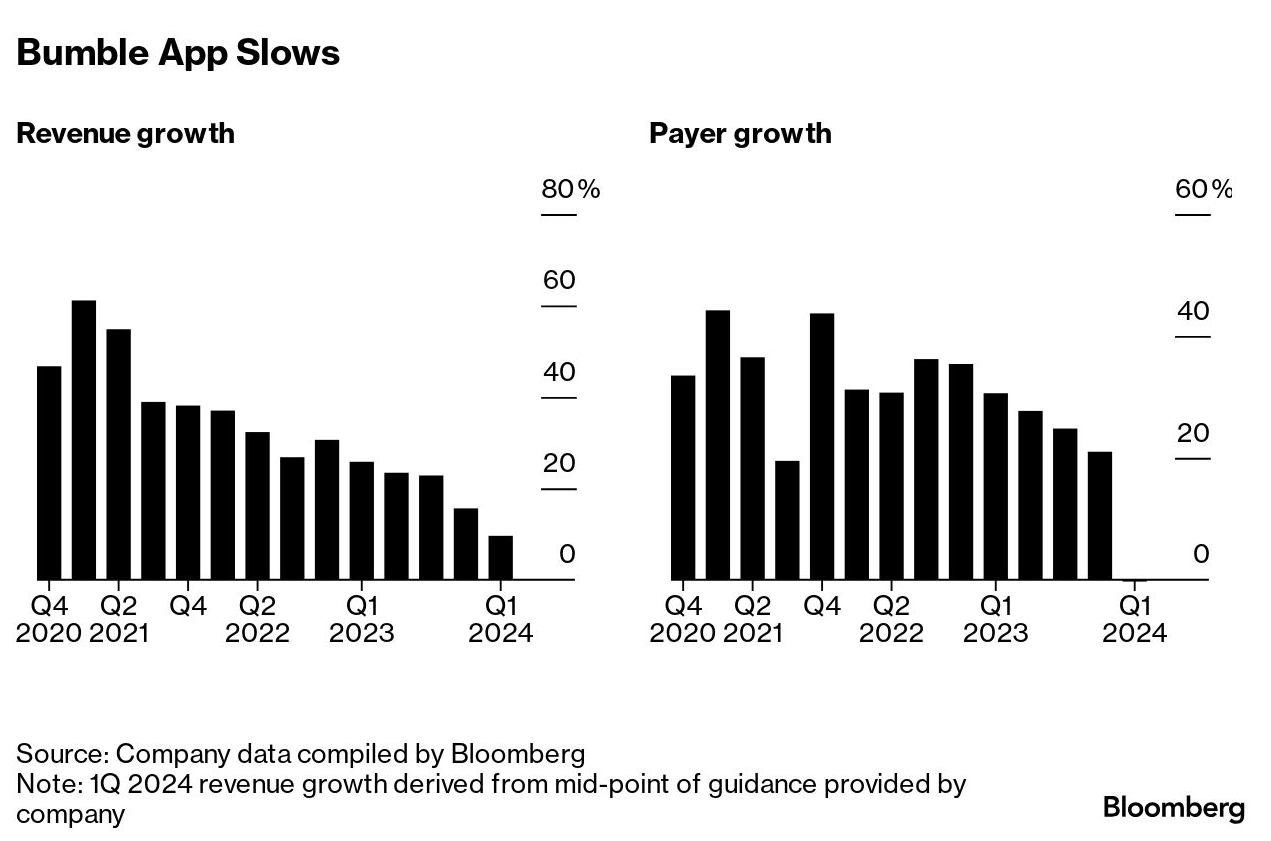

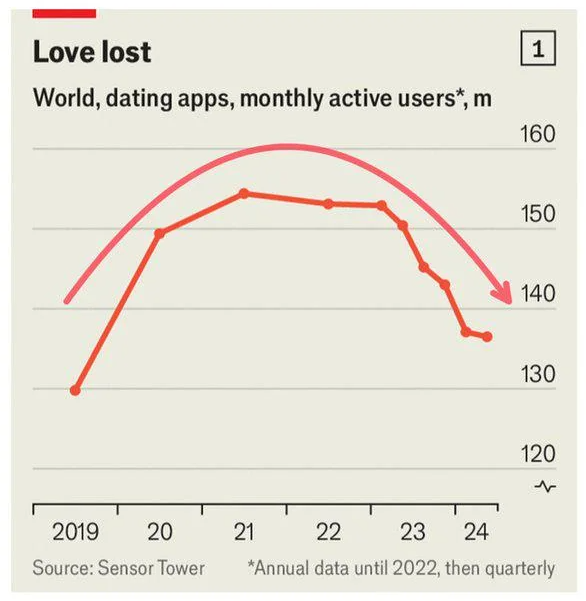

Between May 2023 and May 2024, Tinder lost 594,000 users in the UK. Hinge shed 131,000. Bumble dropped 368,000. By Q2 2025, Bumble's paying users had fallen 8.7% to 3.8 million. Match Group—owner of both Tinder and Hinge—just reported its eighth consecutive quarter of declining payers.

The public markets are screaming. Bumble's stock cratered 30% in August 2024 after slashing revenue guidance. Match Group's Q1 2025 earnings showed total payers down 5% year-over-year to 14.2 million, with Tinder specifically losing 6% of its paying base.

Here's the opportunity: a membership-based dating club in one city generates $7,000-$12,000 monthly profit with a single part-time operator. Scale that to three cities while building the infrastructure platform underneath, and you're running a seven-figure cash-flow business that becomes the Shopify for the entire post-swipe dating economy.

