Last Saturday, about three dozen people marched through San Francisco's Pacific Heights to defend billionaires. They chanted "Gains from trade!" and "Grow the pie!" while counterprotesters in formal wear held signs reading "IT'S A CLASS WAR, AND WE'RE WINNING." Journalists nearly outnumbered the marchers.

The spectacle was organized by Derik Kauffman, a 26-year-old Y Combinator founder, to protest California's proposed Billionaire Tax Act — a one-time 5% levy on residents worth over $1 billion. The initiative, backed by healthcare union SEIU-UHW, set its residency cutoff retroactively to January 1, 2026. Billionaires who didn't leave before New Year's Day may already be on the hook — even though voters won't decide until November.

The response has been swift. Google co-founders Larry Page and Sergey Brin moved business entities out of state in December. Oracle's Larry Ellison reportedly sold his San Francisco mansion for $45 million. Peter Thiel formalized his Florida residency. By some estimates, hundreds of billions in billionaire wealth has already left California.

Billionaire taxes make great theater. But the real money isn't in that fight. It's in the quiet, avoidable carnage happening one rung down — among the founders, early employees, and startup operators who routinely hand six and seven figures to the IRS because the equity-tax system is a maze and nobody handed them a map.

Vest, a "Founder Tax OS" that sits between cap tables and tax filings, flagging landmines before they detonate and modeling decisions before they're irreversible.

> $1,200/year per founder on the B2C side

> $10K–$50K/year B2B contracts for companies that want their employees to stop panicking about equity

This is a $5K–$20K MRR business within 12 months — scaling past $20K–$100K MRR once the enterprise motion kicks in. Specialist routing fees on top (15–20% of engagement value on QSBS planning engagements that run $5,000–$15,000 each) add a high-margin layer that compounds with the user base.

First: The Landmines

Startup equity is designed to create wealth. The tax code is designed to take a piece of it. The gap between those two systems is where founders lose fortunes — usually because they missed a deadline or didn't understand a rule that a $600/hour tax attorney would have caught.

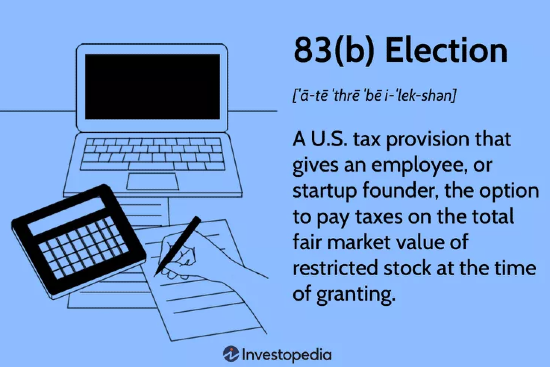

83(b) elections. You receive restricted stock in a startup. You have exactly 30 days to file a one-page letter with the IRS electing to pay taxes now — when the stock is worth pennies — instead of later, when it could be worth millions. Miss that window, and you'll owe ordinary income tax on every vesting tranche at fair market value. No extension. No do-over. The IRS started accepting electronic filings via Form 15620 in mid-2025, but the 30-day clock hasn't changed since the statute was written.

Concrete example: A founder gets 1 million shares at $0.001 per share. With an 83(b), they owe tax on $1,000 of income. Without one, they owe ordinary income tax as shares vest — and if the company raises a Series A that values shares at $5, that first 250,000 shares vesting triggers a tax bill on $1.25 million of phantom income. No cash. Just a bill.

ISO exercises and AMT. Incentive stock options are supposed to be a perk. But when employees exercise ISOs and hold the shares, the spread between strike price and fair market value counts as income under the Alternative Minimum Tax — even though no money changed hands. For 2025, single filers get an $88,100 AMT exemption and married couples get $137,000. That sounds like a cushion until you exercise 5,000 shares with a $40 spread and suddenly have $200,000 in phantom AMT income. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently locked in higher AMT exemptions — but starting in 2026, the phaseout threshold drops, meaning more high-earning startup employees will get caught in the AMT net.

QSBS — the cheat code everyone accidentally disqualifies themselves from. Section 1202 lets founders and investors exclude up to 100% of capital gains on Qualified Small Business Stock held for five years. The OBBBA expanded this significantly: the per-issuer exclusion cap jumped from $10 million to $15 million (or 10x adjusted basis, whichever is greater) for stock issued after July 4, 2025, the gross asset threshold rose from $50 million to $75 million, and a new tiered system offers partial exclusions starting at three years. A founder with $20 million in QSBS gains can shelter the entire amount at the five-year mark. Zero federal tax.

