The Kiosk-in-a-Box for America's Cash Economy

The obvious play is to launch another remittance startup. The sharper play is to sell the operating system to the people already standing next to the cash.

Roughly 19 million U.S. households still rely on nonbank services to handle daily money: check cashing, money orders, prepaid reloads, payday loans, pawn shops. Most of them have a bank account somewhere. Another 5.6 million have no account at all. Those are the FDIC's 2023 numbers, released November 12, 2024, and they've barely budged since the pandemic. Most of these workers own a smartphone and use WhatsApp every day. They navigate gig apps. Their financial life still moves through laundromats, bodegas, ethnic groceries, wire-transfer counters, and prepaid card racks.

Modern phones, archaic money. That's the gap. The opportunity isn't another neobank, or crypto for immigrants, or a beautiful app that assumes the user already has a bank account, debit card, stable address, fluent English, and trust in fintech branding. The opportunity is a cash-to-digital onramp kiosk: a low-cost Android tablet locked into a single app, installed inside laundromats, bodegas, small grocery stores, and migrant-heavy community businesses. It walks cash-heavy workers through phone top-ups, prepaid card loading, remittance initiation, wallet deposits, and eventually a broader bundle of bilingual financial services, with help from the person at the counter.

The real heist isn't owning the kiosks yourself. It's selling the software, setup kit, compliance workflow, merchant playbook, and operating dashboard to local operators who already have the customer relationship. Don't try to become Western Union with worse distribution. Become the Shopify-for-cash-onramps layer for immigrant-serving storefronts.

Here's the brief on the opportunity itself.

The money: 20 active locations at $99–$299/month plus transaction share lands a solo founder in the $3–8K MRR range before scale, with clear lift from a recurring software fee.

Inside:

• MVP scope: 4 buttons, 5 merchants, 60 days

• Three-tier pricing with transaction share

• Merchant outreach script and pilot offer

• Four moats built on local distribution

A market hiding behind unfashionable storefronts

The financial press keeps writing the underbanked off as if they were vanishing. The numbers say otherwise.

