Most consumer healthcare startups die because they aim at the entire system. They try to fix care, fix insurance, fix every dashboard a sick person logs into. The American healthcare system does not bend to a cheerful onboarding flow.

There's a smaller, uglier, more lucrative wedge sitting in plain sight: the moment a patient opens an envelope and reads a hospital bill for $1,800, $7,400, or $23,000. They don't know if the number is accurate, negotiable, inflated, duplicated, mis-coded, eligible for charity care, or simply the price of being too tired to fight back. Every American household eventually lands in that exact moment.

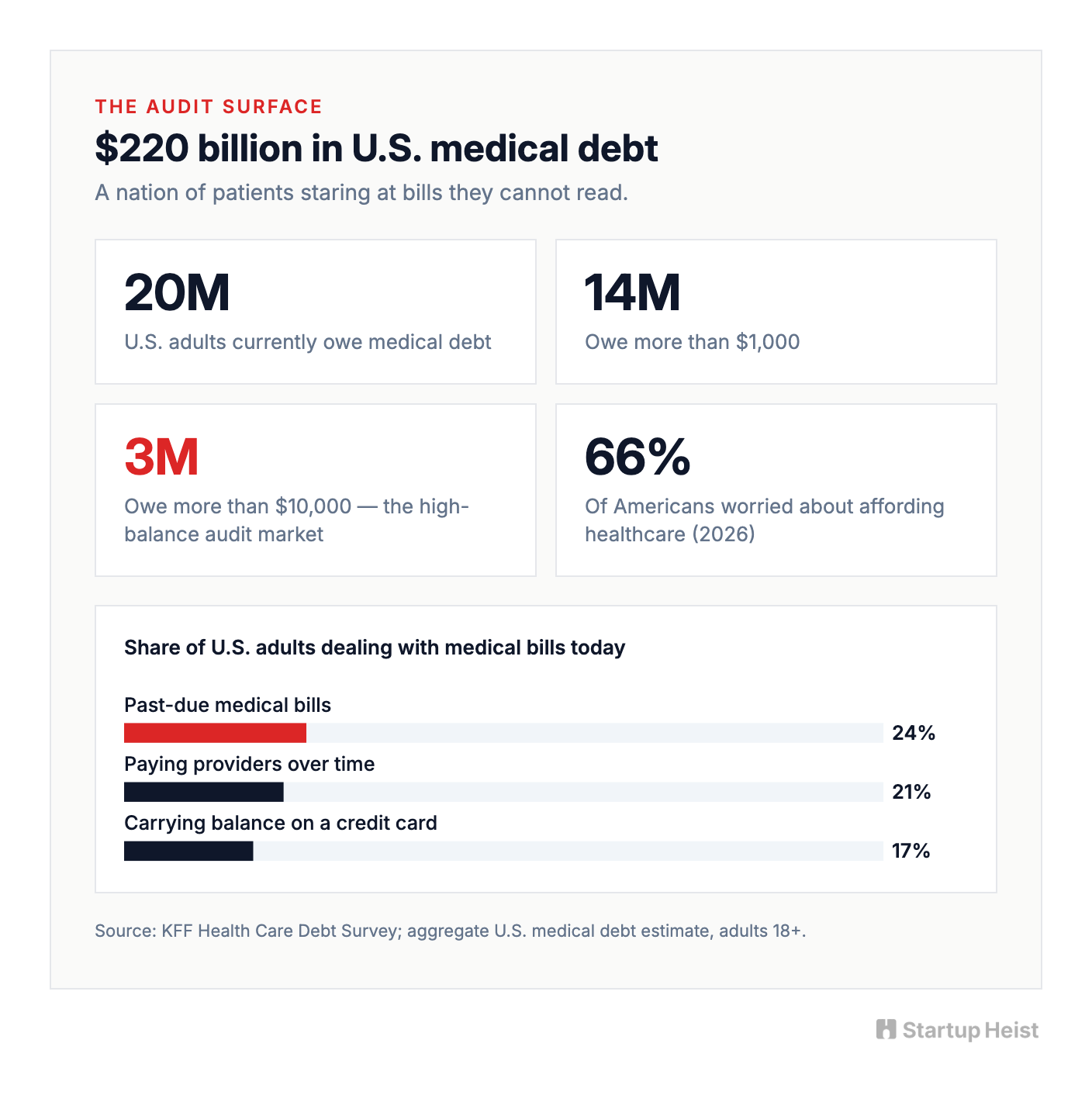

KFF puts U.S. medical debt at roughly $220 billion. About 20 million adults owe it, 14 million owe more than $1,000, and 3 million owe more than $10,000. Pull the lens back and 24% of adults have past-due medical bills, 21% are paying providers over time, and 17% are carrying medical balances on a credit card. As of early 2026, 66% of Americans say they're worried about affording healthcare. Two thirds of the country is one ER visit away from a financial event.

Stack that against industry studies that find 49% to 80% of medical bills contain at least one error. The Medical Billing Advocates of America estimates three out of four hospital bills have mistakes, and the average bill above $10,000 carries about $1,300 in overcharges. The audit surface is enormous, and the patient is staring at a document the hospital itself probably cannot fully defend.

The obvious startup pitch is "upload your bill, let AI fight the hospital." That pitch is too broad, too easy to copy, and too quick to overpromise. The serious version is an AI-assisted medical bill audit tool that parses hospital bills, benchmarks charges against public price transparency data, screens for hospital financial assistance eligibility, and generates the right dispute or hardship packet, with human review for high-value cases. Less "AI writes angry emails," more TurboTax for fighting hospital bills. It doesn't promise a refund. It promises competence at a moment of fear.

Here's the opportunity in one frame:

The money: 300 paying users a month at a $99 average packet fee gets you to roughly $30K MRR before the success-fee tier. Goodbill validated the demand.

Inside:

