Your Insurance Company Is Photographing Your Roof. Sell Homeowners the Counter-Surveillance.

A homeowner opens a letter from their insurance company and learns the carrier won't renew the policy.

There was no storm claim, no inspector on the roof, no knock on the door. The notice mentions roof condition, or overhanging vegetation, or debris. Somewhere upstream, an aerial image captured by satellite, aircraft, or drone passed through an underwriting system. The system saw a risk, and the homeowner got a cancellation deadline.

This is now routine. NPR reported in May 2025 on homeowners across the country losing coverage or receiving repair demands after insurers flagged roof wear, debris, or vegetation visible only from above. One widely covered California case involved a homeowner whose policy was pulled after she drained her swimming pool during a drought and the drone photo read it as deferred maintenance. The state's Department of Insurance has fielded a stream of complaints like it.

The image may be accurate. It may also be old, blurry, aimed at the wrong structure, or showing harmless discoloration rather than material damage. The homeowner usually doesn't know which. They're left to call an agent, find a roofer, gather photographs, interpret a vague letter, and hope somebody at the carrier reconsiders.

That gap is the opportunity: a micro-SaaS that helps homeowners and their agents see the property the way an insurer's aerial-imagery workflow sees it, identify the most likely underwriting problems, and assemble a state-specific remediation or dispute packet in minutes.

The money: 150 agencies at $300/month is $45K MRR, plus reviewed-packet fees on top. No direct competitor serves this niche yet.

Inside:

• Four-state rules engine MVP, no custom CV

• Agent pricing tiers from $149 to $699/month

• Three moats: rules graph, outcomes, network

• Expansion into adverse-action defense

This isn't an anti-insurance protest tool, and it shouldn't promise to reverse every nonrenewal. Sometimes the roof genuinely needs work. Sometimes the carrier is exiting a region and no appeal will fix that. The product is a triage layer: it tells the homeowner whether the fastest path is to challenge the evidence, document a repair, get a professional inspection, trim the trees, replace the roof, or stop fighting and shop for another carrier immediately. A modest promise, and a useful business.

The insurer has an information advantage

The insurance industry has spent years building a remote property-intelligence stack. Nearmap sells AI-derived roof condition assessments that flag staining, ponding, repairs, rusting, and missing tiles; its Roof Age product, updated in October 2025, estimates the year a roof was installed by blending aerial imagery, deep-learning models, building permits, assessor records, and climate data, with results returned in under two seconds. Eagleview sells remote residential property reports with roof measurements, pitch distribution, and oblique imagery starting at $32.75 per address. Zurich announced in 2025 that it is wiring these insights directly into underwriting.

None of this is sinister; the tools are genuinely useful. What's broken is the asymmetry. The professional side can evaluate thousands of homes remotely in seconds, while the homeowner receives the consequence without an intelligible explanation of the inputs, the confidence level, or the fastest route to remediation.

