On January 23, 2026, Substack released TV apps for Apple TV and Google TV, putting creator video on the biggest screen in the house. The move makes sense — video posts and livestreams now have a lean-back destination. What doesn't get discussed enough is what the app includes: a "For You" algorithmic feed mixing subscribed content with recommendations.

That single feature triggered immediate backlash. "Please don't do this. This is not YouTube. Elevate the written word," one creator wrote. Another: "You guys have gone from saying Substack is the best home for longform writing to 'Substack is the home for the best longform—work…'. I get trying to evolve, but this just seems like another venture capital-fueled idea."

The criticism reveals the wedge. Substack needs video to compete with YouTube. Creators want distribution without becoming YouTubers. Those are incompatible goals — unless someone builds the format layer between them.

Your positioning becomes simple: stay a writer, and we'll turn your newsletter into a TV episode. This is a media-ops business with software leverage, not pure SaaS — you're building a boutique studio that productizes workflows, not shipping generic video tools. Three revenue tiers, first dollar at day 60:

- Creator Studio subscriptions at $39-$99/month establish format standards.

- Network partnerships at $1,500-$5,000/month plus revenue share handle aggregation and eventual FAST distribution.

- White label deals at $10,000-$25,000/month serve newsletter platforms competing with Substack.

Substack can chase watch time and algorithmic optimization. You build a system where writers keep their status while gaining distribution — monetization without requiring creators to learn lighting, editing, or on-camera performance.

This opportunity is real, time-bound, and has legs. It's also narrower and more operationally gnarly than most video tool pitches suggest. The core question isn't whether the category exists — it does. The question is whether enough writers in specific verticals (markets, AI, politics, longform investigations) actually want 10-20 minute TV episodes versus simpler video derivatives, and whether you can deliver watchable quality at profitable unit economics.

Why streaming TV actually matters right now

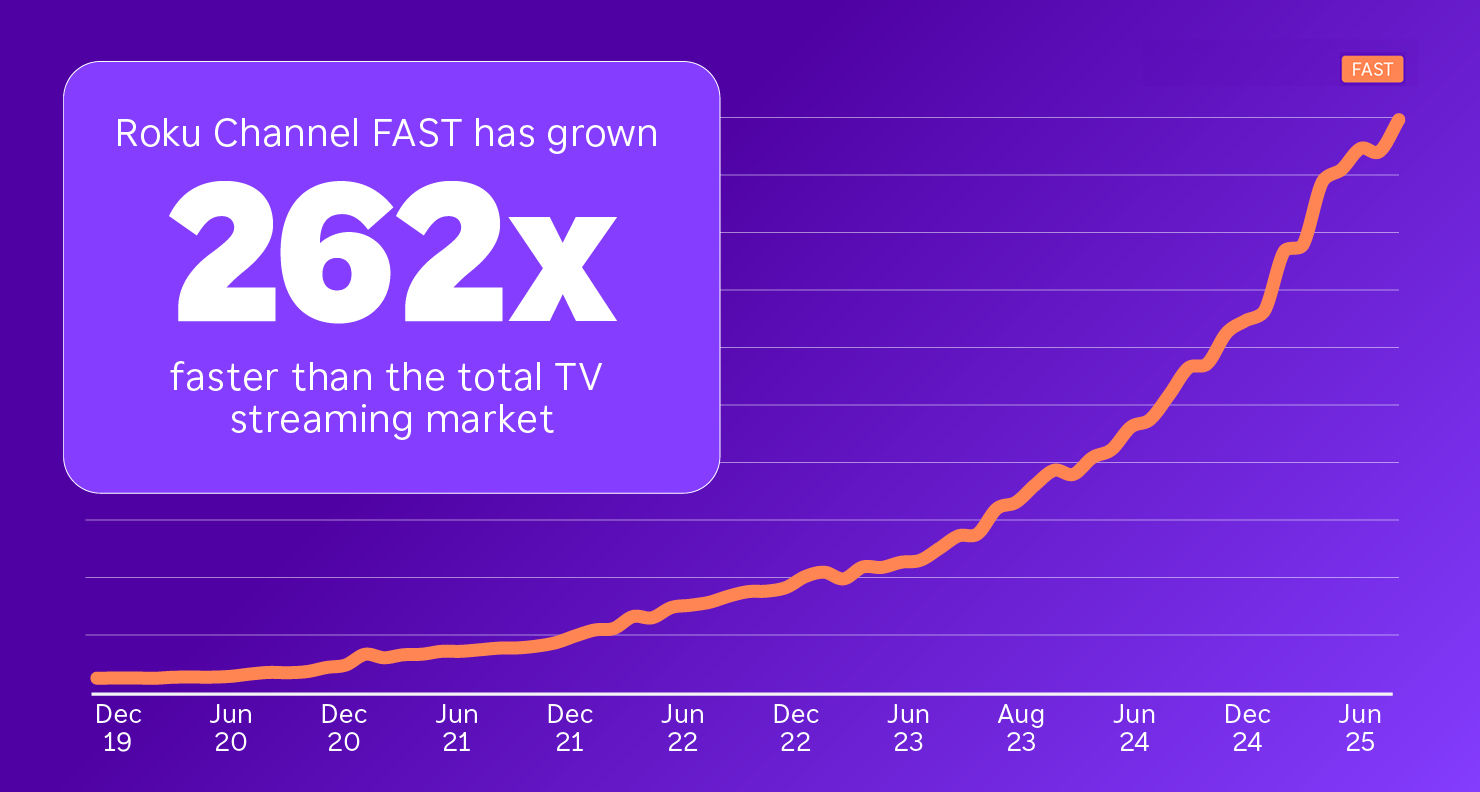

Television is reverting to channels. FAST (free ad-supported streaming TV) is built around schedules, lean-back viewing, and EPG grids — basically cable, but free. Roku reports that roughly two-thirds of Roku households now watch FAST channels, with 88% streaming free, ad-supported content overall.