• Five-module MVP, shippable in 8-12 weeks

• Pricing ladder: $39, $99, $249, success fee

• SEO + community GTM with hospital pages

• Financial-assistance wedge competitors ignore

• The four-layer moat that compounds with use

Why this window opened in 2026

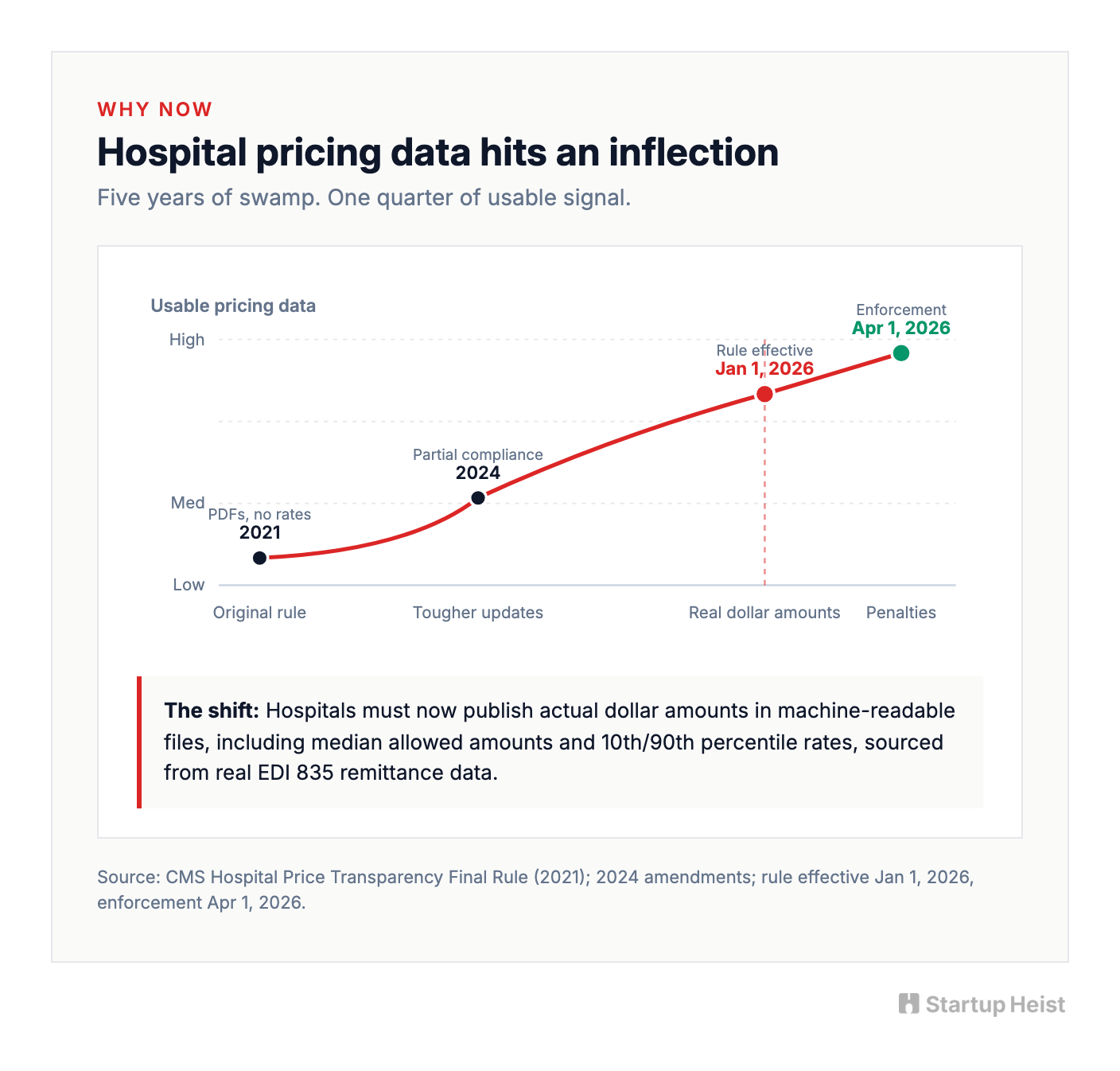

Hospital price transparency rules have technically existed since 2021. The data was a swamp. PDFs without rates. Spreadsheets without keys. Estimated allowed amounts that estimated nothing.

That changed when CMS finalized a tougher round of updates to the Hospital Price Transparency rule. The new requirements took effect January 1, 2026, with enforcement beginning April 1. Hospitals must now publish actual dollar amounts in their machine-readable files, including the median allowed amount and the 10th and 90th percentile allowed amounts when negotiated rates are based on percentages or formulas. They must pull from real EDI 835 remittance data. The era of "we cannot really tell you what we charge" is officially closed.

A patient cannot suddenly compare every line on every bill with surgical precision. Hospital billing is still a forest of negotiated rates, revenue codes, CPT codes, DRGs, facility fees, professional fees, and insurer-specific contracts. Imperfect is still useful. Enough structured pricing data now exists for an audit assistant to say things that were impossible to say cleanly two years ago:

This line item appears materially higher than the median allowed amount published by this hospital.

This bill lacks itemization. The first move is to request one.

This balance may not even be due yet.

The second catalyst pushes from the opposite direction. On July 11, 2025, a federal court in Texas vacated the CFPB rule that would have stripped tens of billions in medical debt from the credit reports of 15 million Americans. Medical debt is back on credit files. Lenders can use it again. The pressure on patients to deal with hospital bills before they hit collections just spiked, and most have no idea where to start.

Three forces converge in the same window: usable pricing data, restored credit-score consequences, and a generation of patients who already trust AI tools enough to paste a bill into one. The window is open now.

The patient does not know what they are holding

The emotional pain is obvious. The operational pain is the real opening.

A patient does not know what kind of document they are looking at. A pre-insurance estimate? A final bill? An Explanation of Benefits, which isn't a bill at all? A facility charge or a separate professional-provider charge? A collections notice? A No Surprises Act protected service that should never have been balance-billed? That confusion is the product opportunity.