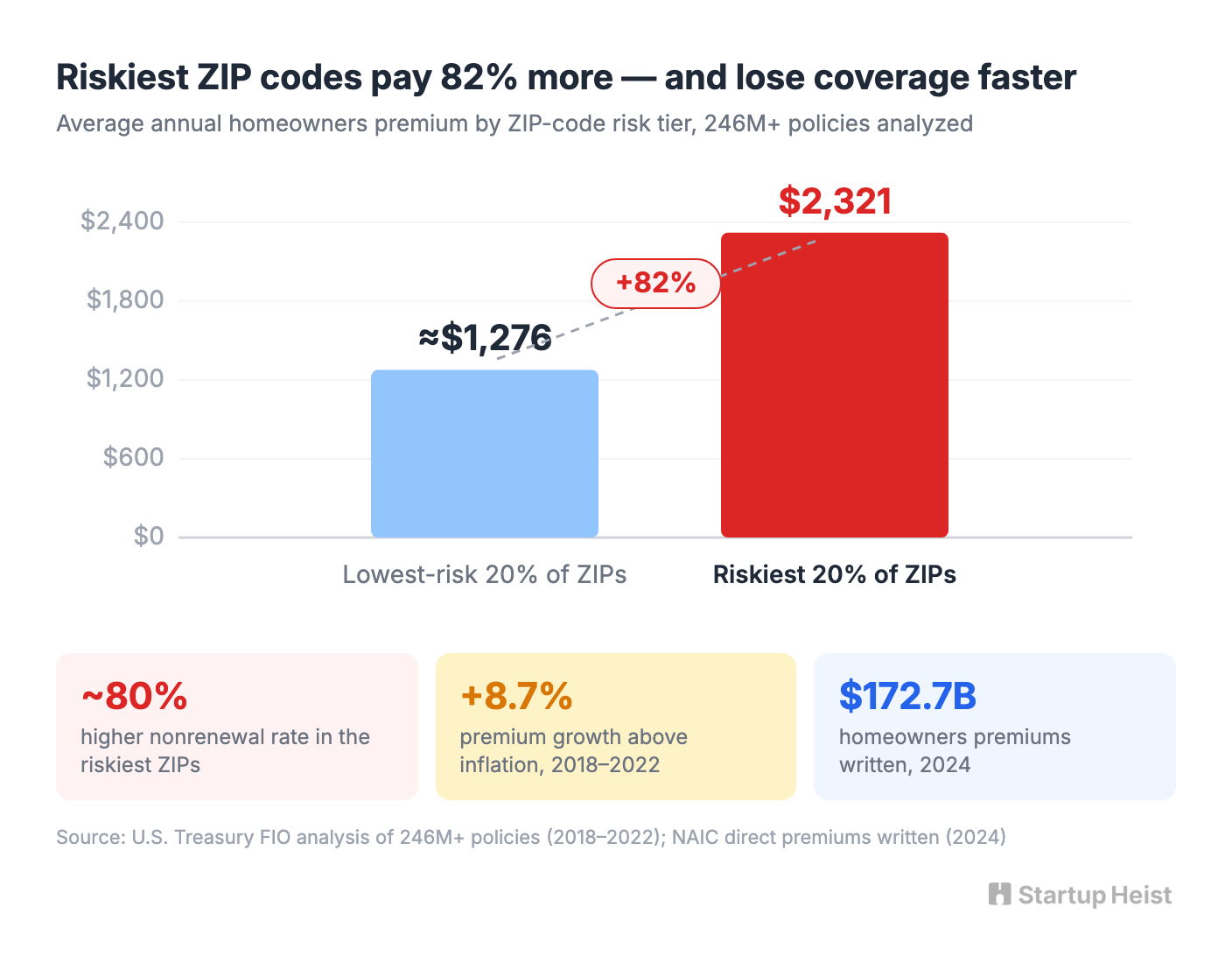

The stakes are large. The National Association of Insurance Commissioners reported $172.73 billion in 2024 direct premiums written for homeowners multiple-peril coverage. A U.S. Treasury analysis covering more than 246 million policies from 2018 to 2022 found average premiums rose 8.7% faster than inflation, and homeowners in the riskiest 20% of ZIP codes paid $2,321 per policy, 82% more than the lowest-risk ZIPs, while facing nonrenewal rates roughly 80% higher. Carriers have every incentive to inspect portfolios more aggressively, and aerial imagery is the cheapest way to do it. Nobody is building the homeowner's side of that equation. Consumer advocacy groups publish general guidance, but no software product exists for disputing an aerial-imagery nonrenewal.

The regulation is becoming productizable

A startup gets more interesting when the customer's pain comes with procedure attached. State regulators have begun issuing guidance on how insurers may use aerial imagery in cancellations, nonrenewals, and claim denials. The standards vary by state, and that variation is the foundation of the product.