Meanwhile, attendance at in-person dating events surged 42% between 2022 and 2023. Eventbrite logged 1.5 million searches for dating events in a 12-month window, with 376,000 attendees and an average of 128,000 monthly searches. Game-based dating events grew 88-163% depending on format. Athletic dating events—pickleball and spin classes for singles—jumped 136%. Thursday, a dating event company that hosts weekly singles mixers, now operates in 75 cities globally and regularly fills venues with 200-300 people per event.

The generation that grew up fully online is souring on dating apps. Gen Z represents just 26% of U.S. dating app users—older millennials and Gen X dominate the market at 61%. In surveys from 2024-2025, 75-80% of Gen Z report dating app burnout or exhaustion. They're still swiping (Hinge's user base is over 50% Gen Z globally), but they're also the demographic most actively seeking alternatives. The apps that win them will look nothing like Tinder.

Dating apps optimized for engagement instead of relationships. Their business model requires you to stay single and keep swiping. There's a gap between what users want—real connection—and what the product delivers—endless choice paralysis. The opportunity isn't to replace dating apps. It's to serve the massive parallel market of burned-out users who want something that actually works.

The Economics Are Broken in a Way That Creates Opportunity

Industry benchmarks paint a brutal picture. Compiled data suggests only 3-4% of dating app users stick around for 12 months. Less than 15% renew premium subscriptions for a second term. The average user stays active on the same platform for under six months. These aren't products people love—they're products people tolerate until they find something better or give up entirely.

Active users spend 80 minutes per day on dating apps in 2024, down from higher levels in 2021. But only 36% open their apps multiple times per week. More than 41% deleted their main dating app at least once last year. The apps call this "engagement." Users call it exhausting.

Out of 350 million worldwide users, estimates suggest roughly 25 million pay for premium features—around a 7% conversion rate. Match Group pulled in $3.5 billion in 2024, controlling 65% of the U.S. market. Total global dating app revenue hit $6.18 billion. The money's still flowing, but user satisfaction is collapsing. Poor match quality (43%) and ghosting are the top complaints.

The apps know this. Bumble launched Bumble IRL in 2022—hosting spin classes, community service outings, and mixers. Match Group added a "72 Hours" feature designed to "disrupt the incessant messaging" and get people offline faster. Even dating apps are admitting that staying on the app is the problem.

The IRL Dating Event Market Already Exists

Thursday Dating raised $3.5 million in seed funding months after launching in London and New York in May 2021. The company generated 100,000 sign-ups and 7,000 matches on launch day. Their model: the app only works on Thursdays. Users have 24 hours to match, chat, and meet up. The artificial scarcity creates urgency. But the real business is the events—weekly singles mixers in 75 cities with themes ranging from "Holiday Pairing Party" to "Line Dancing Hoedown" to "Singles Movie Night." Events regularly draw 200-300 people at $15-30 per ticket.

Pre-Dating, the oldest speed dating company in the U.S. (founded 2001), runs monthly events in 90+ cities. They've facilitated over 5 million dates. Their model is simple: show up, meet 5-12 people in structured 5-minute conversations, exchange contact info if there's mutual interest. No app required.

Meet IRL in Chicago runs weekly singles mixers, speed dating, wine tastings, and pickleball events. Small operation, female-founded, profitable. Their Instagram has 15,000 followers. Events sell out.

The infrastructure already exists. What's missing is the operating system underneath it—the CRM, scheduling tools, feedback loops, and playbooks that let operators run high-quality events at scale.

Four Reasons This Wins Right Now

Misaligned incentives are obvious. Dating apps make money when you stay single. Match Group's former CEO literally said their goal is "monetizing loneliness." Hinge calls itself "the app designed to be deleted," but their parent company's stock price depends on people not deleting it. Even Hinge's own features confess the problem: they delete matches after 24 hours, limit daily matches unless you pay, and push IRL events. When your differentiation is "we don't want you to use us that much," the category is broken.

When a product's business model directly conflicts with the user's goal, someone else will build the alternative.

The "authenticity economy" is expanding. We're seeing verification businesses emerge across creative industries. Books By People verifies human-written literature. Art Recognition uses ML to authenticate paintings. CREDO 23 certifies films made without AI. These exist because consumers want proof of human effort. Dating is the same. Users want proof they're meeting real people with real intent. A members-only club with referral-based entry and light vetting solves this. The trust layer is the product.

There's a mid-market gap nobody's filling. High-end matchmakers exist for rich people ($5,000-$50,000 per client). Low-end dating apps exist for everyone (free to $40/month). What's missing is the scalable "human over algorithm" experience that's cool and accessible—priced like a gym membership instead of a luxury service.

The supply side is fragmented and amateur. Most IRL dating events are run by individual operators using Gmail + Google Sheets + Eventbrite, venue owners throwing "singles night" as filler for slow weekdays, or matchmakers charging $5,000-$50,000 for 1:1 services. There's no Shopify for matchmakers. No Stripe for dating events. No infrastructure layer that lets anyone spin up a high-quality, repeatable dating club in their city.

The Product: A Membership-Based Dating Club

Forget speed dating. Forget forced icebreakers. Build something people actually want to attend even if they don't meet "the one."

The naming matters. Something like "The Setup Agency" positions you as the anti-app from day one—intentional, curated, human-run. But pick whatever works for your market.

Core Principles

Do not deviate from the following 3 principles:

Unlock the Vault.

Join founders who spot opportunities ahead of the crowd. Actionable insights. Zero fluff.

“Intelligent, bold, minus the pretense.”

“Like discovering the cheat codes of the startup world.”

“SH is off-Broadway for founders — weird, sharp, and ahead of the curve.”