The Insurance Claim Verifier the Mid-Market Will Actually Buy

In April 2026, three Los Angeles-area residents were sentenced for a scheme that felt more like a Coen Brothers plot than an insurance case. They staged fake bear attacks inside a 2010 Rolls-Royce Ghost, a 2015 Mercedes G63 AMG, and a 2022 Mercedes E350, filed roughly $142,000 in claims across multiple carriers, and almost got away with it. Operation Bear Claw unraveled when a California Department of Fish and Wildlife biologist watched the footage and concluded the animal was "clearly a human in a bear suit." Detectives later recovered the costume from the suspects' home.

The story is funny because the lie was visible to the naked eye. Primitive fraud gets caught by primitive review. The next wave of AI claim fraud won't look like a man in a cheap costume. It'll look like a perfectly lit photo of a totaled bumper that was never actually damaged.

Here's the opportunity:

The money: 10 mid-market carriers at $6K/mo platform fees = $720K ARR; pilot-led path to $3M–$10M ARR before deepfake detection insurance becomes a crowded category.

Inside:

• MVP scope for a 6-8 week intake wedge

• Hybrid pricing: platform fee + per-scan

• SIU-first cold outreach that converts

• Three-layer moat and 12-month playbook

The problem has already moved

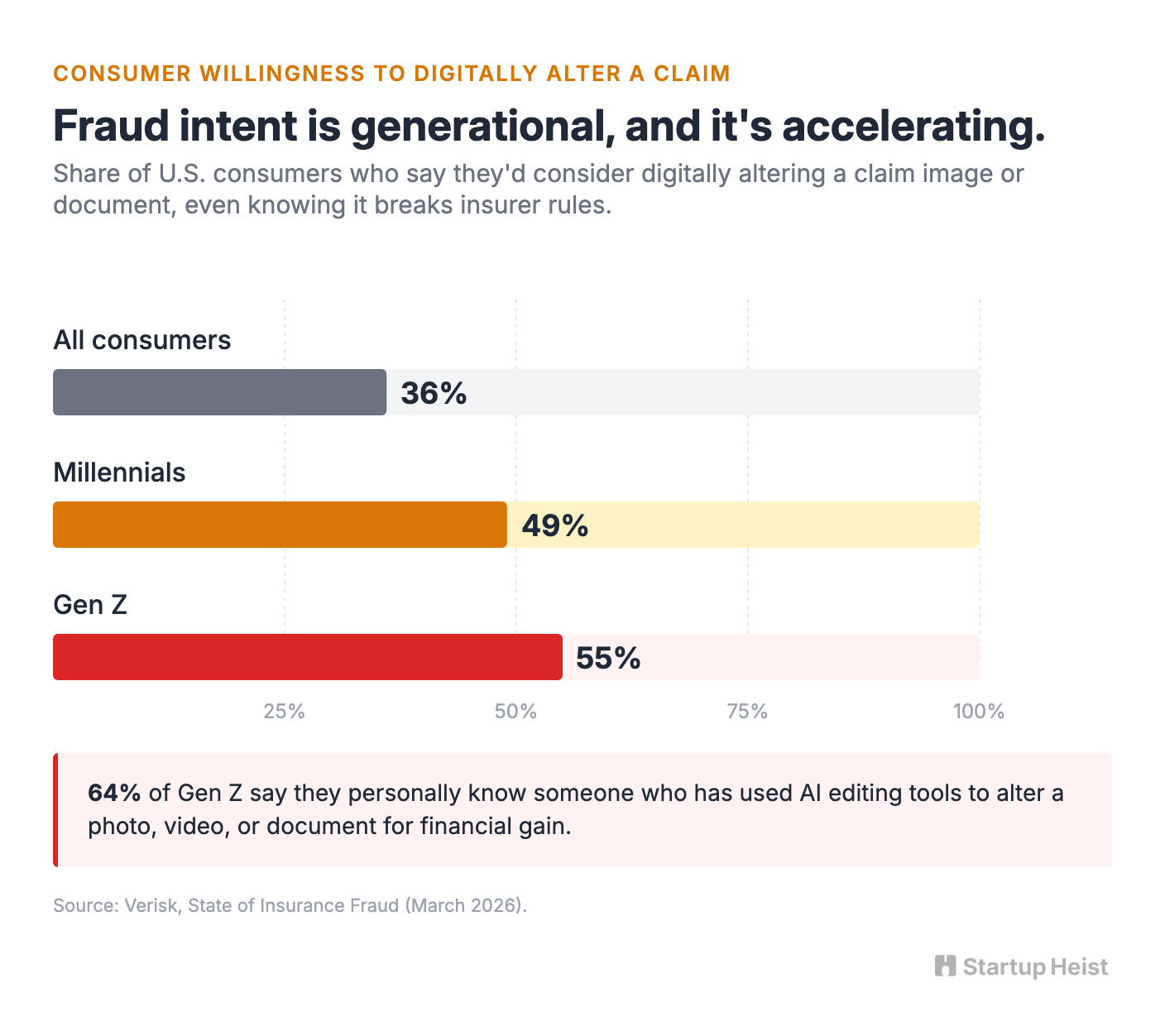

In March 2026, Verisk published its State of Insurance Fraud study and the numbers are blunt. Thirty-six percent of consumers said they'd consider digitally altering a claim image or document, even knowing it breaks insurer rules. That figure rises to 55% for Gen Z and 49% for millennials. Sixty-four percent of Gen Z respondents said they personally know someone who has used AI editing tools to alter a photo, video, or document for financial gain. Nearly half of consumers who have actually used these tools describe the output as "very realistic."