But QSBS eligibility is shockingly easy to blow. Stock redemptions within certain windows can disqualify an entire round. Changing business models can kill it. Converting from an LLC to a C-corp requires precise timing. Moving to California — which still doesn't conform to Section 1202 at all — means you'll pay 13.3% state tax on gains the feds treat as tax-free. And documentation gaps can make it impossible to prove eligibility years later when it actually matters.

State residency timing. The California billionaire exodus is the extreme version of a problem that affects founders at every level. When you move from a high-tax state to a low-tax state matters enormously, and California's Franchise Tax Board is notoriously aggressive about claiming you're still a resident. They'll audit your family photos, your heirlooms, your utility bills, your gym membership. The delta between doing it right and doing it wrong on a $10 million exit can be $1.3 million in California state tax alone.

Tender offers and secondaries. When your company lets employees sell shares pre-IPO, the tax implications depend on ISO vs. NSO, holding periods, exercise dates, QSBS eligibility, and whether you've moved states since the grant. Most employees get a generic FAQ from HR and make irreversible decisions based on vibes.

Why Nothing on the Market Solves This

Carta manages cap tables for over 30,000 companies. Pulley offers equity management with tax transparency dashboards. Various firms provide 409A valuations.

None of them answer the question a founder actually has at 2 AM when their tender offer window closes in 72 hours: "If I do X on date Y, what happens to my tax bill?"

Your accountant shows up after the damage is done. They file the return. They tell you what you owe. The 83(b) window closed nine months ago. The AMT bill is already locked in. Autopsy, not strategy.

Specialist attorneys and CPAs can catch these things — but they bill $600–$1,000 per hour, operate on email threads and PDF attachments, and take weeks to get on the calendar. They're also reactive. You have to know enough to ask the right question before they can give you the right answer. Most founders don't know what they don't know.

The white space is the operating layer between cap tables and tax filings — a system that connects equity events to tax consequences in real time, flags deadlines before they expire, models scenarios before you commit, and routes you to a specialist when human judgment is required.

The Opportunity: Vest

An always-on decision engine between cap tables, transactions, mobility, and tax law. The ideal early customer: mid-to-late stage startup founders, senior employees, and anyone holding equity with $100K+ in plausible upside — people with enough at stake to pay for planning but not enough to retain a full-time tax strategist.

Nobody wakes up wanting a tax platform. They wake up with a moment of panic: My 83(b) window closes in 12 days. My company just announced a tender offer. I can exercise now but AMT might wreck me. We're moving to Austin — when is too late? Do I still qualify for QSBS if we restructure?

The Core Product

1. A "tax twin" of your equity life.

Connect cap table exports, grant details (ISOs, NSOs, vesting schedules, strike prices), 409A history, state residency, income bands, and planned equity events. The output: scenario models (exercise now vs. later, partial exercise, sell vs. hold, move timing), risk scores (AMT likelihood, QSBS risk, deadline risk, documentation gaps), and concrete action plans — what to do this week, this month, this quarter.

2. Event-driven playbooks.

These are the moat. A generic LLM can explain QSBS. It can't guide a founder through seven interconnected scenarios with documents, deadlines, edge cases, and escalation paths.

Build guided flows around how founders actually experience pain:

- 83(b) Sprint: Enter grant details → deadline countdown → filing steps → IRS Form 15620 walkthrough → proof-of-submission vault

- ISO/AMT Planner: AMT crossover estimate → staged exercise plan → year-by-year modeling to stay under exemption thresholds → disqualifying disposition analysis

- Tender Offer Decision: Sell amount optimizer → tax impact modeling → liquidity vs. QSBS holding period tradeoffs

- State Move Timer: "Move on date X vs. date Y" with expected tax delta → residency audit risk flags → documentation checklist

- QSBS Guardian: Eligibility checklist → holding period clock → disqualification alerts (redemptions, asset threshold breaches, business model changes) → state conformity warnings (California = 13.3% on gains the feds exclude)

- Departure Window: Post-termination exercise strategy → option expiration countdown → AMT impact of exercise timing

- Founder Liquidity Plan: Secondary sale structuring → basis planning → charitable giving angles (flag and route to specialist) → loan-against-equity options

3. Specialist routing.

This doesn't replace CPAs. It makes the best ones faster. The specialist receives a clean model, clean timeline, and clean docs. The user gets matched to the right expert — QSBS specialists, cross-border tax attorneys, AMT-heavy situations, residency disputes. The platform takes a fee on engagements.

This turns "I need a unicorn CPA who understands startup equity tax" into a repeatable marketplace where the pre-work is already done.