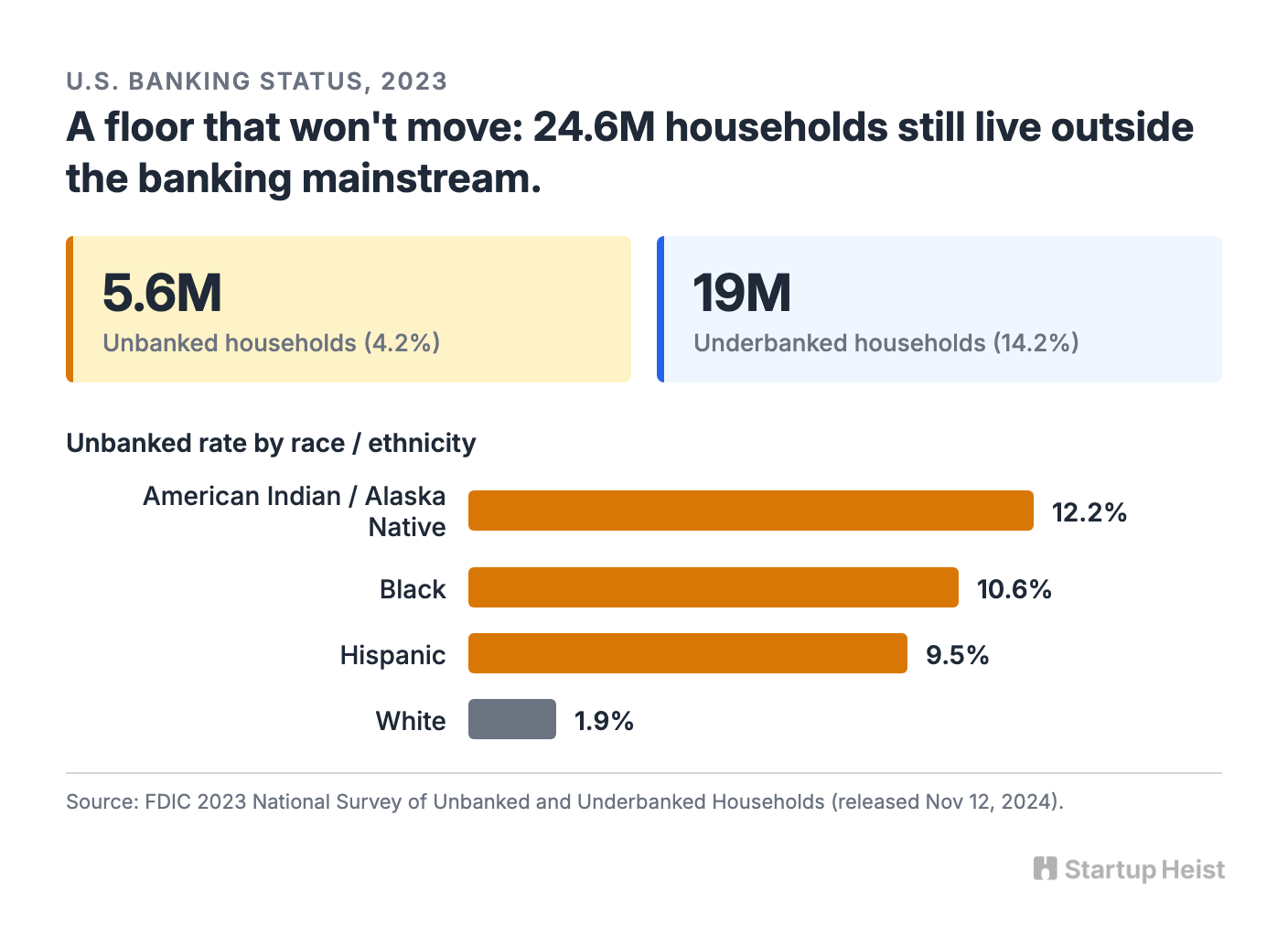

In 2023, 4.2 percent of U.S. households (about 5.6 million) were fully unbanked, and 14.2 percent (about 19 million) were underbanked. The unbanked rate fell almost in half since 2011, but the floor stayed put. Black households remained 10.6 percent unbanked, Hispanic 9.5 percent, American Indian and Alaska Native 12.2 percent, all far above the 1.9 percent rate for white households. These customers aren't financially illiterate. They're practical. They use what works near home, near work, in their language, during the hours they can actually show up.