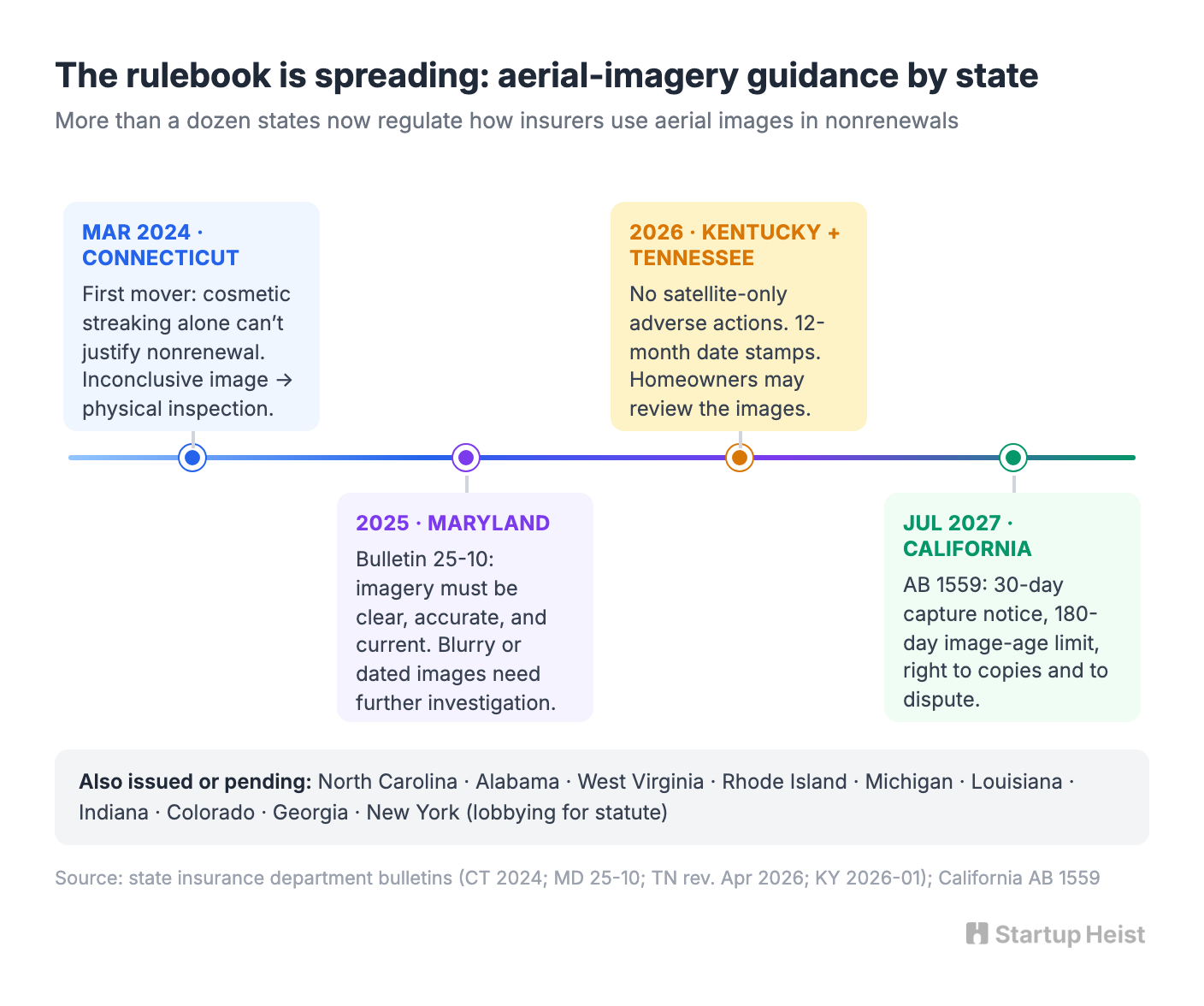

Connecticut moved first, in March 2024: natural discoloration and streaking are cosmetic and don't justify nonrenewal by themselves; insurers need evidence of material degradation, and when an image is inconclusive, a physical inspection or roofer's report should serve as the guardrail. Maryland's Bulletin 25-10 says imagery can justify an adverse action only when it is clear, accurate, and current; blurry or dated images require further investigation. Tennessee's bulletin, updated April 2026, warns that imagery can be vague, outdated, or aimed at the wrong structure, and says homeowners should be allowed to dispute it and given reasonable time for repairs. Kentucky's Bulletin 2026-01 reads like an operational checklist: satellite imagery alone can't support a cancellation, nonrenewal, or claim denial; drone or aircraft imagery must be clear, paired with a written summary of the specific conditions, and date-stamped within the previous 12 months; the insured is entitled to review the images relied upon.

The wave is still building. North Carolina, Alabama, and West Virginia have issued bulletins of their own; Rhode Island, Michigan, Louisiana, Indiana, Colorado, and Georgia have followed with guidance or pending rules; New York producers are lobbying for statutory standards. More than a dozen states are now active. California goes furthest: AB 1559, effective July 1, 2027, requires 30 days' notice before insurers capture aerial images, bans termination based on images older than 180 days, and gives homeowners the right to copies, to dispute accuracy, and to request an in-person inspection to verify remediation.