Why Now

The OBBBA created a two-track QSBS system that demands new planning. Stock issued before July 4, 2025 follows the old rules: five-year minimum hold, $10 million cap, $50 million asset threshold. Stock issued after follows the new rules: tiered exclusions starting at three years, $15 million cap, $75 million threshold. Every founder and investor now needs to track which shares follow which rules, and the planning implications diverge sharply depending on acquisition date. That complexity creates massive value for whoever builds the system that makes it legible.

State-level policy is fracturing. New Jersey adopted QSBS conformity starting January 2026. DC decoupled from expanded QSBS in late 2025. California still doesn't recognize Section 1202 at all — and now wants to add a billionaire wealth tax on top. The rules are changing faster than any individual can track without a system.

AI-era wealth creation is minting new equity holders at unprecedented speed. California alone added an estimated 50 new billionaires last year, driven by AI companies. Below the billionaire line, thousands of engineers, product managers, and early employees at AI startups are holding equity that could be worth millions. Most of them have never dealt with equity tax planning before. The addressable market just expanded by an order of magnitude — and it's populated by people who are tech-savvy, willing to pay for good tools, and acutely aware that they need help.

Moats

Data moat. Cap table tools see ownership. Tax preparers see filings. This product sees decisions. Over time, you'll own the longitudinal dataset of when founders exercise relative to rounds, how often QSBS eligibility is preserved vs. accidentally blown, state move timing vs. liquidity events, and AMT pain distribution across income bands. That becomes benchmarking, portfolio analytics, and a compounding advantage no new entrant can replicate.

Workflow moat. The playbooks — 83(b) Sprint, QSBS Guardian, AMT Planner — become institutional memory. Each edge case handled, each deadline tracked, each scenario modeled makes the system harder to replicate. If you encode how the best lawyers and CPAs actually think and continuously refine those workflows based on outcomes, you're building differentiated labeled data that generic tools can't match.

Distribution moat. If this becomes the default "tax readiness stack" in founder ecosystems — embedded into accelerator onboarding, VC portfolio support, and cap table platforms — switching costs become social, not technical. The earlier you embed, the stickier you get.

MVP: Ship Fast Without Pretending You're a Law Firm

Inputs: Manual entry plus CSV imports from cap table platforms. Basic profile: state, income band, filing status, grant data, 409A history, planned events.

Core features:

- Scenario engine for ISO/NSO exercise timing, AMT exposure estimates with staged exercise plans, and tender offer "sell vs. hold" modeling

- Deadline engine: 83(b) 30-day timer, post-termination exercise windows, QSBS holding period clock

- Tax Risk Dashboard with red/yellow/green alerts and plain-English explanations

- Document vault: store grants, filings, 83(b) proof, board approvals

- Specialist routing: intake form plus one-click "share my model" packet

Legal posture: Education, modeled scenarios with stated assumptions, risk flags, and referral to licensed professionals. Not tax advice. This distinction is load-bearing — if the product looks too much like a tax advisor, regulators and professional bodies may treat it as one. Reinforce the boundary in UI, contracts, and marketing.

V2: Event triggers (new round, 409A update, tender offer), deeper cap table integrations, employer SKU, and "decision receipts" — auditable records of what you decided and why.

Validation shortcut: Before building anything, run a non-code or light-code "Vest Checkup" that manually walks 50–100 real founders and employees through 83(b)/ISO/QSBS/state-move questions and returns a simple risk report. You'll learn what they actually care about, what they'll pay for, and where their confusion peaks. Partner with a small, progressive tax firm to co-design one or two playbooks in exchange for early access to referred clients — this ensures the workflows reflect how experts actually think.

Pricing

B2C: Founders and early employees

- Starter: $299/year — Dashboard, deadlines, doc vault, basic scenarios

- Pro: $1,200/year — Full scenario engine, QSBS Guardian, tender modeling, move timer, priority support

- Concierge: $2,500/year + specialist fees — Annual specialist review, two event consults, pre-built packets

B2B: The stealth bigger market

Equity confusion kills trust. It also hurts retention. When employees don't understand their options, they make bad decisions — or they leave for companies where the equity story is clearer.

- Team Plan: $10K–$50K/year (scaled by headcount and complexity) — Employee self-serve modeling, exec tier, education modules, specialist routing

The B2B pitch: comp ROI, retention, risk reduction. Every HR leader has dealt with an employee who panicked about a tax bill they didn't understand. Expect 12–18 month sales cycles for meaningful ACV deals unless you already have embedded relationships — which is why the VC platform pilot strategy matters.

Go-to-Market

Use the news cycle as the hook. The billionaire tax debate is free distribution. Your angle isn't political — it's practical: stop lighting money on fire because you missed a deadline. Every headline about billionaires fleeing California reminds founders that equity-tax planning matters and most of them don't have a plan.

