Most fraud software is built for the part of the problem banks like to talk about: detection.

The part they still handle with Word docs, Outlook folders, case notes, and nervous judgment calls? That's where this opportunity lives.

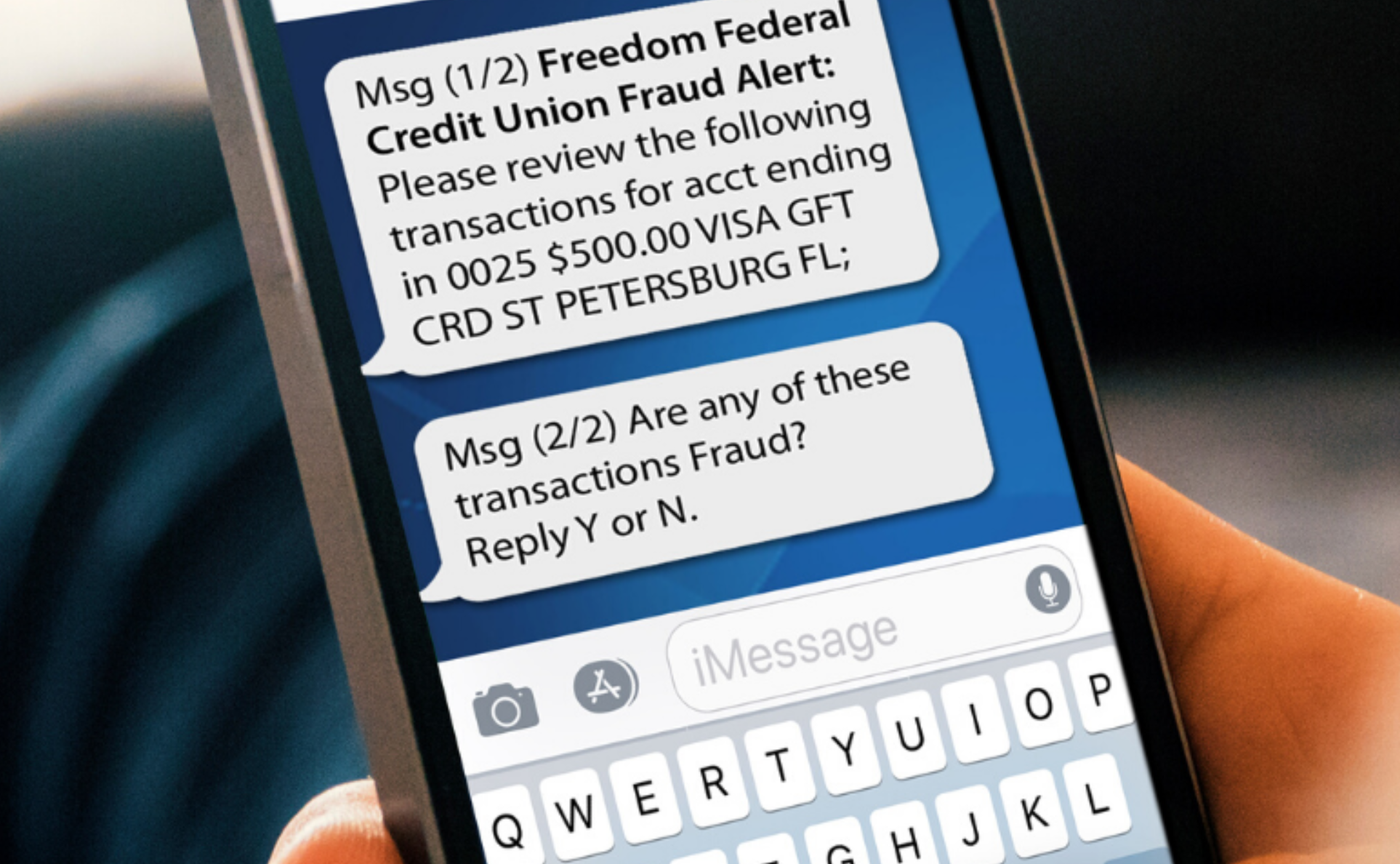

A member walks into a credit union branch after sending a "voluntary" wire to a crypto exchange. An older customer insists the investment platform is legitimate because her online boyfriend helped her set it up. A fraud analyst knows the transaction smells wrong, but now the institution has to reconstruct the story, flag suspicious activity, decide how to escalate, document what happened, and prepare something that will survive compliance review, board scrutiny, or a regulator asking questions six months later. Transaction monitoring doesn't help here. This is an investigation-ops problem — and nobody has built the right tool for it yet.