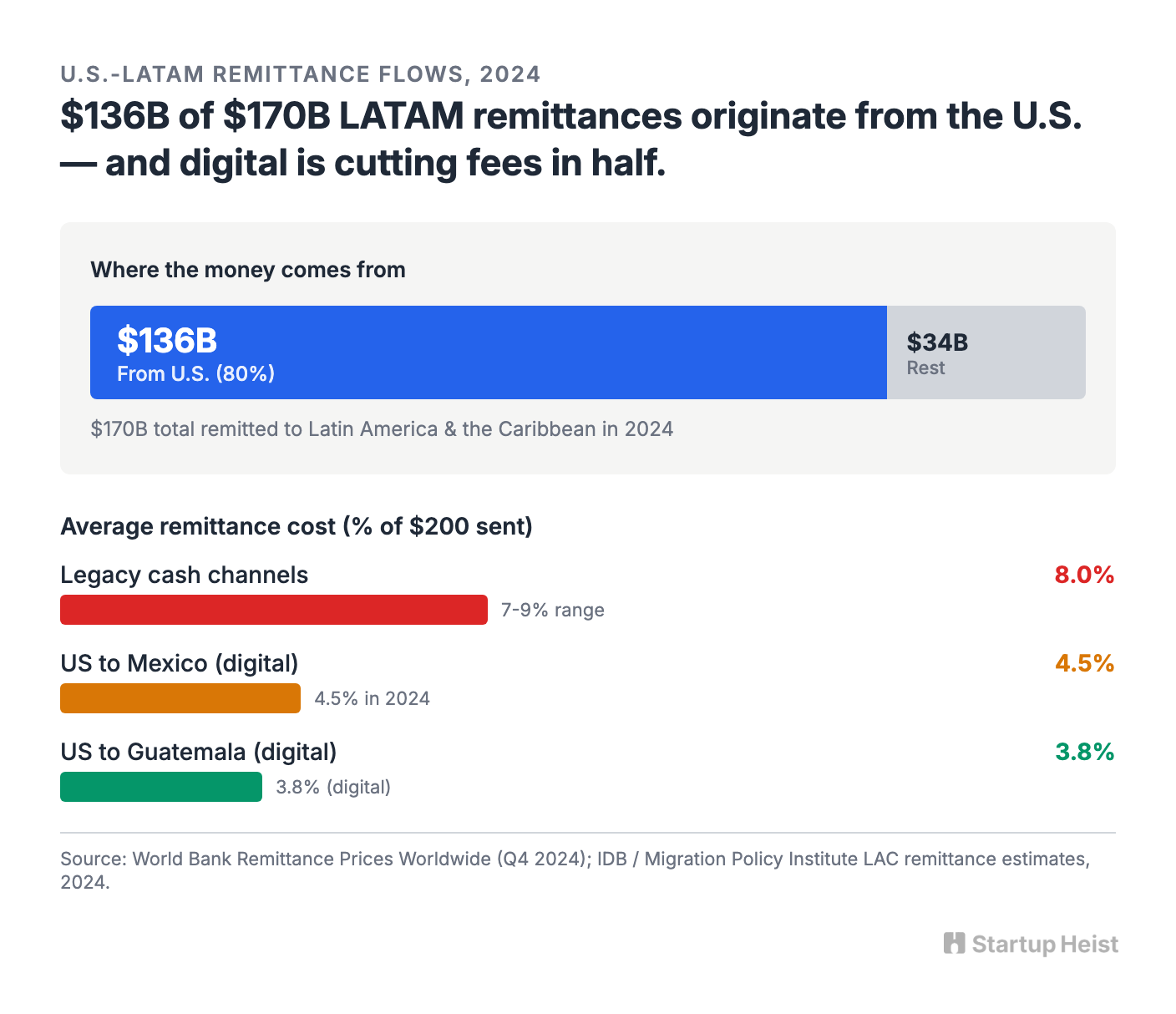

The digital remittance market sits in a parallel timeline. Grand View Research projects the U.S. digital remittance market hitting $12.7 billion by 2030, growing at a 14.9 percent compound annual rate from 2025. The U.S. already accounted for 23.2 percent of the global market in 2024, and roughly $136 billion of the $170 billion remitted to Latin America and the Caribbean that year originated here. World Bank corridor data shows digital channels running roughly 3 to 4 percent for major US-Latin America routes (US-Mexico landed near 4.5 percent in 2024, US-Guatemala digital around 3.8 percent), down meaningfully from legacy cash costs of 7 to 9 percent. So digital remittance is scaling and cash dependency isn't retreating. Most fintechs chase the banked, app-ready customer. Most legacy money-transfer companies serve the cash customer but trap them inside legacy workflows. Nobody has packaged the transition layer in the middle.

The customer doesn't want financial inclusion. He wants Tuesday solved.

A construction worker in South Florida or an agricultural worker in California's Central Valley isn't waking up thinking about digital wallet strategy. He's thinking: my phone needs minutes, my family needs $200 by tomorrow, this check needs cashing without losing too much, this card needs to work online.

