and can't get enough. Aldi needs 180 sites this year. Sprouts needs 40-plus. Off-price, fitness, medical retail, urgent care, discount grocery, QSR, and experiential concepts all want sites. CBRE's 4.8% availability rate proves they can't find enough.

New construction is throttled. Limited deliveries. High costs. No fast fix on the supply side.

The result is a market with closures and a shortage of good vacancy. Data sources for site selection exist, but no clean workflow connects them. That gap is exactly where a focused software product can land.

The MVP looks simple on the surface. The customer picks markets, box sizes, tenant types, co-tenancy preferences, and target formats. The system watches the closure and recapture signals. Each verified signal becomes a site card. The customer gets alerts, a map, and a workflow.

The core object is a recapture event. Each event carries the closing tenant and parent, address and shopping center, estimated square footage, closure trigger (bankruptcy, lease rejection, recapture, liquidation, permit, news), stage (rumored, court-filed, liquidation, vacated, marketed, leased), landlord and broker, adjacent anchors, source documents, confidence score, and recommended buyer fit.

A useful card looks like this:

Site: Former Eddie Bauer, lifestyle center, suburban Philadelphia

Size: 7,000–10,000 sq. ft.

Trigger: Bankruptcy wind-down, auction canceled

Status: Closing sale active

Expected availability: 30–90 days

Best-fit users: Boutique fitness, off-price soft goods, medical retail, specialty grocery, education

Why it matters: Second-gen box in an established trade area; strong-anchored center likely to want a stronger replacement tenancy

Sources: Court filing, retailer closure list, local report

Confidence: Medium-high

Next step: Call landlord; verify broker assignment

From the card, the user can watch, dismiss, assign to a broker, request verification, export to CRM, add notes, or generate landlord outreach. The workflow is the moat, not the map.

The five modules

Build the first product in five parts.

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”