The money: 25 institutions at $15K ARR plus consultant channel revenue puts a solo founder at $30K-$80K MRR with high retention.

Inside:

• Six-module v1 product scope

• Consultant-first go-to-market playbook

• Pricing tiers and revenue model

• Moat strategy: workflow intimacy

The Pressure Is Compounding

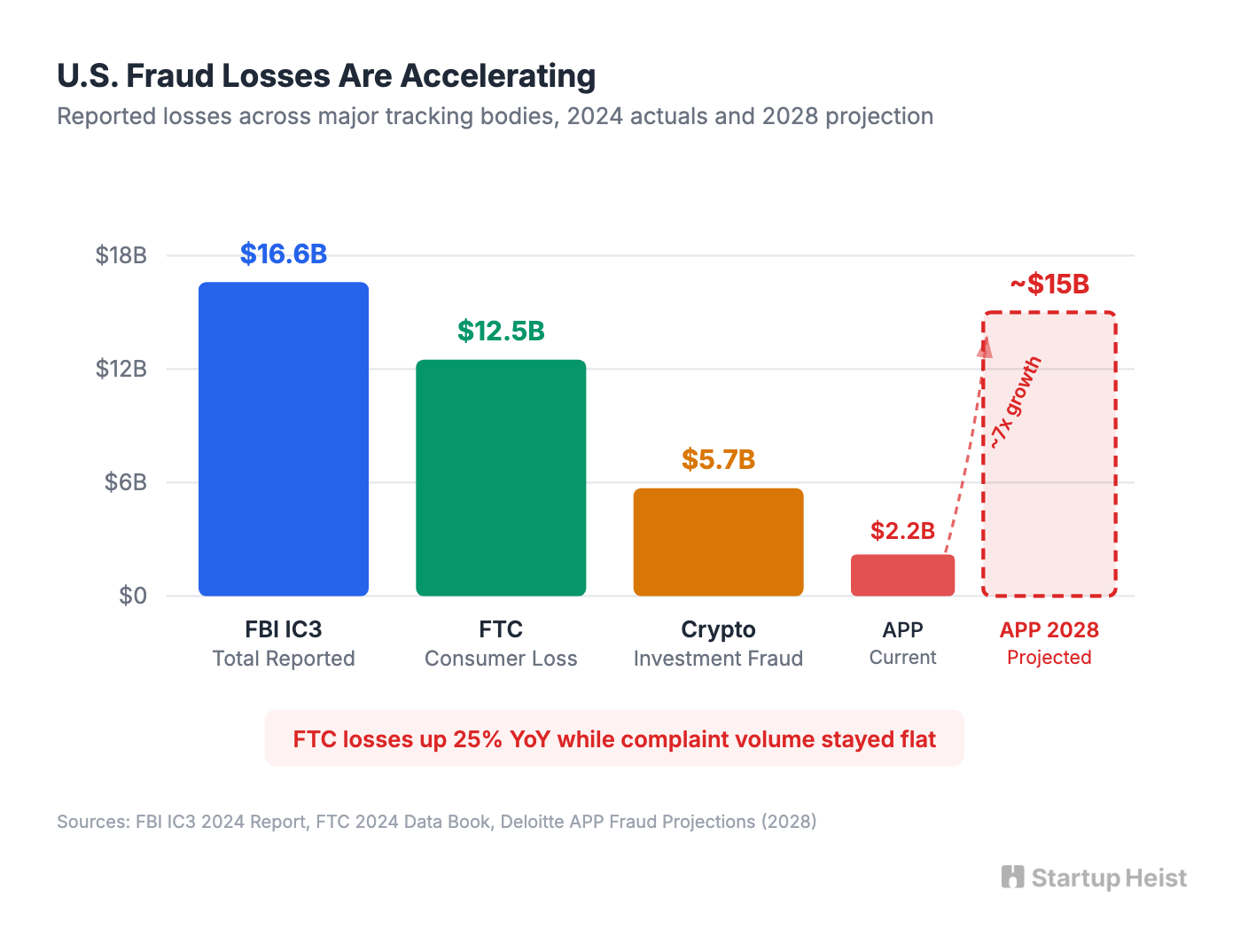

Losses are accelerating. The FBI's 2024 IC3 report recorded $16.6 billion in total reported losses. Crypto investment fraud alone generated more than 41,000 complaints and $5.7 billion in damages. Non-investment authorized push payment fraud in the U.S. hit $2.16 billion, with Deloitte projecting total APP losses reaching nearly $15 billion by 2028. The FTC reported consumers lost more than $12.5 billion to fraud in 2024, up 25% year over year, while complaint volume stayed stable. Severity is rising, not just noise. People in their 70s reported a median loss of $20,000 to investment scams.

Pig-butchering has gone mainstream. Chainalysis reported a nearly 40% revenue increase in 2024, and its 2025 report labeled compound infrastructure behind these schemes a national security threat. The U.S. Treasury sanctioned Myanmar and Cambodia scam-center operators in September 2025. Reuters reported in March 2026 that the scheme is becoming a meaningful legal and compliance risk for U.S. financial institutions because the payments are customer-authorized even when plainly induced by fraud. The FBI's Operation Level Up has notified more than 8,100 victims and prevented an estimated $511 million in losses. FinCEN published specific red flags and SAR guidance, including a designated filing term: "FIN-2023-PIGBUTCHERING." This is a named regulatory category with operational expectations.