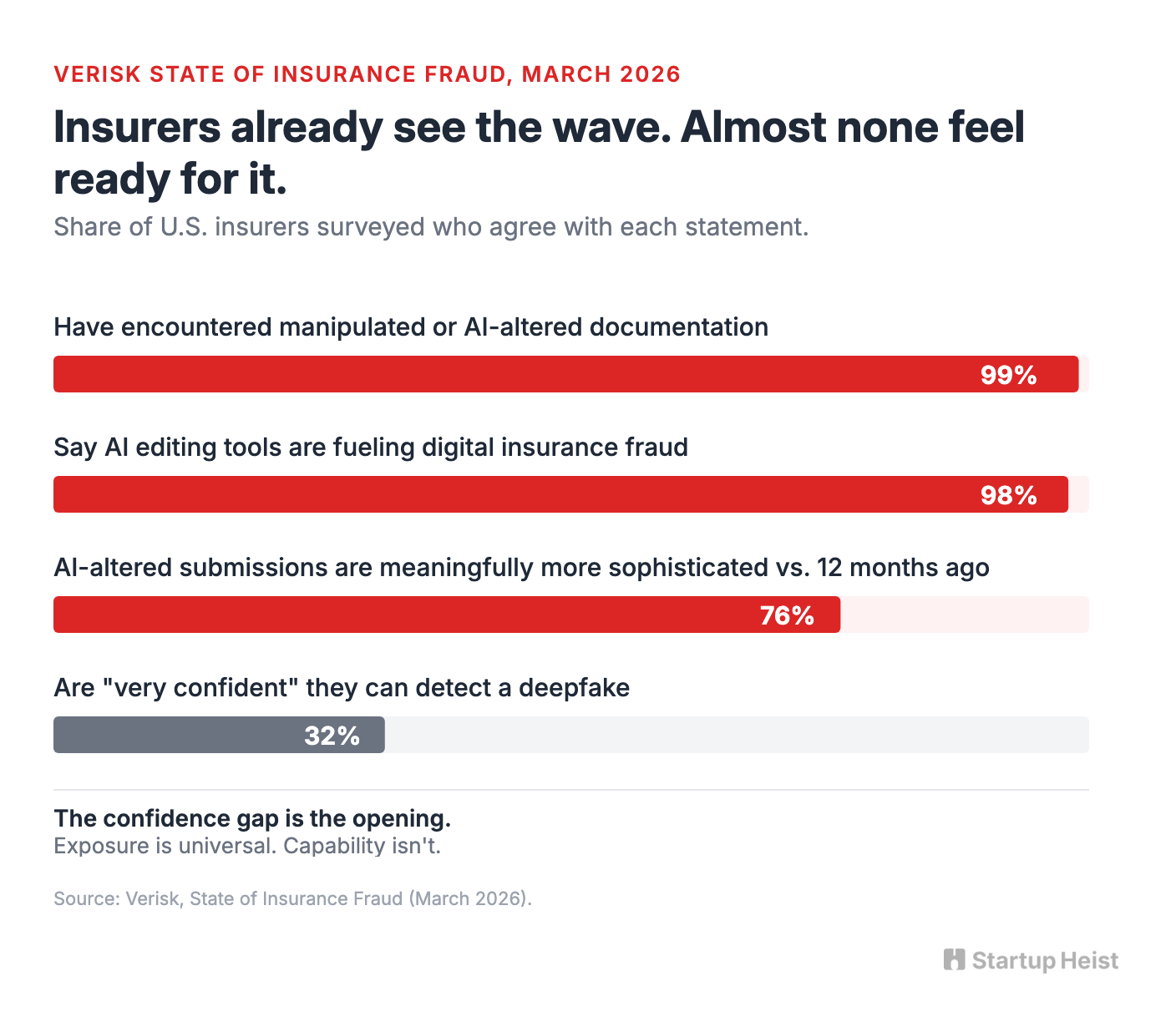

The insurer side of the survey is worse. Ninety-nine percent of insurers said they've already encountered manipulated or AI-altered documentation. Ninety-eight percent said AI editing tools are fueling digital insurance fraud. Seventy-six percent said AI-altered submissions have become meaningfully more sophisticated in the last twelve months. Only 32% said they were very confident they could detect deepfakes.

In April 2026, Admiral reported a 71% year-over-year jump in fraud, attributing the spike directly to AI-fabricated evidence and manipulated claim photos. A separate industry report found that 42% of U.S. carriers say AI and digital tools are already being exploited for fraud inside their claims pipelines. The attackers are mainstream customers with free apps, not underground rings with bespoke models.

Where the incumbents win, and where they don't

The reflex read is that Verisk, Guidewire, and the other giants eat this market. They probably will eat the top of it. Verisk already sits inside the workflows of the largest carriers and keeps getting more entrenched because proprietary insurance data compounds over time. Guidewire owns the core claims stack for many Tier 1 insurers and is already publishing on how C2PA content credentials should flow through claims systems. Strong position.

They won't eat the whole market. There are more than 3,800 P&C insurance companies in the United States. The majority are regional carriers, mutuals, farm bureaus, specialty auto and home carriers, and MGA-backed programs. They have real fraud exposure, real claims volume, and real budget constraints. What they don't have is the appetite for an eighteen-month platform transformation just to answer a simple operational question: should this photo, video, or document be trusted before we pay on it?

A few vendors have circled the problem from different angles. FRISS runs a Trust Automation platform for P&C insurance software buyers with 175+ insurers in 43 countries and strong fraud scoring across underwriting and claims. Attestiv is closest in spirit, with AI-powered media forensics built specifically for insurance and a Duck Creek integration that already puts it inside some mid-market claims stacks. Reality Defender is the general-purpose incumbent, with a public deepfake detection API, a free tier offering 50 scans per month, and SDKs for most major languages.

Every serious player here either sells a broader platform the mid-market can't absorb, or sells a generic detector that a mid-market claims operator has no obvious path to deploy inside FNOL. Attestiv has the cleanest beachhead of the three, which means the insurance-native, lightweight, intake-layer wedge is under-penetrated rather than empty. The job is to outflank Attestiv on focus and velocity, not to pretend the category is a blank sheet. The NAIC still cites roughly $45 billion in annual P&C insurance fraud costs. Even if only a sliver is media manipulation today, the glide path is obvious. Mid-market P&C is where the problem is compounding fastest and the tooling is weakest.

What the product actually is

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”