A useful audit tool does not say "you may want to negotiate." It says, in order:

- This is the type of document you uploaded.

- These are the codes and charges we found.

- These charges look worth challenging.

- These probably are not.

- This hospital has a financial-assistance policy.

- Based on your household size and income, you may qualify.

- Here is the exact packet to send.

- Here is the follow-up schedule.

- Here is when to escalate to a human advocate.

The product's value isn't magic. It's calm, structured compression: a terrifying pile of codes turned into a plan.

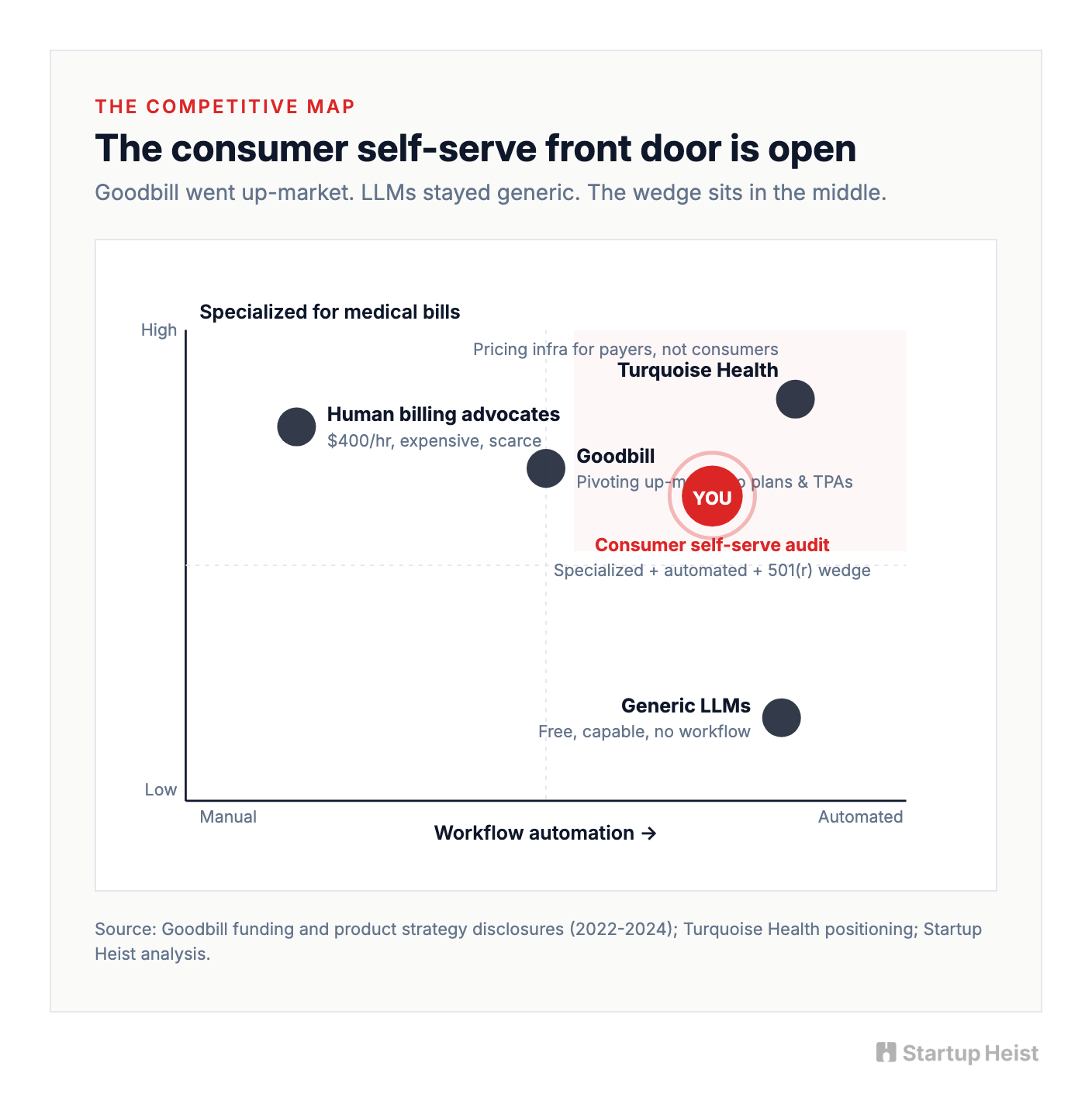

The competition

The total medical debt pool is $220 billion, but the addressable market for a startup is narrower than that headline suggests. Plenty of balances are too small to bother with. Some patients cannot pay anything regardless. Some bills are already in collections. Some require legal aid. Some are simply correct. The realistic early market is high-balance, pre-collections hospital bills where the patient still has time to dispute, negotiate, apply for financial assistance, or request itemization. Even narrowed that hard, it's large. A lean consumer product can run on three revenue layers: a low-priced self-serve audit, a mid-priced dispute packet, and a success-fee concierge tier for big balances.