The rules are fragmented across bulletins, statutes, notices, and complaint procedures. Most homeowners will never read them. Most agents don't have time to turn each new regulator notice into a repeatable workflow. A focused software product can.

The product: an adverse-action copilot for the home

Call it RoofProof for now. The customer enters an address and uploads the carrier's notice. RoofProof retrieves current third-party imagery where available, asks a short series of questions, and generates a structured response.

The interface shouldn't claim to reproduce the carrier's proprietary algorithm. That would be difficult to prove and unnecessary. The honest promise is narrower: see the visible conditions an aerial-imagery underwriting workflow is likely to flag, compare the carrier's explanation against your state's standards, and generate the evidence package needed to respond quickly.

RoofProof has two core modes.

Mode 1: the pre-renewal risk scan. A homeowner, agent, or roofer enters an address 60 to 120 days before renewal. The report highlights visible issues that may attract underwriting scrutiny: overhanging branches, roof staining or streaking, possible ponding, patching or tarping, debris, missing shingles, structures obscured by trees, pools and trampolines, plus the age and confidence level of the imagery itself. The output is a prioritized maintenance list rather than a pass-or-fail insurability score: Fix now. Document now. Inspect in person. Probably cosmetic. Unable to determine from aerial imagery. That last label matters because Connecticut's regulator explicitly treats inconclusive imagery as grounds for a physical inspection, not an adverse action. The product's honesty mirrors the rulebook.

Mode 2: the nonrenewal response packet. The urgent product starts with the carrier's notice. The homeowner uploads the letter, selects the insurer, and answers a guided questionnaire: What reason did the insurer give? Did the carrier provide the image? Is the image date visible? Has the roof been repaired recently? How many days remain? Is this property-specific, or is the carrier withdrawing from the region? The rules engine then produces the packet:

- A plain-English summary of the carrier's allegation

- A state-specific evidence checklist

- A request for the images and supporting materials, where appropriate

- A remediation letter documenting repairs or scheduled work

- An appeal or reconsideration letter

- An organized appendix with images, receipts, inspection reports, and contractor notes

- A regulator-complaint cover sheet when escalation is appropriate

- A separate checklist for shopping replacement coverage if the appeal fails

The product generates documents, not legal conclusions. It can say: "Kentucky guidance indicates that aerial imagery used as the basis for a nonrenewal should be clear, paired with a written summary, and date-stamped within the previous 12 months. Your uploaded notice does not appear to include the image date. Consider requesting the image and asking the carrier to confirm the date." It shouldn't say: "Your insurer violated the law." That distinction protects both the customer and the company.

Don't sell primarily to panicked homeowners

The highest-intent search query is a distressed homeowner typing "insurance nonrenewal roof aerial photo what do I do." That makes direct-to-consumer SEO valuable. It doesn't make DTC the best primary business model. A pure consumer funnel has weaknesses: demand is episodic, support is emotionally intensive, the customer may blame the software when an appeal fails, and each homeowner is usually a one-time buyer who needs a roofer or agent anyway.

The better wedge is the independent insurance agent. The Big "I" Agency Universe Study counts approximately 39,000 independent property-and-casualty agencies in the United States, 76% of them small or medium-sized. When a customer receives a roof-related notice, the agent is already the first phone call. The agent needs to preserve trust, explain what happened, collect evidence, decide whether to push back, and find alternative coverage if necessary. RoofProof turns that messy service problem into a repeatable client-retention workflow.

Roofers are the second channel. IBISWorld counts roughly 109,000 U.S. roofing businesses generating $92.5 billion in 2026 revenue, and a co-branded scan is a sharper lead-generation tool than a generic free inspection. But roofers shouldn't be the first wedge. An agent can credibly say, "Let's figure out whether you need a repair, an inspection, an appeal, or a new policy." A roofer risks sounding like every problem requires a new roof. The agent owns the trusted triage moment. The roofer is the fulfillment partner.

The MVP: build the rules engine before the computer vision

The obvious temptation is to build a sophisticated roof-scoring model. Resist it. Nearmap, Eagleview, and other property-intelligence providers have already invested heavily in imagery and AI-derived detections. Use those capabilities rather than attempting to outperform them from day one. The scarce value sits in the translation layer between imagery, homeowner evidence, state-specific procedure, and a clean next action.

A credible v1 launches with these four states:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”