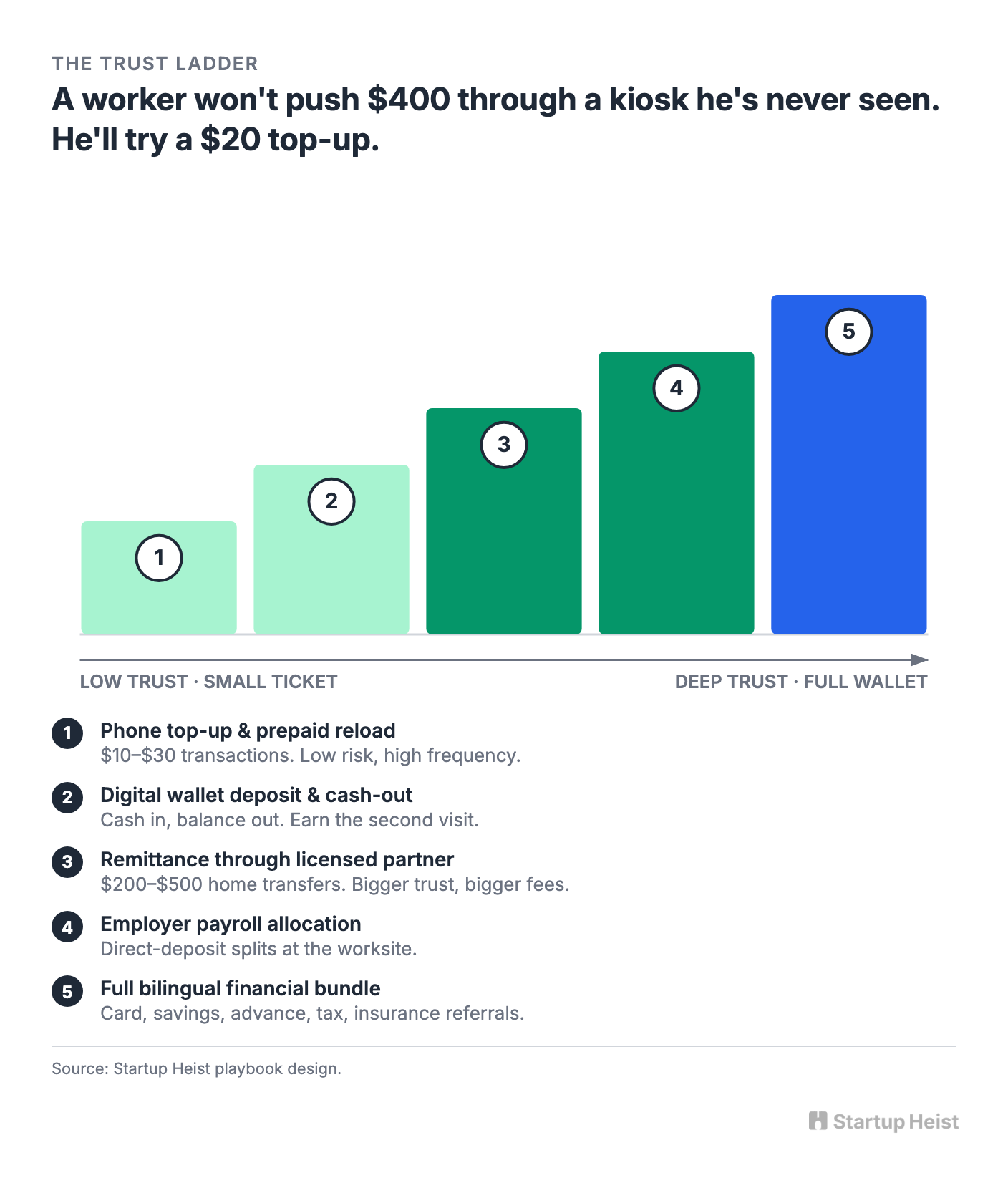

That's why the kiosk has a shot. It sells small, concrete jobs: put money on my phone, send money home, load a prepaid card, turn cash into usable digital balance, get a receipt, do it in Spanish, let me ask the cashier if I get stuck. That last part is underrated. The kiosk shouldn't be imagined as a fully autonomous ATM. The first winning version is a counter-assisted tablet, where the local store owner or trained cashier helps the user complete the flow. The tablet standardizes the process, reduces training burden, captures transaction data, and creates a repeatable software layer. This is an assisted-service kiosk, and that distinction quietly changes the entire business model.