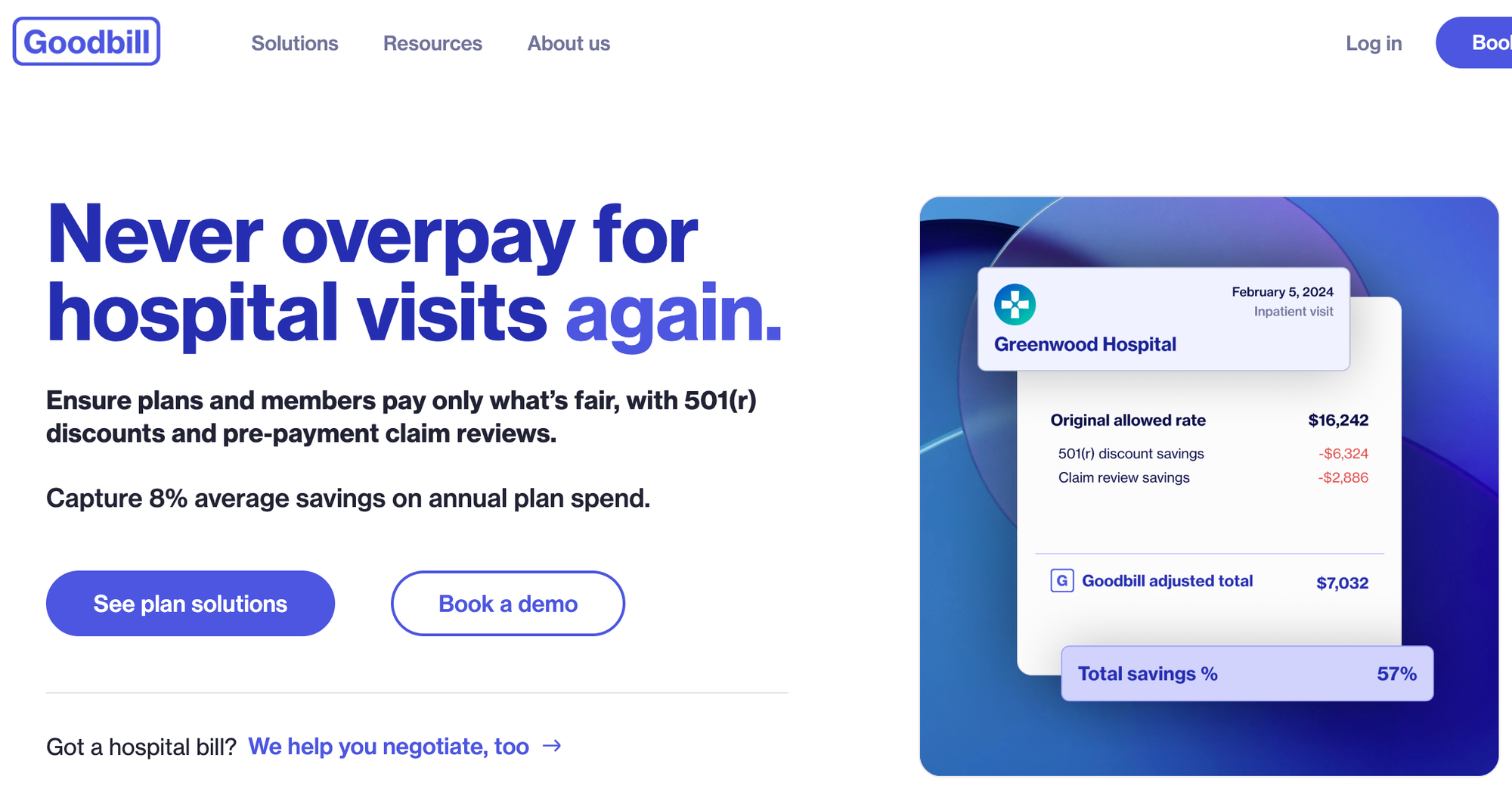

The competitive set looks crowded until you map it. Human billing advocates handle the high end well, but the model is manual, often expensive, and rarely under $400 an hour. Goodbill, the Seattle startup founded in 2022 by Patrick Haig and Ian Sefferman, runs medical coding audits, negotiates on the patient's behalf, and charges 15% of realized savings with no upfront fee. After an initial $3.4M seed, Goodbill raised another $2M in 2024, bringing total funding to roughly $5.4M, and has materially pivoted toward selling into health plans, employers, and TPAs. That move up-market validates the model and quietly leaves the consumer self-serve front door more open than it looks. Above the consumer layer, infrastructure companies like Turquoise Health do the hard work of normalizing hospital pricing files for payers and employers. They aren't consumer dispute products, but they validate the data opportunity.

The biggest long-term threat is the cheapest. A motivated patient can already drop a PDF into ChatGPT or Claude and get useful answers. One 2026 case made the rounds when a patient used Claude on a $195,000 hospital bill and negotiated it down to $33,000, an 83% reduction, after the AI flagged duplicate charges, illegal codes, and markups flagged by the AI of up to 2,300%. Stories like that train consumers to expect the product to exist.

So the moat cannot be "LLM writes a letter." That commodity is already free. The moat is the system around the model: specialized document parsing, hospital-specific policy lookup, pricing-data normalization, confidence scoring, workflow execution, case history, proof of outcomes. Patients won't pay for AI. They'll pay for something that knows what to do next.