Launch a "Vest Checkup" lead magnet. Seven minutes. Enter your equity situation. Get your top three risk flags, two recommended actions, and a countdown of upcoming deadlines. Then upsell to Pro.

Partnerships that compound. Accelerators and founder communities embed this into onboarding. VC platform teams use it as portfolio support — they want founders building, not panicking about AMT. Cap table tools like Carta and Pulley are natural distribution partners because they don't want the liability of giving tax guidance, but their users desperately need it.

Case studies that convert. Anonymized stories hit both buttons founders respond to — competition and fear:

- "Seed founder saved $340K by exercising before Series A and filing 83(b) on time"

- "Employee avoided $180K AMT surprise with staged ISO exercise plan"

- "QSBS eligibility preserved through corporate restructure — saving $1.5M on exit"

Outreach Templates

VC platform teams

Subject: Eliminate portfolio equity tax landmines (83b, AMT, QSBS)

Hi [Name] — quick one.

A huge chunk of portfolio value leaks through avoidable equity tax mistakes: missed 83(b) windows, AMT surprises on ISO exercises, and QSBS eligibility getting accidentally blown.

Vest flags top risks per founder and exec, models exercise/tender/move timing scenarios, and routes to vetted equity-comp specialists with a pre-filled packet.

Happy to run a free "Vest Checkup" for 5 portfolio founders and share anonymized risk patterns back to your team. Worth 15 minutes?

Startup CFO / Head of People

Subject: Equity education that improves retention

Hi [Name] —

Equity is supposed to retain talent. Instead it creates stress: employees miss deadlines, misunderstand exercise costs, and get blindsided by taxes.

This stack provides self-serve modeling for exercise and tender decisions, deadline tracking (83b, post-termination windows), an exec tier for senior staff, and specialist routing when needed.

It's cheaper than one "equity panic" incident and shows up directly in retention and trust. Open to a quick call?

Founder direct (DM / community)

Subject: Quick QSBS / AMT risk check?

If you hold private-company equity, there's a decent chance you have a silent landmine: 83(b), AMT on ISO exercise, or QSBS clock risk.

A free 7-minute checkup outputs your top 3 risks, what to do next, and what not to do. Want the link?

Revenue Potential

At $1,200/year for Pro users:

- 500 subscribers = $600K ARR

- 2,000 subscribers = $2.4M ARR

- Add B2B contracts at $25K average = another $500K–$2.5M

With specialist routing fees (15–20% of engagement value), the marketplace layer adds a high-margin revenue stream that grows with the user base. A single QSBS planning engagement can run $5,000–$15,000 — your cut on a few hundred of those per year is material.

This is a $5K–$20K MRR business within 12 months with focused execution, scaling to $20K–$100K MRR as the B2B motion kicks in.

Risks and How to Manage Them

Liability and advice boundaries. Win by being the modeling and workflow layer, never the advisor. Clear disclaimers, stated assumptions, and "needs specialist review" flags on every output. Route to licensed professionals when judgment is required. The "holding out" risk is real — if your product looks too much like it's giving tax advice, state bar associations and state boards of accountancy can come knocking.

Data accuracy. Start conservative. Show confidence levels. Flag edge cases. The worst outcome is a user making a decision based on a wrong model, so build in friction before irreversible actions. Every recommendation should show its assumptions, ranges, and links to the underlying rules so professionals are comfortable blessing or adjusting them.

Integrations take time. Start with exports and CSV parsing. Build APIs after traction. Don't let perfect integrations delay a product that works with manual input.

Specialist supply. Many high-end equity-comp tax professionals are fully booked and wary of platforms. Start with a smaller, tech-friendly subset willing to experiment. The referral marketplace only works once you can demonstrate clean intake packets and clients who convert.

"AI will commoditize this." The moat isn't a prettier chatbot. It's structured playbooks, event triggers, decision data, distribution into founder ecosystems, and the specialist network. ChatGPT can explain 83(b) elections. It can't track your specific 30-day deadline, model your AMT exposure against your actual income, or alert you when a corporate restructure threatens your QSBS eligibility.

The Takeaway

The "March for Billionaires" will be forgotten by next week. The opportunity behind it won't.

Founders and early employees are making irreversible equity decisions with incomplete information. The tax code just got more complex — OBBBA changed QSBS, AMT, and holding period rules simultaneously. State policy is more volatile than it's been in decades. And the population of equity holders is growing faster than the supply of advisors who understand this stuff.

The only question anyone cares about: "What should I do right now — and what happens if I wait?"

Vest answers it.