Don't own the cash. Sell the kit.

The romantic version of this business is simple: buy tablets, install lockboxes, place kiosks everywhere, take transaction fees. That version turns ugly fast. The moment a startup owns the cash box, it owns theft risk, cash reconciliation, insurance, repair, hardware replacement, local servicing, fraud disputes, customer support, compliance exposure, and state-by-state money transmission headaches.

Handling cross-border money flows or stored value can trigger Money Services Business obligations. FinCEN requires MSBs to register within 180 days of establishment, with renewal every two years. An agent of a registered MSB doesn't have to register separately, provided the agent only acts as an agent, but the MSB itself must maintain an agent list, update it annually, and retain it for five years. That regulatory shape points to the better structure: don't become the regulated money transmitter on day one. Partner with one. Let the local merchant handle the physical relationship under a structured agent or partner model designed with counsel.

Your first paying customer isn't the migrant worker. It's the local merchant who already serves migrant workers: laundromats, bodegas, small groceries, ethnic markets, tax prep shops, prepaid phone retailers, independent check-cashing operators, money-transfer counters that want better digital workflows.

The pitch is direct. You already have the foot traffic. We give you a counter-grade service desk that turns it into recurring fee income, without making you build software, negotiate integrations, design bilingual flows, or figure out device setup yourself. The kit ships with a locked-down Android tablet, a recommended stand and cash-handling setup, bilingual customer flows, an operator dashboard, transaction reconciliation, an integration layer to money-movement partners, scripts and signage, a compliance checklist, training videos, a merchant revenue-share calculator, local marketing templates, and a support playbook. That stack turns the company from a cash-logistics business into a merchant-distributed fintech. Better founder-market shape, better business to scale.

Why this is suddenly buildable

This is a 2026 idea, not a 2018 idea. Four things changed.

Digital remittance crossed the threshold from fringe to default: billions in U.S. revenue, mid-teens annual growth. Underbanked Americans aren't shrinking, and 19 million is too large a market to dismiss as a niche, especially because cash-preferred and documentation-sensitive workers move in and out of nonbank services seasonally. Android kiosk infrastructure has become cheap and boring; vendors like Hexnode and Scalefusion lock devices into single or multi-app modes and centrally manage fleets at roughly $2 to $4 per device per month.

Then the rails arrived. On May 2, 2025, MoneyGram and the Stellar Development Foundation launched MoneyGram Ramps, a developer API that lets wallets and apps move users between physical cash and digital dollars (Circle's USDC) using MoneyGram's network across 180-plus countries, without requiring a bank account. Wallets like Decaf, Vibrant, and LOBSTR have already integrated, with more activity across the broader Stellar ecosystem. By September 2025, MoneyGram itself shipped a stablecoin-powered consumer app in Colombia. The plumbing isn't theoretical anymore. What doesn't exist is a packaged interface and operating model that lets thousands of small local merchants run on top of those rails. AllTrust Networks and Maya have built a real assisted-retail footprint (about 2,000 merchants in 46 states, $53 billion in checks processed historically, a 9 million-consumer biometric database), but their product centers on check cashing, not the broader bundle a cash-first customer brings to the counter.

The opportunity isn't to beat MoneyGram or AllTrust. It's to make MoneyGram-grade rails usable by thousands of smaller operators, with a service stack broader than what check-cashing networks already cover.

Start with phone top-ups, not remittance

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”