The financial-assistance wedge nobody is using

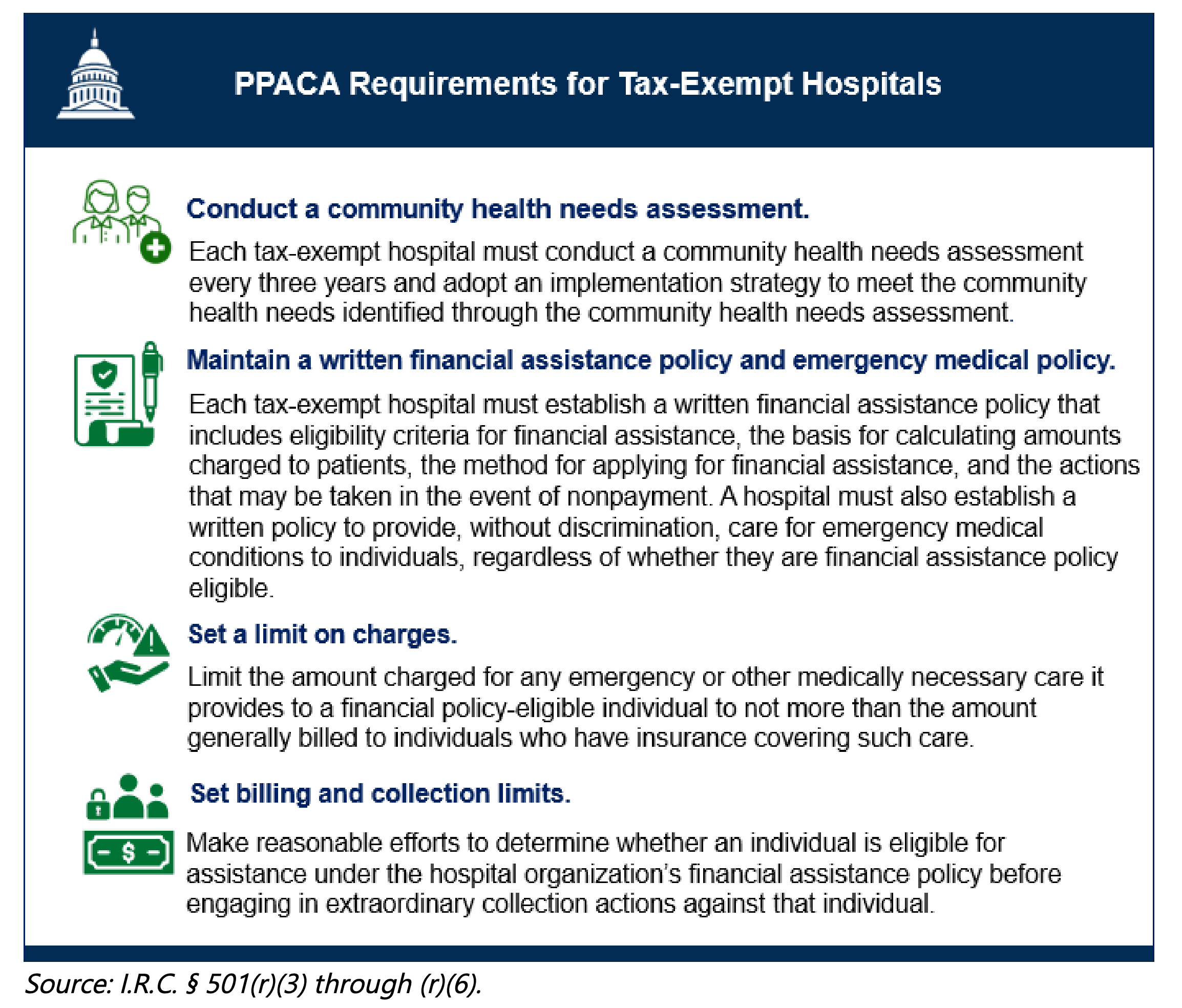

Under IRS Section 501(r), every nonprofit hospital in the United States is required to maintain a written Financial Assistance Policy. It must define eligibility, lay out discount tiers, list covered providers, and be widely publicized in plain language in the ER, online, and on request. Hospitals must attempt to determine assistance eligibility before pursuing extraordinary collection actions. Nonprofit hospitals that fall out of compliance with 501(r) risk losing their 501(c)(3) tax-exempt status, a devastating consequence for systems that lean on tax-exempt bond financing and charitable contributions.

Most patients have no idea this exists. Many never read the back of the bill. Some hospitals technically comply with publication requirements while making the application maze almost impossible to navigate. A hospital bill audit product should ask the harder, more useful question. Not just "was this charge too high," but should this patient have been billed this much at all?

Building a hospital-by-hospital database of 501(r) charity care policies is unglamorous data work. Income thresholds, household-size rules, discount tiers, asset tests, residency requirements, application forms, required documents, submission methods, response timelines, appeal processes. It's tedious, it needs maintenance, and it's exactly the kind of asset a casual copycat won't bother to build. A first product that leads with "check if your hospital bill qualifies for assistance or reduction" and layers price audit underneath earns trust faster than one that opens with "fight your bill." It's also more often the right answer.

The product

Build a web app. Skip the Chrome extension. Skip the mobile app on day one.

Bills arrive as PDFs, portals, photos, letters, EOBs, and screenshots. The user needs a clean upload-and-review surface, not a browser button. Mobile can come later. Web is faster, easier to support, and better for document review.

The MVP has five modules.

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”