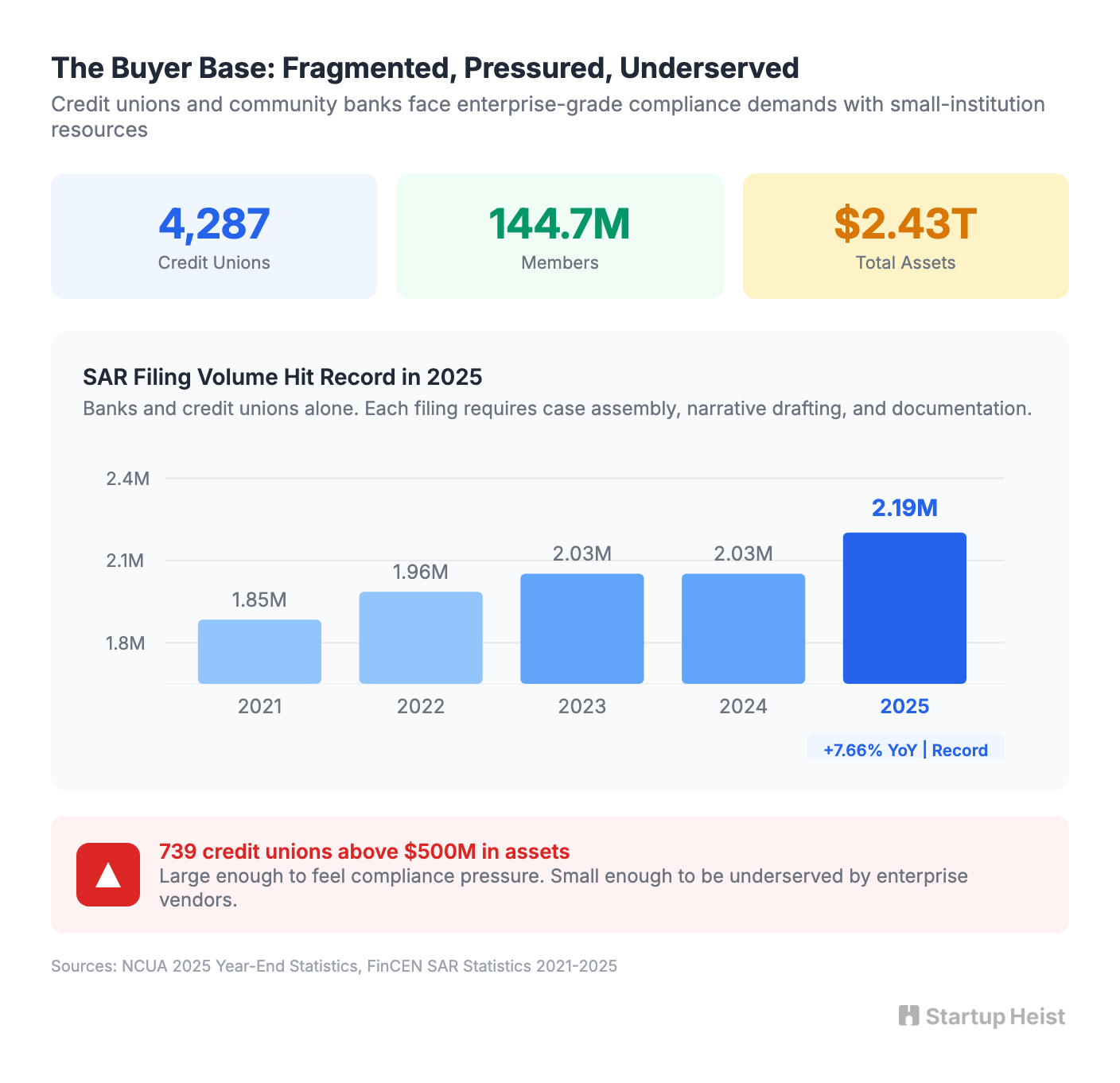

The buyer base is real and fragmented. Credit unions ended 2025 with $2.43 trillion in assets, 144.7 million members, and 4,287 institutions — 739 of them above $500 million. Large enough to feel compliance pressure. Small enough to be underserved by enterprise fraud vendors. SAR filings hit a record in 2025: more than 2.19 million from banks and credit unions alone, up 7.66% over 2024. Every one of those filings required someone to assemble a case, write a narrative, and produce a defensible document. The workflow behind each filing is where the pain concentrates.

The risk isn't theoretical. In 2023, the CEO of Heartland Tri-State Bank wired $47.1 million in a pig-butchering scheme, causing the bank's collapse. When authorized-fraud cases go wrong at small institutions, the consequences are existential.

The Wedge: Investigation Ops

Forget "AI fraud prevention" or "next-generation AML." Forget reimbursement decisions.

The wedge is authorized-scam investigation ops: a lightweight workbench for credit unions and community banks, purpose-built for pig-butchering cases, elder exploitation, romance-investment fraud, and related social-engineering incidents. It helps frontline fraud and BSA teams intake the case, reconstruct the timeline, capture red flags, draft SAR narratives, and produce regulator-ready files without buying an enterprise fraud stack.

Enterprise vendors already sell case management. Lucinity (named top vendor in the Datos Insights 2025 Fraud/AML Case Management Matrix), Feedzai, Quavo, CaseHUB by Quinte, and Abrigo all prove that investigation software is real budget territory. The pattern across these platforms is consistent: too broad, too enterprise, too detection-centric, or too dispute-oriented for the exact pain small institutions face in authorized-scam case assembly. Quavo optimizes for Reg E claims and chargeback workflows — authorized-scam cases have no chargeback to initiate. Enterprise platforms assume dedicated IT teams and six-figure budgets. No purpose-built authorized-scam workbench for small institutions exists today. The real opening is understanding how a $900 million credit union handles a scam case when the evidence is half in email and half in a traumatized member conversation.

The Product: Six Modules for v1

1. Structured Intake

A guided case form for branch staff, call-center agents, and fraud analysts. It captures transaction type, amount, channel, customer age band, destination details, relationship narrative, urgency markers, prior warnings given, and whether the customer appears coached or under pressure. The fields are tuned to specific scam typologies: pig butchering, romance-investment fraud, elder exploitation, impersonation scams, P2P coercion.

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”