Free ad-supported streaming television captured $4.9 billion in revenue in 2024 and is tracking toward $9 billion by 2029, according to PwC. That's a 13.8% annual growth rate in a mature market. FAST platforms — Tubi, Pluto TV, The Roku Channel — now account for 5.7% of total U.S. TV viewing time per Nielsen Gauge data from May 2025. That share exceeds the individual viewership of any single broadcast network.

The behavioral shift is clear. Streaming viewership (FAST plus subscription services) has surpassed cable and broadcast combined. Viewers want scheduled programming without subscription fees, and advertisers want reach without platform gatekeepers. CTV ad spend is one of the fastest-growing advertising metrics in PwC's broader outlook.

Substack is betting it can capture this shift by putting longform creator content on TV. The bet makes financial sense — connected TV advertising revenue is growing faster than any other video segment. But execution remains the problem. Newsletter writers don't have production teams. They have Google Docs and publish dates.

The actual market opening (and why it's defensible)

Text-to-video conversion tools already exist. Lumen5 starts at $29/month for watermarked output, with professional plans at $199/month. Pictory offers similar AI-powered conversion. Both focus on short-form social media content — 30 to 90 second clips optimized for Instagram and TikTok.

The opening isn't better stock footage selection. It's episodic TV formatting designed for 10-20 minute lean-back viewing. That requires different infrastructure: format standardization, aggregation economics, and distribution operations.

Format standardization means a recognizable grammar for "newsletter television" — cold opens, segment breaks, chapter cards, pause-to-read moments for data visualization. Consistency in pacing, visual language, and narrative structure that makes a channel feel like a channel, not a random collection of uploaded files. The quality bar here is high: generic TTS with stock footage won't cut it. You need episodes that people actually finish, which means investing in voice cloning, careful segment pacing, and visual rhythm that holds attention for 15 minutes.

Aggregation economics: individual creators can't negotiate FAST distribution. Individual creators can't hire playout engineers or manage ad insertion schedules. But thematic channels can. "AI Brief TV" programming 18 different AI newsletters into a 24/7 schedule has distribution leverage. "Macro After Dark" bundling six financial analysis writers into evening programming has advertiser appeal.

Distribution operations: FAST isn't "upload a video." FAST platforms expect continuous streams with EPGs (electronic program guides), dynamic ad insertion markers, proper encoding formats, metadata management, and rights tracking. Industry vendors — Amagi, Wurl, Frequency — handle this infrastructure but target enterprise customers with enterprise budgets.

The moat comes from solving aggregation and distribution as a unified product. Individual tools for "text-to-video" remain commodity. But a network that transforms 25 newsletters into programmed channels with managed distribution? That's operational complexity competitors won't replicate quickly.

Be clear-eyed: this is a media-ops business with software leverage, not a pure software company. Your early revenue comes from being a boutique studio that later productizes workflows. The margin lives in network partnerships and white label deals, not the software tier.

What makes this timing-specific

Three conditions align right now that won't stay aligned.

Substack's platform risk. The TV app announcement accelerated creator anxiety about algorithmic drift. Writers built businesses on "no algorithm" positioning. The "For You" feed breaks that promise, creating an opening for alternative distribution that respects writer control while adding reach. Substack is explicitly optimizing for longform video and watch time on its own app — their job is getting creators to make more native video. Your job is different: protect writer identity, offload production, give them multi-platform distribution.

FAST's supply shortage. Platforms need quality content to fill channels. Tyler Perry recently moved 600 hours of programming to BET's FAST channels. Roku reported 80% year-over-year growth in creator-led content viewing hours. The bottleneck isn't viewer demand — viewers already watch FAST for 5.7% of total TV time. The bottleneck is programming that holds attention beyond the first minute.

Distribution infrastructure maturity. Cloud playout services now start at $250/month for basic FAST channels. That's still too expensive for individual creators but economically viable for aggregated channels serving 10-15 writers. The infrastructure exists and is priced for mid-tier operations. Five years ago, minimum viable spend was 10x higher.

Roku's sunset of Direct Publisher in January 2024 killed the old "one-click Roku channel" path and forced distribution into more complex SDK or vendor-driven approaches. No more easy hacks — you need real infrastructure, which favors aggregators over individuals.

If Substack successfully pivots creators toward native video production, the "newsletter to TV" value proposition weakens. If FAST platforms saturate with quality content, the distribution advantage disappears. But right now? Undersupplied platforms, anxious creators, and accessible infrastructure create a 12-18 month experimentation window.

3-Tier Revenue model that scales beyond SaaS pricing

Pure software gets compared to Lumen5 pricing immediately. The better model layers monetization.

Tier 1: Creator Studio ($39-$99/month)

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”